HAS - Hasbro's Position As A Toymaking Leader Will Be Reinforced By Streamlining Efforts

2023-08-07 04:18:08 ET

Summary

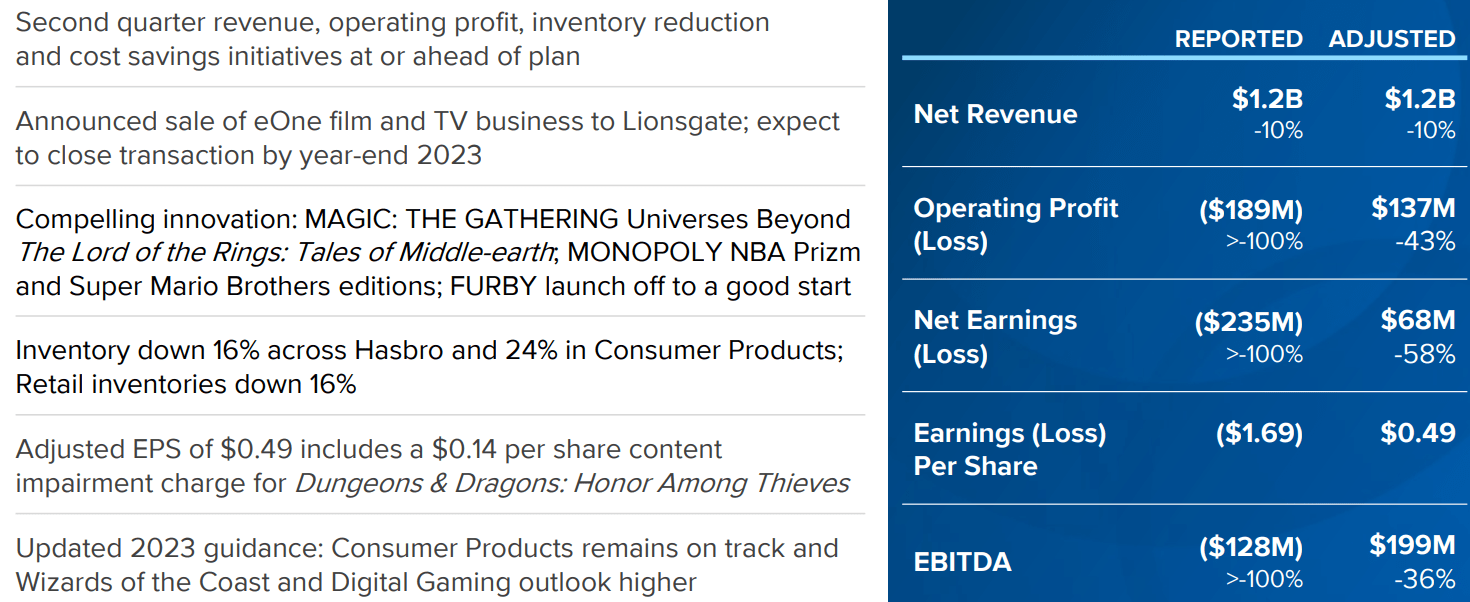

- Hasbro has achieved a 10% YoY decline in net revenues and a net loss of -$235mn in the past quarter.

- The company's long-run growth strategy focuses on executing its margin-focused 'Blueprint 2.0' and investing in ROE-rich growth drivers.

- Hasbro is undervalued by approximately 10% according to discounted cash flow valuation, with a fair value of $79.23.

Hasbro ( HAS ) is a Rhode Island-based toymaker and entertainment and gaming company. The firm is currently the owner of brands such as Magic: The Gathering, Nerf, My Little Pony, Transformers, Monopoly, Dungeons & Dragons, and so on.

{kind=link}

In the past quarter, Hasbro has achieved net revenues of $1.2bn- a 10% YoY decline- alongside a net loss of -$235mn, leading to an EBITDA of -$128mn.

Introduction

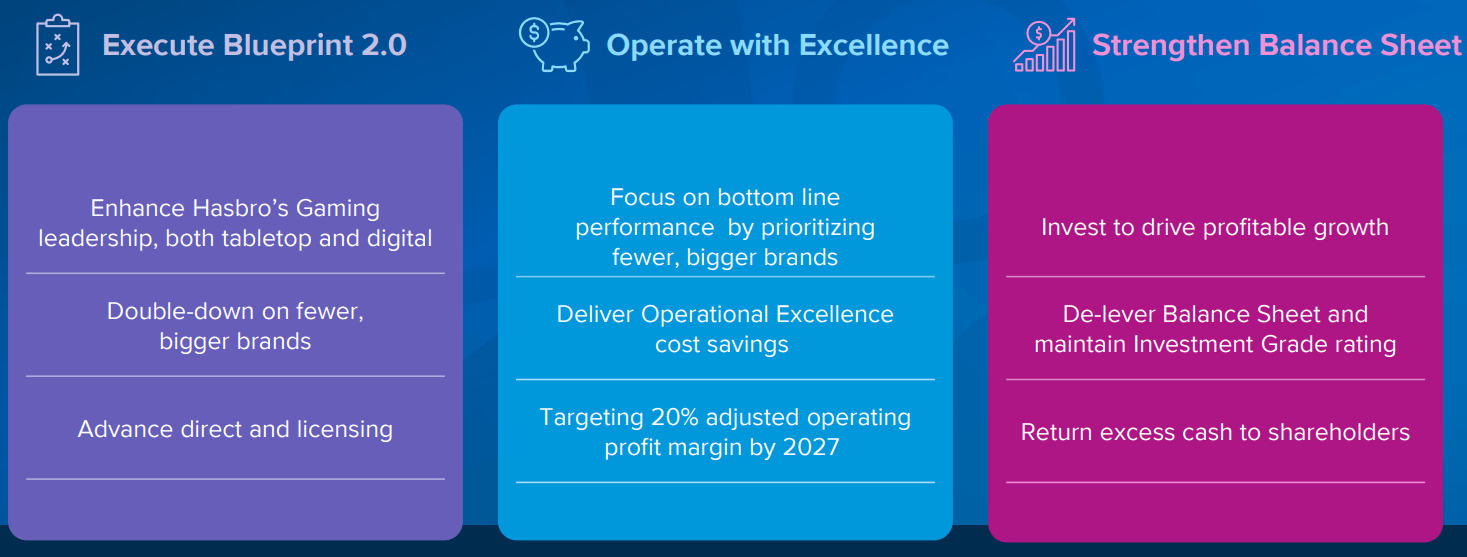

At the core of Hasbro's long-run growth strategy remains its threefold operational strategy, which encompasses the firm's dedication to executing its margin-focused 'Blueprint 2.0' by concentrating on a streamlined organization, ensuring efficient and effective operations through cost savings and expense base management, and a strengthened balance sheet by investing in ROE-rich growth drivers.

{kind=link}

The potential margin-expanding impact of this strategy, combined with the accretive sale of eOne to Lions Gate ( LGF ) and a moderate undervaluation lead me to rate the company a 'buy'.

Valuation & Financials

General Overview

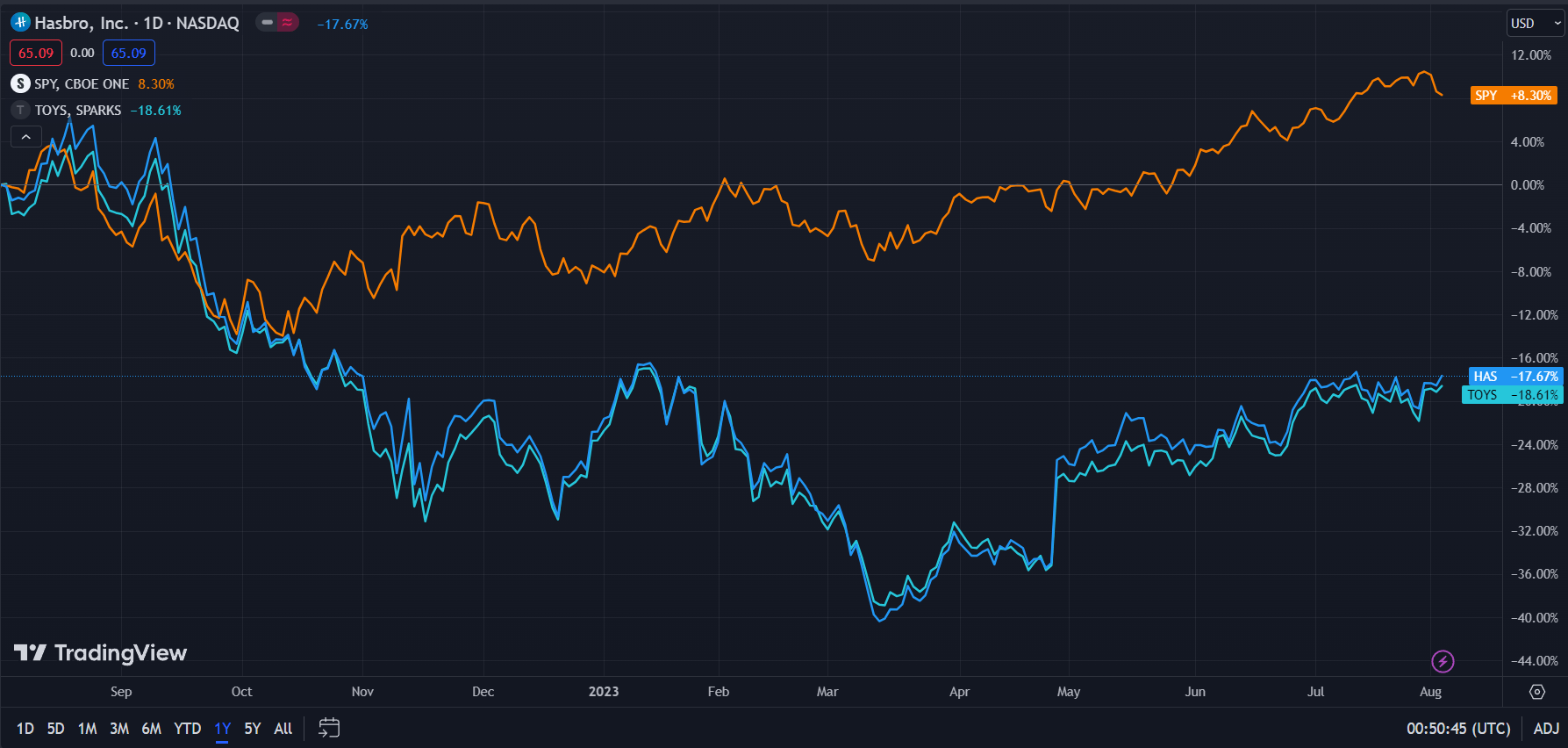

In the TTM period, Hasbro- down 17.67%- has experienced price action similar to TradingView's Toymakers Index- down 18.61%- and poorer to the broader market, as represented by the S&P 500 ( SPY )- up 8.30%.

{kind=link}

I believe the underperformance by both Hasbro and the toymaking industry is driven by the record highs otherwise experienced due to increased demand from COVID-19 and ensuing lockdowns.

That said, I believe Hasbro has significant room to grow due to operational capabilities and a solid value base.

Comparable Companies

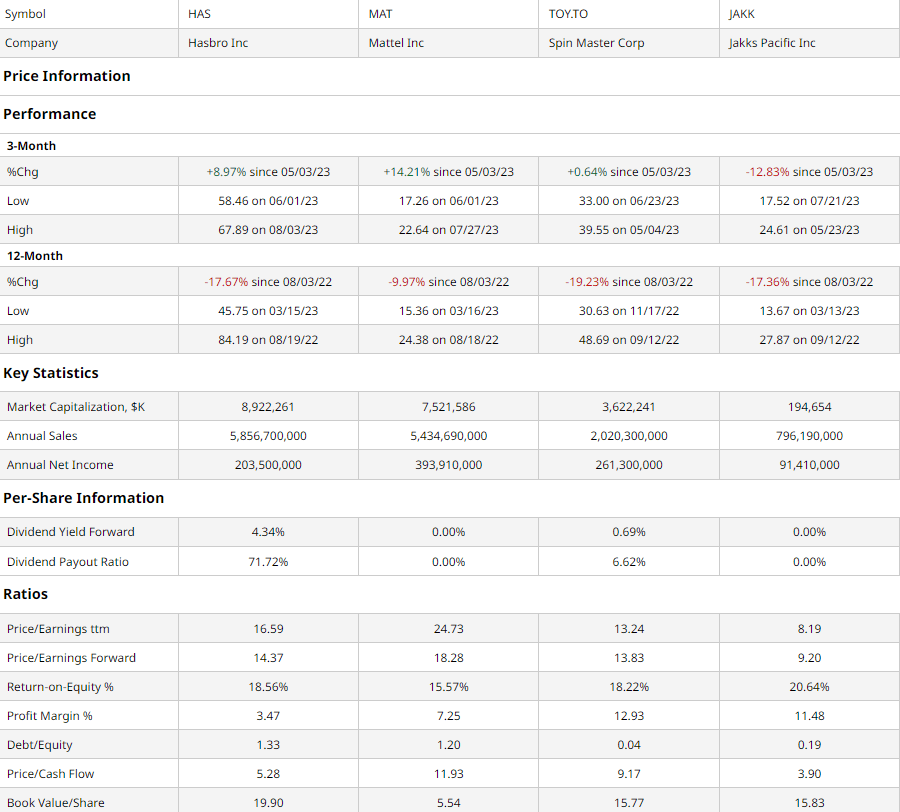

The toymaking industry remains highly consolidated, with a select few industry leaders generally owning major toy brands and persistently acquiring intellectual property and smaller brands. This group includes Hasbro's principal rival and the owner of Barbie and Hot Wheels, Mattel ( MAT ), Paw Patrol producer, Spin Master (TOY.TO), and action figure maker- among other things- JAKKS Pacific ( JAKK ).

{kind=link}

In the trailing 3-month period, Hasbro has experienced the second-best price action, behind only Mattel- itself spurred by the publicity of the Barbie movie- and enabled by the second-poorest yearly price performance.

Despite this, Hasbro maintains a strong position on a multiples basis and when addressing the firm's fiscal condition. For instance, Hasbro maintains the second-lowest P/CF alongside the second-highest ROE.

This works alongside the company's highest book value per share to ensure investors remain in a secure business.

Moreover, with the highest- by a significant margin- dividend of the peer group, investors can expect outsized returns from Hasbro's secure catalogue of IP.

Valuation

According to my discounted cash flow valuation, at its base case, the net present value of Hasbro is $71.17, meaning, at its current price of $63.75, the company is undervalued by ~10%.

My model, calculated over 5 years without built-in perpetual growth, assumes a discount rate of 10%, incorporating Hasbro's larger debt levels and higher sensitivity to macro events. Moreover, I projected an average revenue growth rate of 5%, lower than Hasbro's smoothed-out- to account for COVID-19 and subsequent anomalies- trailing 5Y revenue growth rate.

{kind=link}

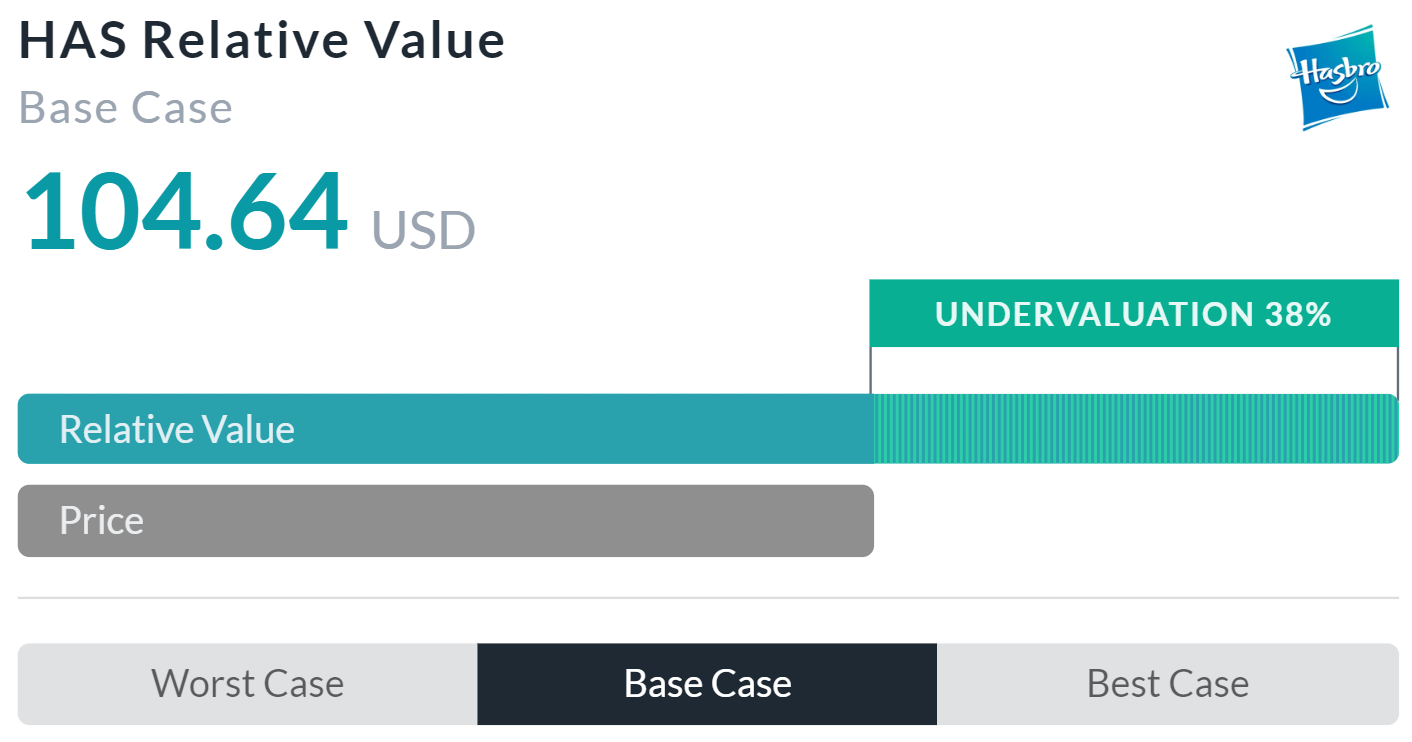

Alpha Spread's multiples-based relative valuation more than corroborates my thesis on undervaluation, estimating a base case undervaluation of 38%, with the company's relative value being $104.64.

However, Alpha Spread fails to adequately reflect Hasbro's true value, since the model does not discount growth multiples for dividends and fails to capture Hasbro's higher debt levels.

As such, using a weighted average of the company's NPV and relative value, skewed towards my DCF, the fair value of Hasbro is $79.23, with the stock undervalued by ~20%.

Divestment from eOne & Focus on Big Brands Supports Margin Expansion Efforts

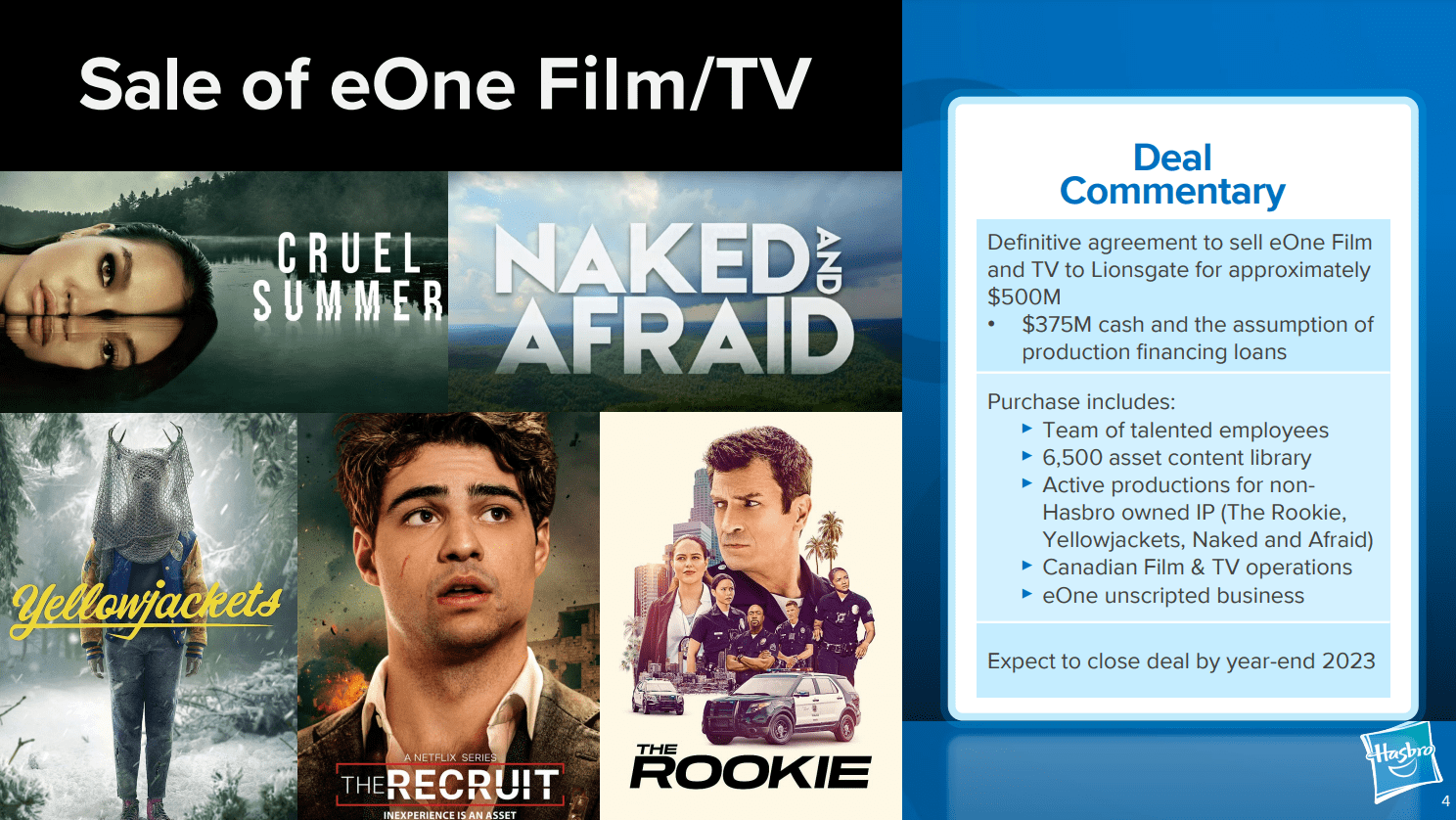

Hasbro's overall business objective in the medium term remains its efforts to streamline its operations and focus on bigger brand, virtuous cycle-inducing, integrative growth. The sale of Hasbro's eOne film and television segments manifests this sentiment, netting Hasbro $375mn in immediate cash injection and ensuring a laser-focus on core activities.

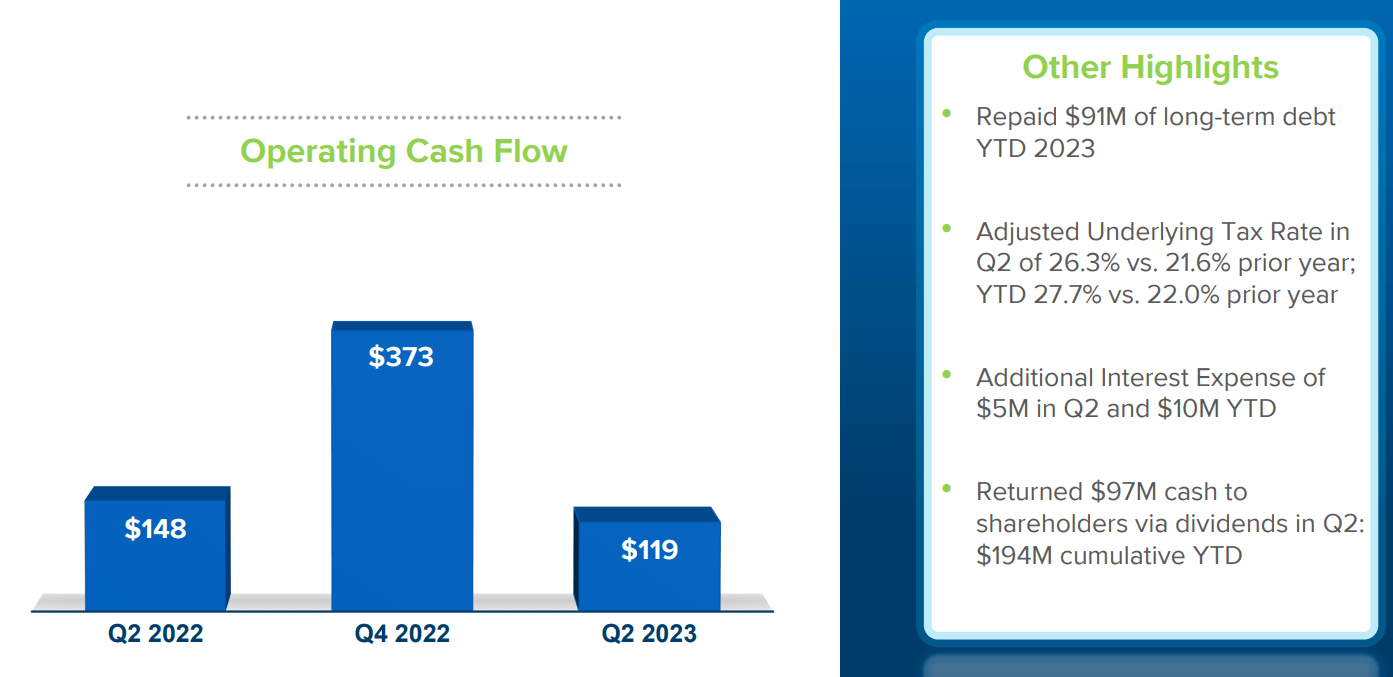

Beyond operations, Hasbro has additionally positioned itself for accelerated deleveraging efforts and greater reinvestment into existing brands.

{kind=link}

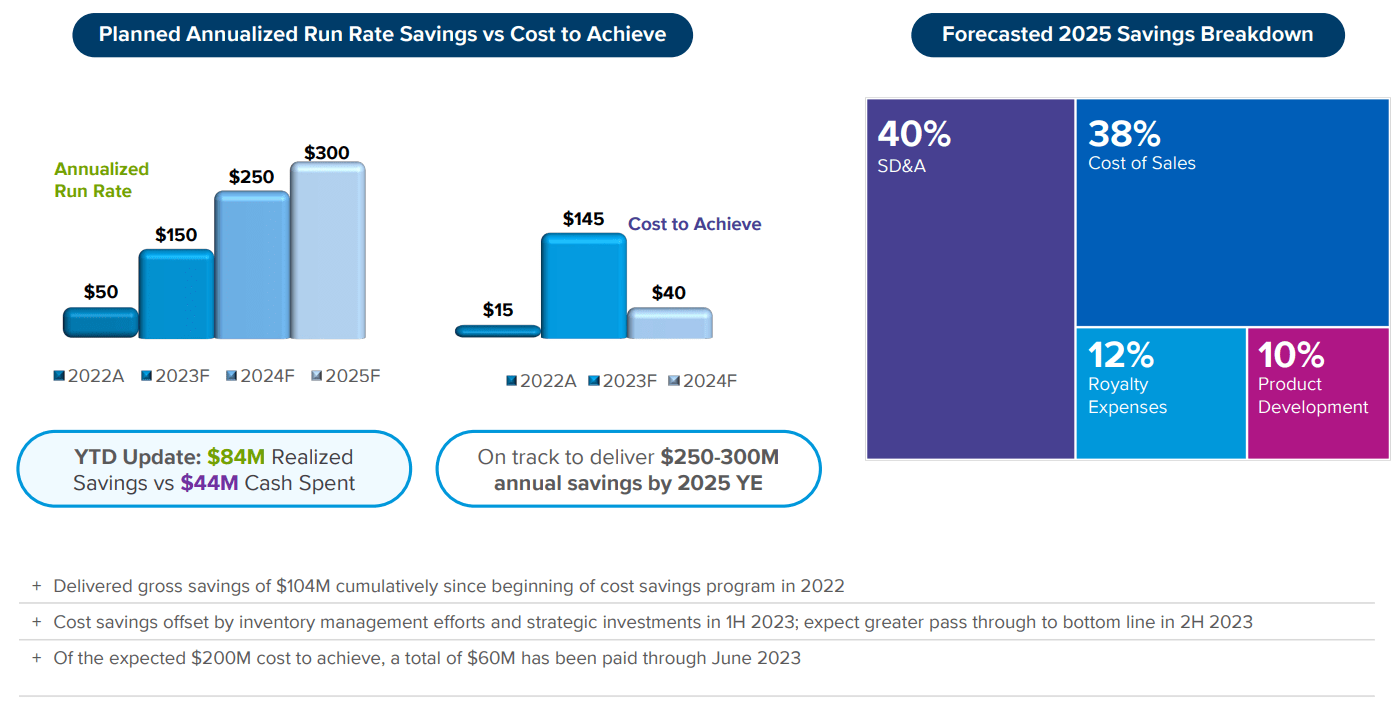

And apart from attaining a solid financial position, the key to sustaining it is a level of financial discipline and austerity, which starts with widening the firm's savings base and managing its expense structure. In doing so, Hasbro has managed to reduce the cost to achieve run-rate savings significantly, while increasing said savings structures. On a more granular level, Hasbro has dedicated itself to superior inventory management and reduced overhead related to non-core businesses.

{kind=link}

With these excess cash flows, investors can expect Hasbro to continually invest in core businesses, ensure long-run deleveraging, and return cash flows to investors through a peerless dividend program.

{kind=link}

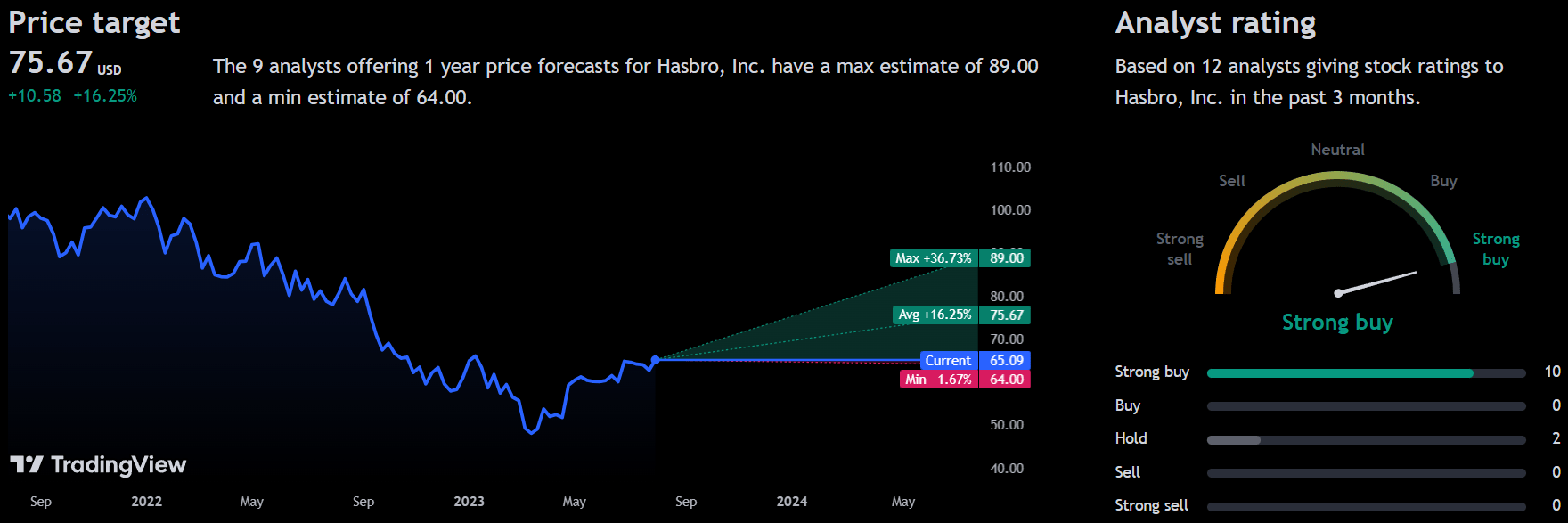

Wall Street Consensus

Analysts generally support my positive view of the company, projecting an average 1Y price target of $75.67, a 16.25% interest. This runs alongside general 'strong buy' sentiment.

{kind=link}

Even at the minimum projected price of $64.00, a 1.67% decline, investors can expect to remain positive due to Hasbro's dividend.

I believe analysts' overall positive sentiment reflects Wall Street's opinion that the market has overreacted to post-COVID financial decline and its durability.

Risks & Challenges

Rising Interest Rates Continue to Hamper Cost Base & Demand Levels

As aforementioned, among industry peers, Hasbro continues to maintain a dependence on debt to finance its activities. As such, with rising interest rates, Hasbro maintains a reduced ability to reinvest or return cash flows to investors. Moreover, as Hasbro's tabletop and digital games remain discretionary spending items, lagging consumer sentiment has resulted in a temporary recession for toy demand.

Long-Run Demand May be on a Downtrend

Regardless of temporary demand headwinds, Hasbro may be contending with long-run demand declines, as a result of aggressive digitalization of entertainment products and alternative segments experiencing greater growth- such as video gaming and such. Therefore, Hasbro must remain pragmatic in cost management efforts to reduce long-term uncertainties.

Conclusion

In the long run, Hasbro aims to become a more streamlined and nimble organization, mindful of its expense base and aggressively promoting its higher margin core business, to the benefit of its impressive dividend program and, thus, investors.

For further details see:

Hasbro's Position As A Toymaking Leader Will Be Reinforced By Streamlining Efforts