HAS - Hasbro: Excess Debt Leaves Shares Unattractive

2023-12-19 20:13:41 ET

Summary

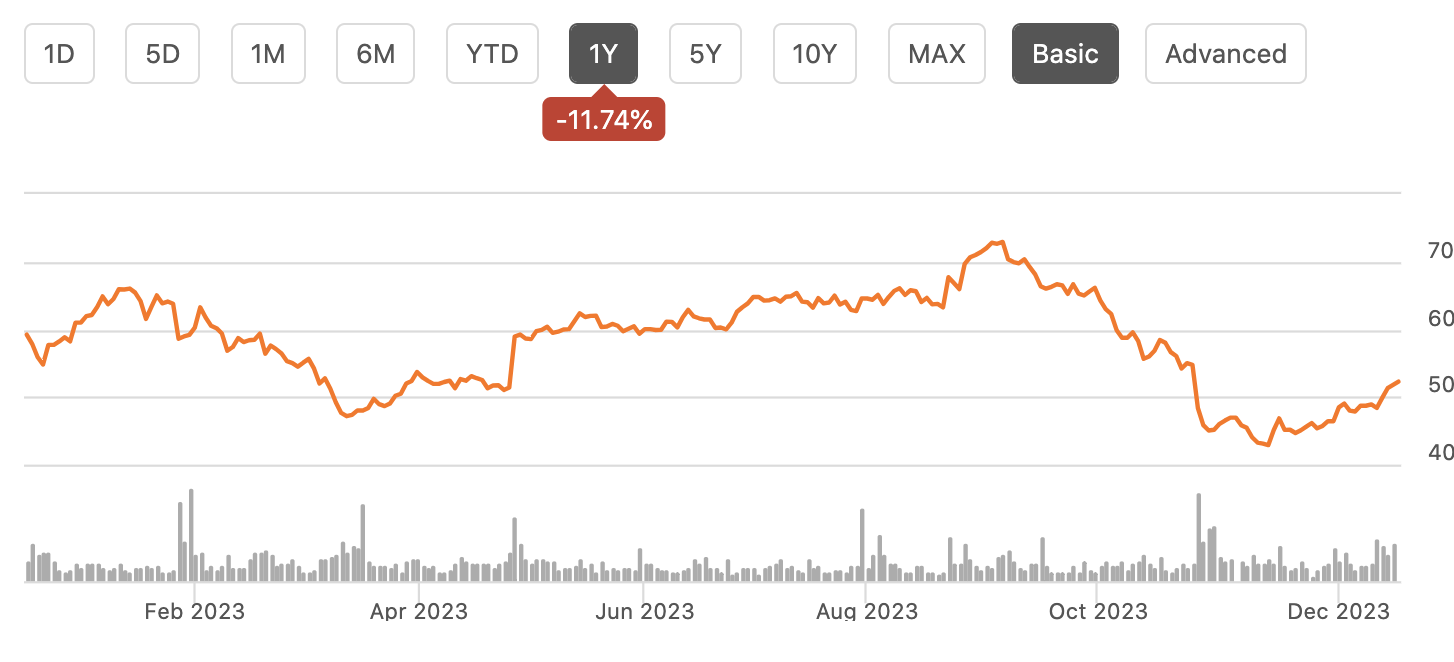

- Hasbro has been underperforming, with shares down 12% in the past year and nearly cut in half since the beginning of 2022.

- The company announced 900 layoffs and aims to reduce expenses by $100 million, showing progress in cost-saving efforts.

- Toy spending is likely to be down 10+% this year, reaching a decade low, and Hasbro's revenue is expected to decline by 13-15% in Q4.

- While toy spending may be bottoming, reducing debt will be a multiyear process after its failed media efforts, leaving shares unattractive.

Hasbro ( HAS ) has been a meaningful underperformer over the past year with the stock down 12%. This has added to long-term underperformance, and shares have been nearly cut in half since the beginning of 2022. The company has been hit with a toy spending recession while its foray into entertainment was a failed experiment. Its balance sheet is likely to take several years to fix, so even with shares beaten up considerably, I would not be a buyer here.

{kind=link}

Given the challenges it faces, last week on December 11th, Hasbro announced another 900 layoffs, aiming to reduce run-rate expenses by $100 million. Combined with earlier layoffs, the company expects to have reduced its cost structure by $350-400 million by the end of 2025. There will be $40 million of incremental one-time expenses to implement these additional cuts. While Hasbro’s revenue has come under significant pressure, these cost-savings effort are showing some progress.

In the company’s third quarter released in October, it reported adjusted earnings of $1.64, $0.05 below consensus , as revenue fell by 11% to $1.5 billion. Consumer products revenue fell by 18% while entertainment declined by 42%, due to the writers’ strike. Its Wizards of the Coast/Digital Gaming unit did see 40% revenue growth to $424 million with segment operating profits doubling to $203 million. Digital revenue doubled while tabletop revenue rose by 18%. This segment which houses games like Dungeons and Dragons has been the one standout and sole generator of growth.

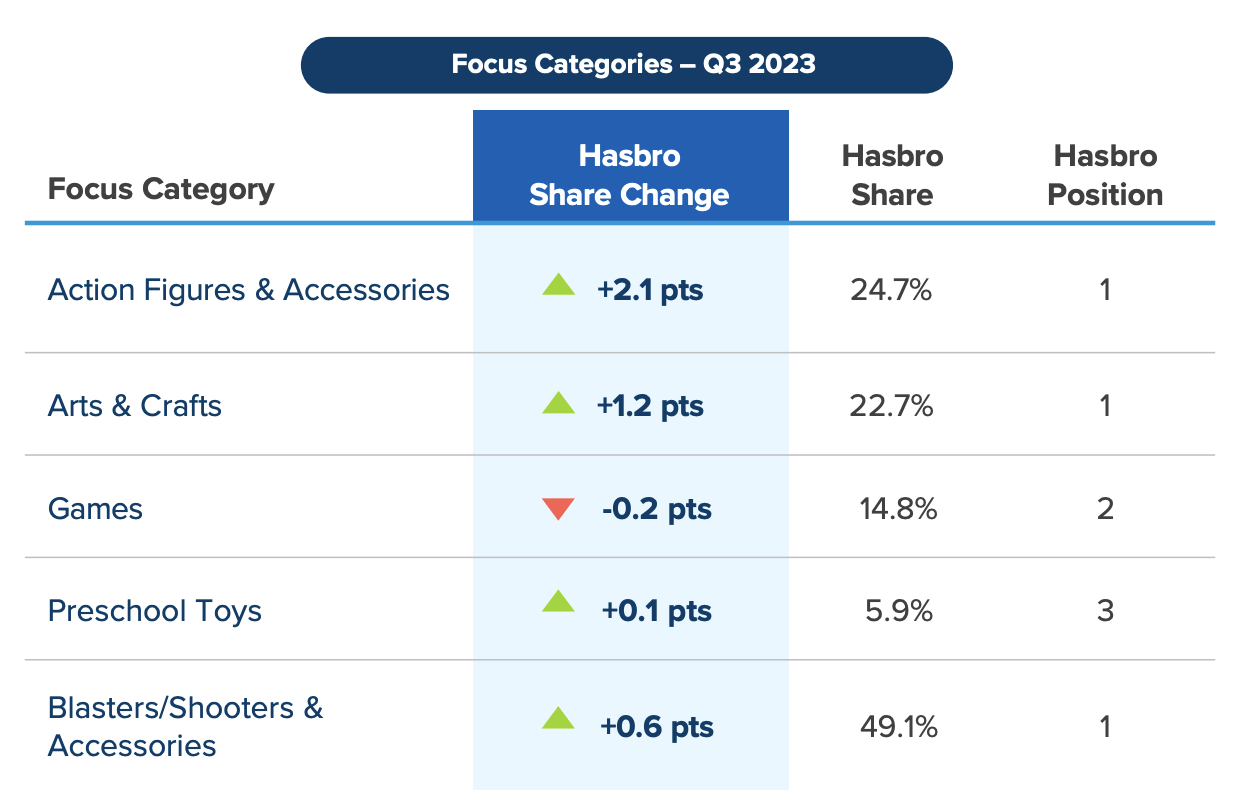

This good news has been offset by consumer products where revenue fell by 18% to $957 million with adjusted operating profits down 26% to $107 million. Margins fell by 140bp to 11.2%. The challenge here is less executional than macro: families are spending less buying toys. As you can see below, Hasbro has generally been a share winner this year in its key competitive categories. It is not as though sales are declining because it is losing out on sales to competitors. The toymakers are simply fighting over a shrinking pie. Overall, Dungeons and Dragons and Transformers were both up solidly while partner brands have been soft.

{kind=link}

The government only releases data on toy spending annually, but based on Hasbro and Mattel ( MAT ) results, toy spending is likely to be down 10+% this year, meaning it will be about $150. Adjusted for inflation, that will bring spending to a decade low. I am inclined to think that spending on toys is getting to be about as bad as it can be.

St. Louis Federal Reserve

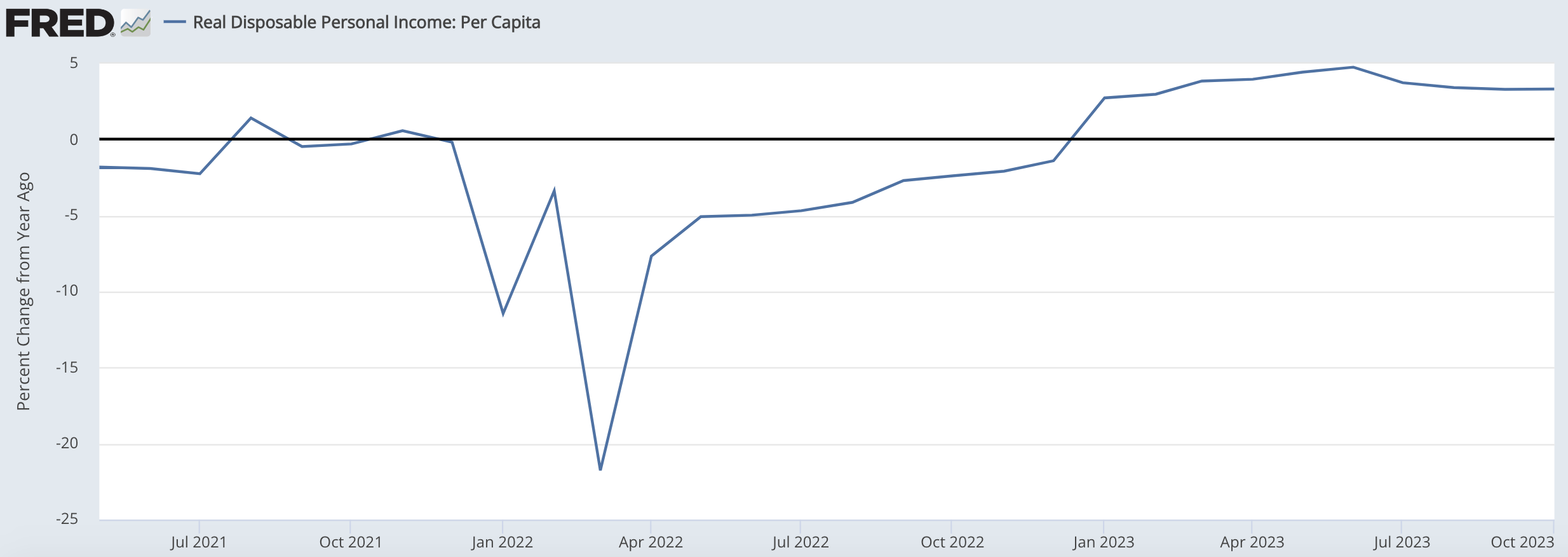

One positive possibility for 2024 is that spending this year may have been crunched by higher inflation, weighing on disposable income. But with incomes now rising in real terms thanks to a strong labor market and diminishing inflation, consumers should have more room to spend on discretionary items, like toys in 2024.

{kind=link}

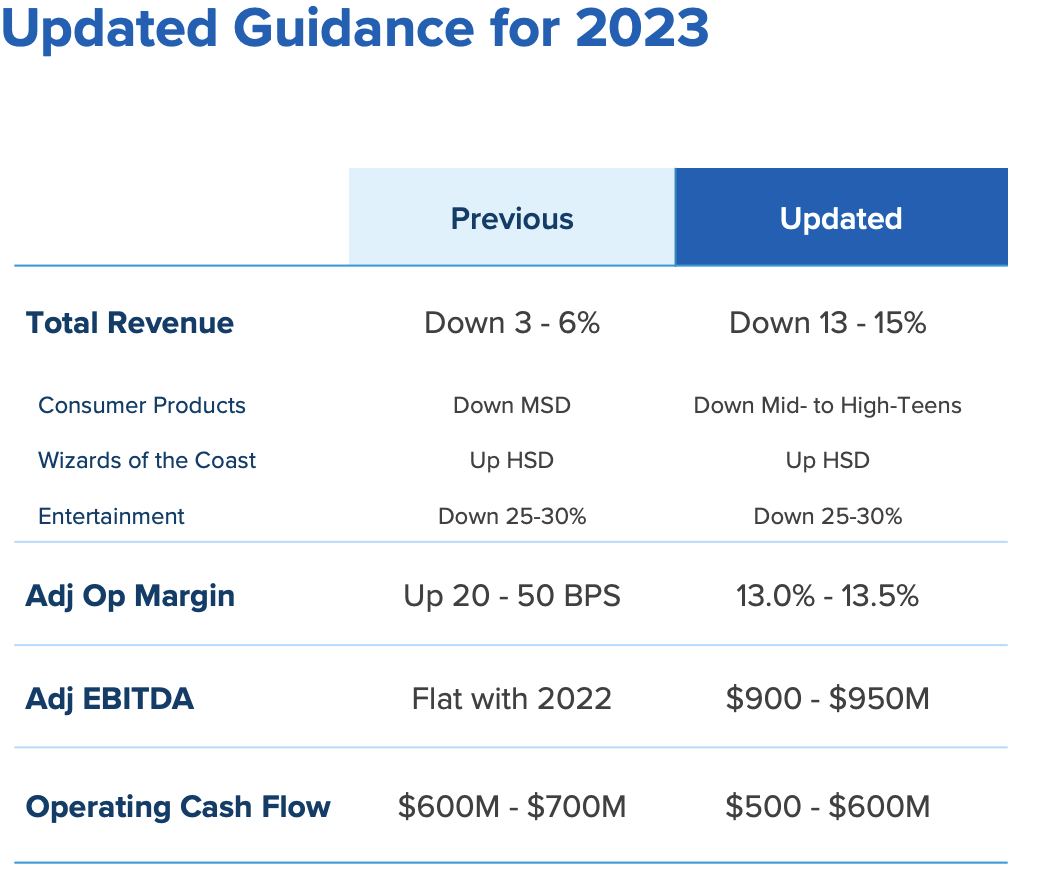

While this may help 2024 results, it does not appear this recovery in incomes has been sufficient to save the Christmas season. Alongside Q3 results, Hasbro significantly cut guidance. The company now expects revenue down by 13-15% as consumer products declines by mid-to-high teens. This should result in $500-$600 million of operating cash flow, and about $300-400 million of free cash flow. Hasbro’s dividend is about $385 million, consuming essentially all of free cash flow. This guidance points to a fairly weak Q4.

{kind=link}

In the face of this macro weakness, Hasbro is doing what any prudent management team would do: cut expenses. Cost of goods sold declined from 35% of revenue to 32.9%. Product development spending fell by 7%. Advertising spending was down by 29%. SG&A was down by 3.5%. Improved supply chains and layoffs have helped the company bring down expenses across the board, which is a reason why Adjusted EBITDA rose by 16% to $402 million

Additionally, Hasbro has been aggressively destocking inventories. Consumer product inventories are down by 34% with total inventories down 27%, at $618 million from $845 million last year. Decreased inventories should help to reduce pricing pressure and preserve margin next year.

While the company is struggling, given the prospect of toy sales bottoming and constructive actions on the cost front, I could see why investors are inclined to buy into shares after their decline the past year. However, its misadventures in media and associated balance sheet harm leave me on the sidelines. Hasbro carries $3.65 billion in debt following media acquisitions. While Mattel has had success this year with Barbie, Hasbro has seen less success, with Dungeons and Dragons notably stumbling at the box office this year and Transformers a much smaller box office force today than fifteen years ago. As such it is selling the eOne film and TV business, booking a $473 million loss on this failed effort. It expects to complete the sale by year end.

The sale of eONE will provide $375 million in cash and the offloading of about $125 million in debt, allowing the company to reduce its debt load by a minimum $400 million, eliminating floating rate debt from its capital structure. While this debt reduction will reduce interest expense, it has $500 million of 3% notes due next December that likely will need to be refinanced at a higher rate, adding back interest expense.

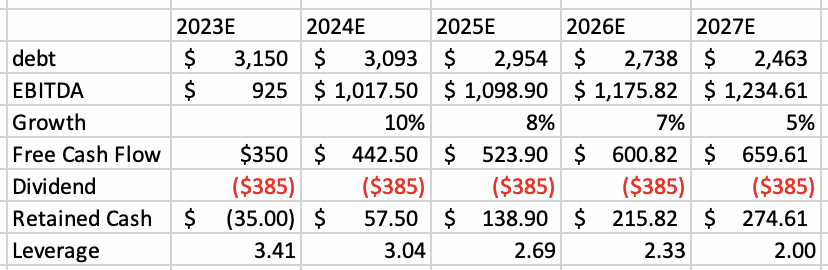

Management targets 2-2.5x leverage (Debt/EBITDA). Based on guidance, leverage is nearly 4x today. However, the deleveraging from the eOne sale will reduce leverage by about 0.5x. The challenge is its dividend is consuming nearly all of its free cash flow, which means it will be a very long process to bring leverage to target. Until it does so, any material share repurchases are unlikely. Investors can collect a 5.6% yield, but that will be the only capital return.

Given my view that toy sales may be “as bad as they can get” absent a recession, I assume about 10% growth next year, gradually slowing to a potential growth rate of 5% by 2027. This forecast would translate to 33% EBITDA growth over four years, a relatively optimistic outlook. If the company allocates all cash to debt reduction, it will only return to its targeted leverage level at the end of 2026, finally opening the door to buyback in 2027.

{kind=link}

Three to four years to wait for an increase in shareholder returns is a long time. At a 10x EV/EBITDA and with a 5% free cash flow yield, shares are not particularly cheap to discount such a long turnaround. That leaves me with the view shares are likely to be dead money in the $45-55 range for a prolonged period as investors wait to see if this debt paydown effort remains on track. One thing that keeps me from moving to an outright “sell” rating is the risk that the company could seek to split off or sell its higher-performing digital assets to accelerate this process. I would note Capital Research has a 10% passive stake in the company. While this stake is passive, if the company struggles further, Capital or another investor could seek to accelerate change and go activist, which could provide at least a short-term lift to shares.

Being patient in investing is often effective as it can take time for a thesis to play out. However, it is important for investors to be compensated fully for the level of patience required. I would see an argument for being patient on a toy sales turnaround, but given the balance sheet hole Hasbro is working out off, I think shares are not attractive enough today to wait for three years. I would rather own Mattel , which would benefit from a toy rebound and has more successful media efforts than Hasbro. While an activist investor could be a positive catalyst, I do not see that as sufficient reason to buy HAS, which I expect to languish around current levels.

For further details see:

Hasbro: Excess Debt Leaves Shares Unattractive