HHS - Harte Hanks: Results Could Improve Soon But Little Upside Right Now

2023-07-23 00:14:42 ET

Summary

- The company’s revenues and EBITDA dropped by 4% and 47.2% in Q1 2023, respectively, but this was mainly due to a lack of one-offs and pandemic-related projects.

- In my view, EBITDA could surpass $17 million for 2023 as margins improve over the coming months.

- Unfortunately, the margin of safety isn't high enough for me to consider opening a position at this time.

Introduction

I like to write about microcap stocks on SA, and today I want to talk about Harte Hanks (HHS). It’s a global customer experience company that had a tough start of 2023 with Q1 revenues declining by 4% and the net loss coming in at $0.8 million. I expect the remainder of the year to be better but I think that the company isn't particularly cheap at the moment from a fundamentals point of view. Harte Hanks currently has a TTM EBITDA of $15.5 million and the EV/EBITDA ratio is just below 4.2x. My rating on the stock is neutral.

Overview of the business and financials

Harte Hanks was founded in 1923 and its business is split into three segments - marketing services, customer care, and fulfillment and logistics services. The marketing services segment specializes in strategic planning, data strategy, performance analytics, creative development and execution, technology enablement, marketing automation, and database management solutions. Customer care, in turn, focuses on advanced contact center solutions including speech, voice and video chat, integrated voice response, analytics, social cloud monitoring, and web self-service. And finally, the fulfillment and logistics services segment is involved in the provision of B2B product and literature fulfillment, B2C e-commerce and sampling, and end-to-end supply chain and logistics services. Harte Hanks has 11 offices across North America, Asia Pacific, and Europe and the average client tenure is 12 years. It employs about 2,500 people and its customers include Ford (NYSE: F )), International Business Machines (IBM), and Pfizer (PFE) among others.

{kind=link}

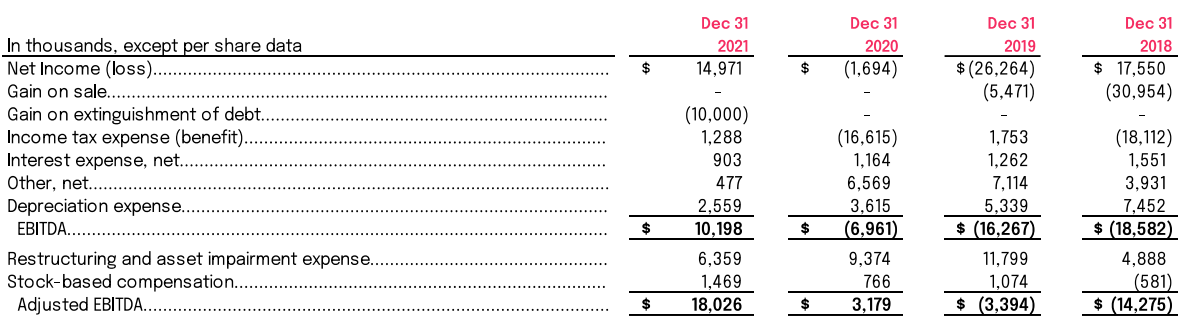

The company was struggling financially in the middle of the last decade, and it embarked on a restructuring process in 2019 that included shrinking the business and focusing on profitable core areas as well as going for an asset-light business model. Several offices were closed, and unprofitable contracts were cut. In addition, Hanke Hanks opened a 400,000-square-foot logistics facility in Kansas City that became one of its primary logistics hubs. In my view, the restructuring was successful as adjusted EBITDA was back in the black by 2020 while the net income returned to positive territory in 2021.

{kind=link}

Revenues shrank from $284.6 million in 2018 to $176.9 million in 2020 but returned to growth in 2021, reaching $206.3 million in 2022. Overall, I think that 2022 was a solid year for Harte Hanks as sales rose by 6% while net income soared by 145.3% to $36.8 million. Yet, it's worth noting that the latter included a $19.8 million tax benefit.

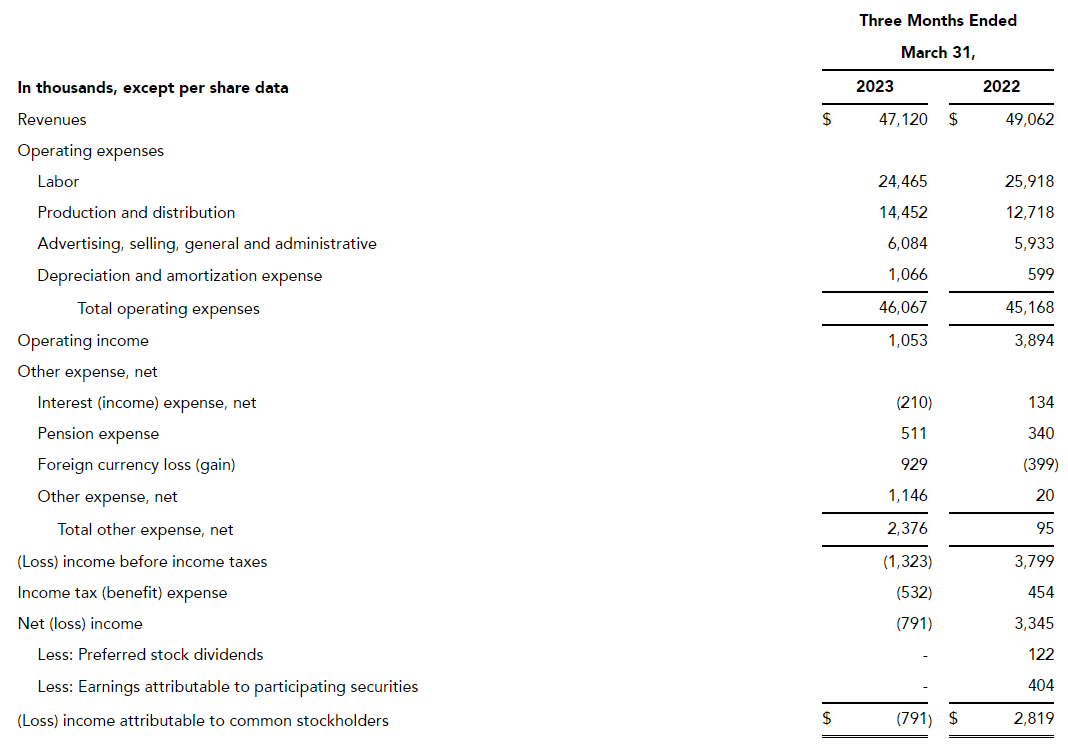

Looking at the Q1 2023 financial results of Harte Hanks, we can see that revenues fell by 4% year on year to $47.1 million and the company swung to a $0.8 million net loss from a $2.8 million net income a year earlier. EBITDA, in turn, slumped by 47.2% to $2.1 million.

{kind=link}

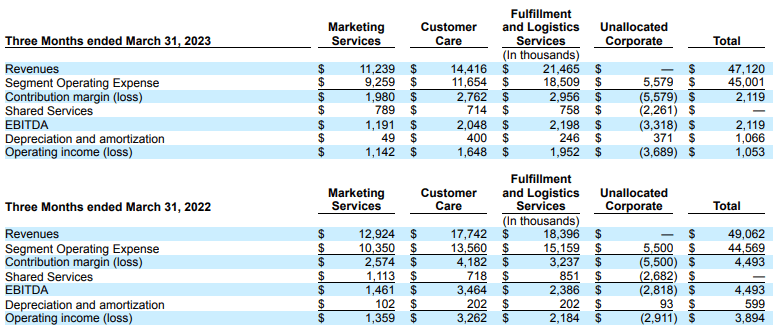

The financial results look underwhelming at first glance, but I think that they aren’t so bad considering Q1 2022 benefitted from a one-time product recall project and pandemic-related projects. This affected mainly the customer care segment where federal and state-funded pandemic-related projects ended in the second half of 2022. The revenues of the marketing services segment dipped due to the roll-off of direct legacy direct mail campaigns and reduced spend from B2B tech customers while the fulfillment and logistics segment continued to grow. Yet, the EBITDA of the latter fell slightly to $2.2 million due to the increase in the share of lower-margin logistics solutions.

{kind=link}

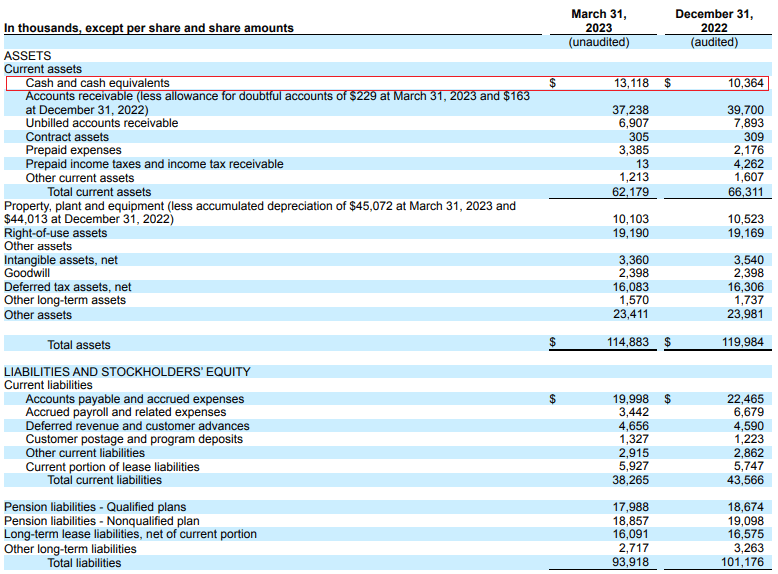

On a positive note, free cash flow for the quarter came in at $1.2 million while cash and cash equivalents increased by $2.8 million quarter on quarter to $13.1 million as of March 2023. Harte Hanks has no debts and I think that the balance sheet looks solid at the moment. Yet, it's worth noting that pension liabilities stand at $36.8 million which is a significant figure for a company of this size.

{kind=link}

Looking at the future, the company said during its Q1 2023 earnings call that it expects a sequential improvement in EBITDA for Q2 and I’m optimistic that EBITDA for the year could remain above $17 million. Harte Hanks said during the earnings call that it’s combining its marketing services and customer care segments into a new segment called customer experience and I expect this move to result in operating margin improvement over the second half of 2023. In addition, Harte Hanks approved a $6.5 million share buyback program which I think could provide support for the share price over the coming months considering its market capitalization has fallen to just $41 million as of the time of writing.

Turning our attention to the valuation, Harte Hanks has an enterprise value of $64.7 million (note that I included pension liabilities in net debt calculations but not lease liabilities) and is trading at an LTM EV/EBITDA ratio of 4.2x. If EBITDA increased to $17 million in 2023, this ratio would drop to 3.8x at today's share price. Considering that the company has a stable business with several blue-chip customers and that its profitability should improve over the coming months, I think that it should be trading at above 4x EV/EBITDA. Unfortunately, the margin of safety isn't high enough for me to consider opening a position at this time.

Looking at the downside risks, I think that the major one is that I could be overoptimistic about the improvement in EBITDA over the remainder of 2023. If this proves to be a challenging year for Harte Hanks and EBITDA drops below $10 million, the share price could fall under the $4.00 mark. In addition, this is a thinly traded stock and the daily trading volume rarely surpasses 30,000 shares. In my view, we could see significant share price volatility in the future, and it could be hard to exit a large position here.

Investor takeaway

In my view, Harte Hanks completed a successful restructuring of its business over the past few years and the company has a strong balance sheet with over $13 million in cash and no debts. Yet, pension liabilities stand at $36.8 million. The Q1 2023 financial results looked weak due to the lack of one-offs and pandemic-related projects, and I expect EBITDA to surpass $17 million for 2023 as margins improve. However, I think the margin of safety here is too thin and this is why I'm putting a neutral rating on HHS stock.

For further details see:

Harte Hanks: Results Could Improve Soon, But Little Upside Right Now