HAS - Hasbro: I See A Real Deep-Value Style Fat-Pitch Opportunity Here

2023-11-15 01:34:34 ET

Summary

- Hasbro is the largest toy manufacturer in the world with a huge set of valuable franchises and licensing agreements bolstering their wide portfolio of toys.

- The company has successfully transitioned into the digital realm with both critically and consumer acclaimed product releases driving strong revenue growth for the business units.

- Despite a decline in total revenues due to external macroeconomic and competitive factors, Hasbro has maintained profitability and improved operating margins.

- A potentially massive 68% undervaluation in shares may be present.

- Strong Buy rating issued.

Investment Thesis – Q3 FY23 Update

Hasbro ( HAS ) remains one of my favorite deep-value, Buffett-style fat pitch opportunities. The recent selloff came after what I believe were largely misinterpreted earnings results.

The margin expansion, increased operating profit and massive reduction in costs has been ignored by the markets with the significant drop in consumer products and entertainment revenues instead dominating the headlines.

However, I believe this selloff has only strengthened the value opportunity potential present in shares with current valuations suggesting the stock may be up for grabs at a 68% discount.

Therefore, I continue to rate Hasbro stock a Strong Buy.

Company Background

Hasbro is an American MNC conglomerate headquartered in Pawtucket, Rhode Island. The company owns some of the largest toy brands in the world including Milton Bradley, Parker Brothers and Wizards of The Coast.

The company was founded over 100 years ago and continues to be one of the largest toy manufacturers in the world. Their portfolio of products includes partnerships with huge franchises such as Star Wars, Marvel, Transformers, Furby, Nerf, My Little Pony and even Peppa Pig.

Their immense scale and huge portfolio of brands has left the company with a significant set of valuable tangible and intangible assets which help drive moatiness for the firm’s business operations.

While their primary competitor Mattel ( MAT ) is a slightly smaller company, the incredibly competitive nature of the toy industry means Hasbro must continue to innovate and maintain a relevant portfolio of products in order to attract new customers.

Economic Moat – Q3 FY23 Update

I conducted a full in-depth analysis on Hasbro’s economic moat back in March 2023 and rated the firm a Strong Buy. I believe that fundamentally, little has changed with regards to the firm’s economic moat or my investment thesis.

The firm still have the largest and most robust economic moat of any company operating within the toy industry thanks to their unique portfolio consisting of both physical and digital products that market to a wide variety of customers.

To read a comprehensive analysis into Hasbro’s narrow yet robust economic moat, checkout my article “ Hasbro: Good Business At An Amazing Price ”.

In this update article, I would like the discuss Hasbro’s digital product releases, the progress made towards closing the eOne entertainment sale and how the firm is managing Wizards of the Coast.

The past quarter saw Hasbro make multiple digital product releases that resonated soundly with both consumers and critics alike.

Hasbro FY23 Q3 Earnings Presentation

Hasbro released a Dungeons & Dragons themed CRPG computer game titled “Baldur’s Gate 3” which sees the company translate one of their most lucrative physical franchises into a truly revolutionary video game.

Critical acclaim for the release has been outstanding with IGN ’s Leana Hafer stating the game sets a new “high-water mark for the entire genre” of games.

This critical and consumer acclaim appears to have translated well into earnings for the firm too with their Wizards of the Coast & Digital gaming segment reporting massive 40% YoY increases in revenue.

Some critics suspected that Hasbro may have been mismanaging the Wizards of the Coast franchises due to excessive monetization and some less than stellar product releases. However, I believe Hasbro has righted those mistakes by refocusing on what their core customers enjoy most which fundamentally encompasses the firm’s “Refocusing on Play” turnaround strategy.

Hasbro FY23 Q3 Earnings Presentation

Hasbro’s mobile Monopoly game offering, “ Monopoly Go! ”, also continues to generate great revenue growth for the firm. The game has been made in partnership with Scopely an established mobile game developer.

This deal has allowed Hasbro to sell licensing rights to Scopely which generates revenue for Hasbro through royalties due to the firm.

Overall, the combined successes within Hasbro’s Wizards of the Coast and Digital Gaming segments suggests that this transformative step towards becoming a combined physical toy and media powerhouse has worked well for the firm.

Furthermore, the progress made towards closing the sale of eOne to Lionsgate means Hasbro should be able to complete this deal by the end of the year. The initial concept behind eOne was that Hasbro could produce their film, TV and gaming content inhouse.

While this initial belief was misinformed, Hasbro has been quick to admit their mistakes by divesting the business unit and refocusing their digital product strategy on one that revolves around licensing agreement sales and close collaboration with established media powerhouses.

I believe this strategy should allow Hasbro to massively outperform the roughly 10% margins the firm was able to extract from the eOne business thanks to the less resource intensive strategy now being pursued by the firm.

Financial Situation – Q3 FY23 Update

Hasbro’s most recent Q3 results delivered a slightly mixed bag of fiscal results which I believe ultimately have been misunderstood by the markets.

HAS FY23 Q3 Earnings Presentation

{kind=link}

Adjusted earnings for Q3 (due to the negative impacts GAAP accounting methods would inflict on results as a consequence of the eOne divestiture) saw Hasbro’s total revenues fall 10% YoY to just $1.5B.

This earnings weakness was due to a massive 18% and 42% drop in revenues YoY from Hasbro’s Consumer Products and Entertainment business segments.

Consumer Products revenues declined sharply due to a flurry of macroeconomic and competitive headwinds. The resurgence of Mattel’s Barbie set of dolls and toys has potentially negatively impacted Hasbro’s overall sale of toys due to the currently “in” nature of the pink franchise among consumers.

The increasingly bearish macro conditions currently impacting consumers across the globe has placed a real strain on the amount of disposable income consumers have to spend on toys and non-essential items.

European and Asian markets have been hit particularly hard with the U.S. markets seemingly only being buoyed by credit card debt .

However, the key here is that none of the headwinds responsible for this decline in core consumer product sales was due to failed execution or mismanagement on the part of Hasbro.

Inevitably, competing brands will occasionally achieve perfected execution of product launches that sees popularity increase in the short-term. Equally, the toy market has always largely been tied to the prevailing macroeconomic conditions.

Therefore, while the drop in earnings from Hasbro’s core business are regrettable, nothing is fundamentally wrong at the firm.

A similar narrative appears to be present within the firm’s entertainment business with the Hollywood actors and writers strikes of 2023 having led to a whopping 42% drop in revenues YoY.

While the resolution of theses strikes has been positive, I believe it may take up to around 4 months for the damage to content pipelines caused by these industry actions the be rectified.

Still, Hasbro is proactively working with their relevant industry partners to ramp-up production of new releases and content to ensure their entertainment business rebounds meaningfully moving into 2024.

HAS FY23 Q3 Earnings Presentation

{kind=link}

Adjusted operating profit for Q3 FY23 still increased 27% YoY thanks to a favorable product mix of high-margin digital game revenues and lower royalty & operating expenses. The firm has also exceeded their 2023 cost savings target if $150M with total gross savings estimated to currently be around $200M and still increasing as the firm moves towards the end of FY23.

The firm’s operating margin also increased to 22.8% up from just 16.1% in FY22. Fundamentally, despite the falling revenues, Hasbro has become an even more profitable and efficient firm.

I firmly believe that the core objective for a business is to generate profits, not revenues. Following this line of thought, Hasbro has arguably become an even better business in Q3 FY23 despite the overall consensus from investors.

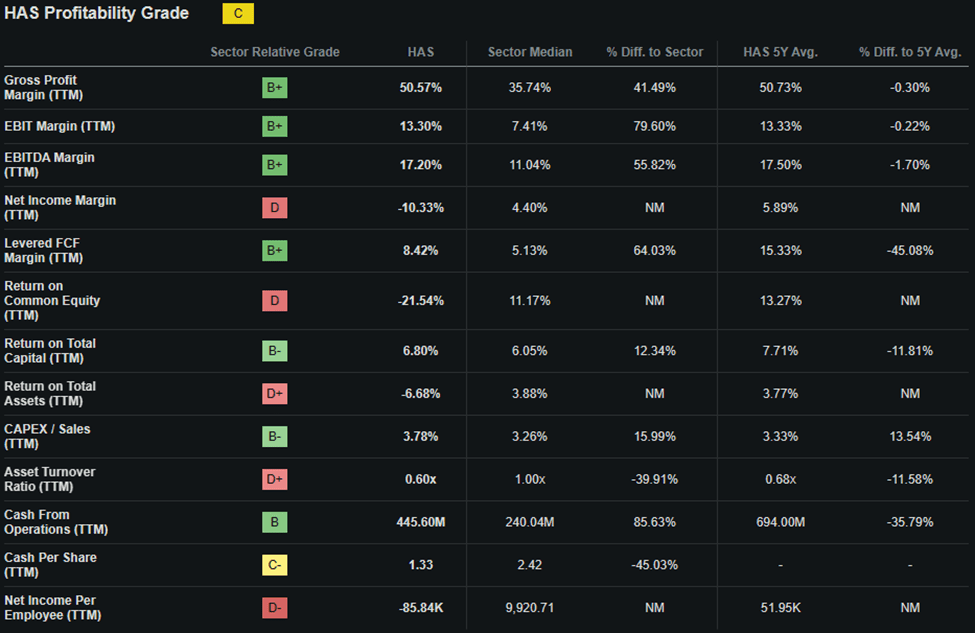

Seeking Alpha | HAS | Profitability

{kind=link}

Seeking Alpha’s Quant has downgraded Hasbro’s profitability rating to a “ C ” which I believe is an excessively pessimistic representation of the core profitability present at Hasbro given the aforementioned reasons for their drop in revenues.

Hasbro’s balance sheets continue to be in healthy shape with the divestiture of their eOne business set to further strengthen their fiscal stability. Their existing debt remains efficiently structured with no huge maturities due before 2029.

Moody’s continues to affirm Hasbro’s senior unsecured domestic debts at a Baa2 rating while their domestic commercial paper is rated a P-2. Moody’s classifies Baa2 ratings as being of “medium investment grade” while P-2 are considered of medium short-term quality.

Overall, I believe Hasbro is excelling both on meeting their turnaround goals and increasing the margins present within their business. The divestiture of eOne promises to further expand the firm's margins while a more favorable macroeconomic environment should lead to revenues growing YoY in the low double-digit range.

Valuation – Q3 FY23 Update

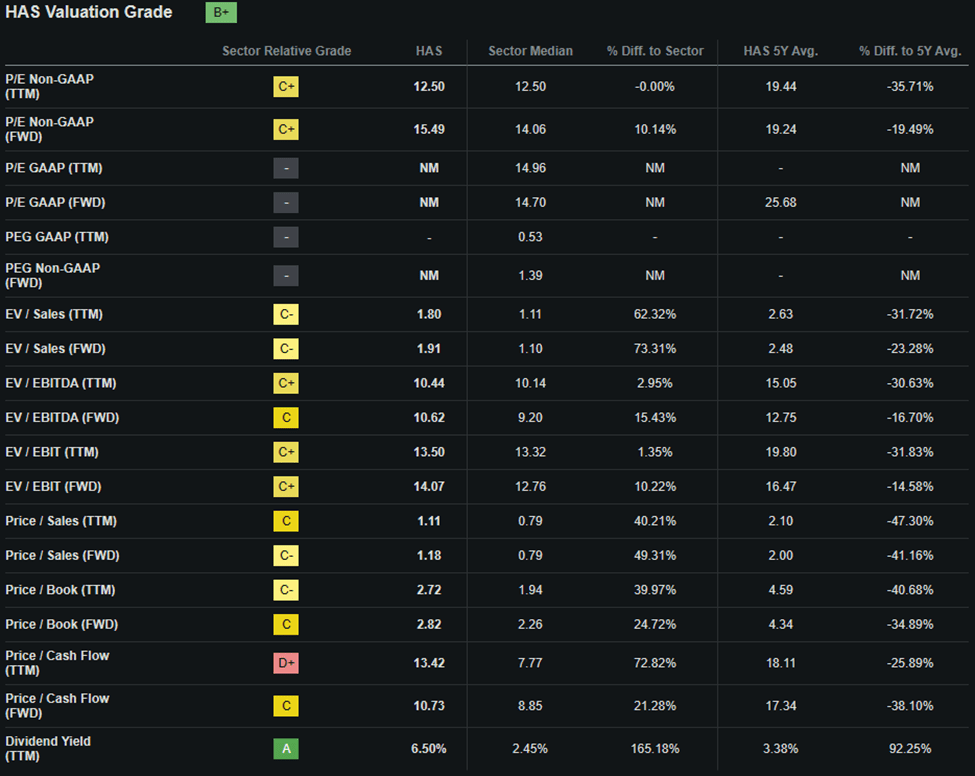

Seeking Alpha | HAS | Valuation

{kind=link}

Seeking Alpha’s Quant has assigned Hasbro with a “ B+ ” Valuation rating. I believe that this relative valuation is still a little pessimistic and fails to effectively illustrate the massive value present in Hasbro shares at current prices.

The firm is currently trading at a P/E non-GAAP FWD ratio of 15.49x and a P/CF ratio FWD of 10.73x. Their FWD Price/Book ratio is 2.82x and the firm’s EV/Sales FWD is 1.91x. While these metrics are not particularly low, Hasbro is currently trading at a P/S FWD ratio of just 1.18x.

To reiterate, Hasbro is trading at just 1.81x their projected 12-month total net sales.

Considering these relative quant valuation metrics, Hasbro appears to be somewhere between fairly valued and available at a modest discount.

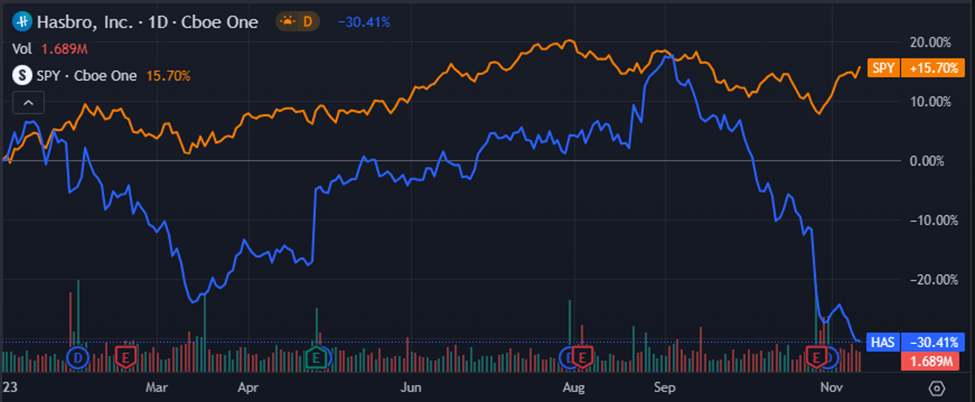

Seeking Alpha | HAS | Advanced Chart

{kind=link}

From an absolute perspective, Hasbro’s shares are available at a huge discount relative to previous valuations. YTD shares have fallen a whopping 30% underperforming the U.S. market as a whole by over 45%.

While the relative valuation provided by simple metrics and ratios along with the absolute comparison certainly appear to suggest Hasbro is currently undervalued, a quantitative value calculation must still be conducted.

The Value Corner

By utilizing The Value Corner’s specially formulated Intrinsic Valuation Calculation, we can better understand what value exists in the company from a more objective perspective.

By inputting Hasbro’s current share price of $43.11, an estimated 2024 EPS of $4.04, a realistic “r” value of 0.15 (15%) and the current Moody’s Seasoned AAA Corporate Bond Yield ratio of 5.13x into the formula, a base-case IV of $133.40 can be derived.

This would mean a whopping 68% undervaluation in shares is present.

When using a more pessimistic CAGR value for r of just 0.06 (6%) to reflect a scenario where Hasbro struggles to increase revenues and margins due to an acute recession limiting the spending power of consumers, shares are still valued at 40% discount relative to the current price of $43.00.

Considering these valuation metrics, absolute valuation and intrinsic value calculation, I believe Hasbro is trading soundly in Buffett-style fat pitch deep value territory.

Warren Buffett defines fat-pitches as rare, “no-brainer” opportunities which usually present themselves while the rest of the markets are panicking. Considering this definition, Hasbro definitely appears to fit the definition.

Still, in the short term (3-12 months), I find it difficult to say exactly what may happen to the stock. While the absolute destruction in shares prices means little downside potential should exist from a logical perspective, markets are inherently irrational mechanisms that sometimes result in illogical valuations.

An overall souring in investor sentiments regarding the U.S. economy as a whole could also see Hasbro shares struggle to rebound quickly.

In the long term (2-10 years), I see Hasbro strengthening their position at the forefront of toy industry. Their large scale, diverse set of hugely popular franchises and brands along with an increasingly lucrative digital presence should allow the firm to outpace its competitors and continue earning outsized returns on their invested capital.

Risks Facing Hasbro – Q3 FY23 Update

Little change has occurred to the risks racing Hasbro with the possibility for failed execution still remaining the main threat.

For a more detailed analysis of the risks facing the firm, I suggest reading my original article here .

While recent successes from their digital lineup have been excellent to see, Hasbro must continue to accurately target the wants and needs of consumers in order to guarantee long-term growth and profitability.

{kind=link}

From an ESG perspective, no tangible change has happened at Hasbro with the firm continuing to generate a positive ESG impact from their operations.

I still believe Hasbro makes for a great ESG conscious investment but of course recommend you conduct your own analysis into their ESG profile should this be of concern to you.

Summary

Hasbro continues to remain one of my favorite deep-value picks. Their fundamental profitability remains unharmed with the recent Q3 selloff screaming “fat pitch opportunity” to my ears.

The negative market sentiment surrounding their drop in revenues has ignored the adjusted increased in operating profits and margins while entirely discounting the success of recent digital releases.

I believe that the most recent Q3 results indicate Hasbro has successfully executed the first stage of their turnaround strategy with dropping costs and expanding margins illustrating this improvement.

A compromised macroeconomic landscape has led to what may initially appear as weak performance which further supports the hypothesis that a fat pitch opportunity may be present in shares.

This is compounded by the potential 68% undervaluation present in the stock.

Therefore, I continue to rate Hasbro a Strong Buy and have built a sizable 20% stake in the firm relative to my total portfolio value.

For further details see:

Hasbro: I See A Real Deep-Value Style Fat-Pitch Opportunity Here