HHS - Harte Hanks: Stock Could Reasonably Double In 2023 On Cash Flow ROIC Strength

Summary

- Harte Hanks might have temporary headwinds in 2023 with an expected decline in earnings as compared to 2022.

- However, the long-term earnings growth looks positive.

- The low valuation and weakness in the stock are setting up a good buy point for a long-term position.

- Harte Hanks is improving the company for the long term with a new acquisition.

This article continues my ongoing coverage of Harte Hanks ( HHS ), a company involved in customer service, marketing, and fulfillment/logistics services. The stock did double in price from May to August in 2022 after my last article . However, the stock did decline since then. I believe the current weakness in the stock will set up another good run after we get past the uncertainties of the current economic situation.

Harte Hanks operates in three segments: Marketing Services, Customer Care, and Fulfillment & Logistics Services. In a nutshell, Harte Hanks provides strategic guidance to clients for comprehensive marketing which includes planning & executing marketing plans, customer identification, predictive modeling, on and offline marketing, and data strategy services. The company also provides website and app development, database building & management, and other marketing-related services. The company has many well-known large corporate clients.

Why the Recent Weakness in the Stock?

The stock did reach an overbought level in August 2022. This led to a significant pullback in the stock as many traders probably took profits after the sizable run up. Over the past month, earnings estimates were lowered by about 11.5% for 2023. This may have led traders to sell the stock. The company is scheduled to report earnings on March 14, 2022 for Q4 2022. This report is likely to provide more insight into the outlook for 2023.

Another concern for Harte Hanks has been the pension obligations which were $49.6 million on the latest balance sheet. The high amount of pensions led the company to have $3.1 million more total liabilities than total assets, giving Harte Hanks negative equity. The good news is that the pension obligations have decreased each year from $70 million in 2019.

Keys to Growth

The services that Harte Hanks provides is needed for its clients to maximize sales through various marketing channels and data. This is something that clients need even if the economy goes soft in 2023. So, Harte Hanks should have some resilience during the economic uncertainty of this year.

The long-term outlook appears bright for Harte Hanks. Each market for the company's business segments is projected to grow. The marketing and analytics software market is expected to grow at about 14% annually to reach $14.3 billion by 2031. The global customer care services market is projected to grow at 4.5% annually to 2027. The global ecommerce fulfillment market is expected to grow at 9.5% annually to reach $198.6 billion by 2030. Harte Hanks is likely to get its piece of the pie as this market growth can act as a positive tailwind for Harte Hanks' revenue growth.

The company is projected to grow revenue at about 10% in 2023. Earnings are projected to be 11.5% lower in 2023 as compared to 2022. However, earnings are expected to average 12% annual growth over the next 3 to 5 years. I would put more emphasis on the long-term multiple year expected growth.

New Acquisition

Harte Hanks acquired all of the assets of InsideOut Solutions for $7.5 million in December 2022. InsideOut is involved in building, scaling, and optimizing inside sales initiatives for large companies, including many Fortune 500 companies. The acquisition can help Harte Hanks better serve its clients by driving their growth through enhanced sales/marketing programs.

Revenue is immediately accretive from the acquisition and Harte Hanks expects to get cost synergies that will drive its valuation to the 3x to 4x EBITDA range.

Valuation

HHS is trading with an attractively low valuation. Just check out these metrics.

| Harte Hanks |

| Sector Median |

| Forward PE |

| 6 |

| 16 |

| PEG Ratio |

| 0.50 |

| 1.45 |

| Price/Sales |

| 0.37 |

| 1.32 |

| Price/Cash Flow |

| 2.95 |

| 7.78 |

source: Seeking Alpha

Harte Hanks is deeply undervalued with a forward PE below 10 and with a PEG ratio and price/sales below 1. The low price to cash flow ratio reinforces the company's attractive valuation.

You are probably wondering why a profitable company like HHS is trading at such a bargain valuation. One reason for this is because Harte Hanks has high pension obligations. The balance sheet shows $49.6 million in pension obligations. The good news is that this figure has been reduced every year for the past three years from the $70 million in pension obligations that HHS had in 2019.

Another reason for the low valuation is probably due to the negative operating cash flow that HHS had in 2020 and 2021. However, that has turned around significantly as HHS had $26.4 million in positive operating cash flow over the past 12 months.

One other concern that potential investors have pondered is the company's large amount of total debt of $21.1 million while total cash and equivalents are only $6.9 million. The significant improvement in cash flow puts the company in a much better position to pay down the high amount of debt over the long-term.

I'd like to point out an important metric that should put potential investors at ease. That is the company's high ROIC of 70% that HHS achieved over the past 12 months. This shows that HHS is highly effective in allocating capital for profitable returns. Although the debt is high, the high returns that HHS is achieving plus the positive cash flow generation outweighs the debt risks in my opinion.

With the improvements of lower pension obligations, the return of strong operating cash flow, and high ROIC, HHS has room for PE expansion as the company continues to grow over the next few years. Investors are likely to take notice of these improvements and bid up the stock price.

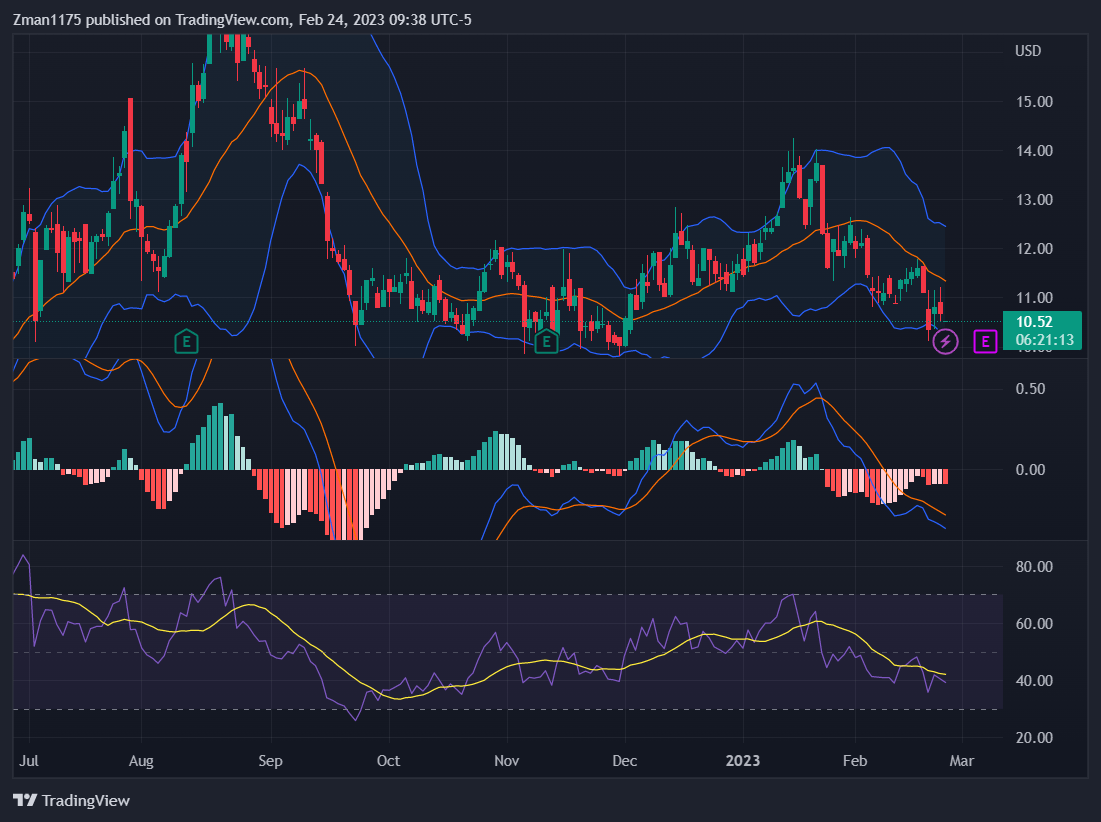

Technical Analysis

{kind=link}

The stock is trading about 41% below its 52-week high of $17.88. The price has some near-term support around the $10 area. Unless the company reports some unexpected negative news, I wouldn't expect the price to fall much below that level.

Of course, the stock could also drop on a broad-market sell-off. Investors should watch for the stock to bounce higher from a support level. The MACD indicator in the middle of the chart would display a change in trend back to positive when the blue line crosses above the red signal line. The RSI (purple line at the bottom of the chart) would also show a bounce higher possibly from an oversold level (similar to what occurred in September into October). These conditions would indicate a better entry point.

Harte Hanks Investment Outlook

The deep, low valuation should help the stock from dropping too steeply. Harte Hanks would probably have to report some significant unexpected negative news for the stock to drop below the $10 support level in my opinion. The company is scheduled to report earnings on March 7 after the market close. So, investors may want to wait to see how the company reports and guides for the rest of the year before starting a position. A positive report with positive guidance could be the catalyst that shifts the stock into a new uptrend.

Analysts have a one-year $22 price target for the stock. This would more than double the current stock price. The $22 target would take the PE ratio up to 13.7 based on expected EPS of $1.61 for 2013. That would still be below the S&P 500's ( SPY ) PE of 20.

The price target is reasonable in my opinion as the company has been producing positive cash flow, reducing its pension obligations, achieving high ROIC, and as it gains synergies from the InsideOut Solutions acquisition.

For further details see:

Harte Hanks: Stock Could Reasonably Double In 2023 On Cash Flow, ROIC Strength