HVT - Haverty: A Solid But Overvalued Company In A Lackluster Market

Summary

- Haverty Furniture Companies maintains a stable performance despite the moderating market demand.

- Its impressive liquidity position helps suffice its capacity and withstand headwinds.

- Market prospects are less robust than in 2021-2022 but still decent.

- Dividend payouts remain attractive, given the sustained growth and yields.

- The stock price uptrend is evident but seems too high for its fundamentals.

It’s been quite a while since I first covered Haverty Furniture Companies, Inc. (NYSE: HVT). In the following quarters, it has remained an ideal dividend stock. Its fundamentals remained solid with enticing dividend yields. Indeed, its existence for over a century can speak a lot about its solid reputation.

Today, Haverty remains a strong company with impressive revenues and margins. Despite this, HVT must stay on the watch as market demand softens. The market starts to clear supply chain bottlenecks. Thankfully, it has a solid financial positioning against macroeconomic headwinds. Cash reserves are adequate to maintain its liquidity position. It may not have to raise financial leverage to cover its current capacity.

Moreover, dividend payouts are consistent with impressive yields. However, HVT's stock price is too much for the company's intrinsic value.

Company Performance

The home furnishing retail industry has dramatically changed in the last two years. Disruptions escalated from restrictions that resulted in a deep recession. Despite this, home furnishing manufacturers and retailers proved their resilience. They regained their footing in a short period. Thanks to the massive price decreases, hybrid work setups, and property boom. All these led to a favorable shift in consumer behavior.

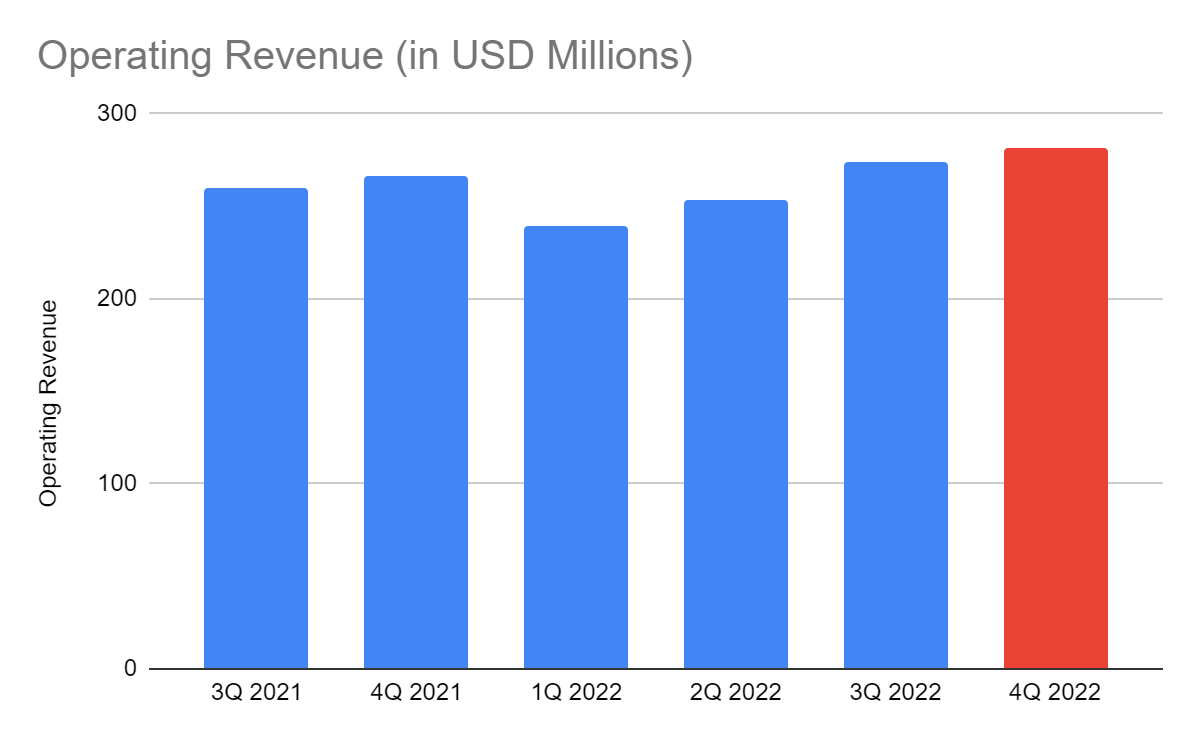

Today, Haverty shows it can withstand market blows as it surpasses pre-pandemic performances. The 3Q operating revenue amounted to $274.5 million , a 5% year-over-year increase. Indeed, it’s nice to see HVT sustaining revenue growth amidst the moderating demand. We can see its sequential decrease since 1Q 2022. But given the current changes, we must observe its near-term performance. We can attribute these positive results to various factors.

Operating Revenue (MarketWatch And 4Q Author Estimation)

{kind=link}

First, its efforts to raise sales manifested in its enhanced operating capacity. It allowed HVT to deliver backorders, given the high container volumes from vendors. It was evident in 3Q as customers returned to traditional shopping patterns. After all, Labor Day is often one of the peak periods during the third quarter. We can also notice that there has been a 7.2% decrease in written business. Yet, it was still 16% higher than in 3Q 2019. It proved the maintained capacity of the company to navigate a high-inflation environment. Also, the industry sees the end of supply chain bottlenecks. This scenario may indicate the normalizing demand. It may become more evident this year.

Second, Haverty maintains the balance between revenue growth and fundamental stability. For instance, it avoids carrying too high inventories amidst the softening demand. HVT's inventory levels remain manageable on the Balance Sheet. It can easily adjust retail volumes to prevent or reduce the risk of overloading. This aspect gives it increased flexibility in its pricing strategy. So despite the lower volume, it set favorable prices during 3Q peak periods.

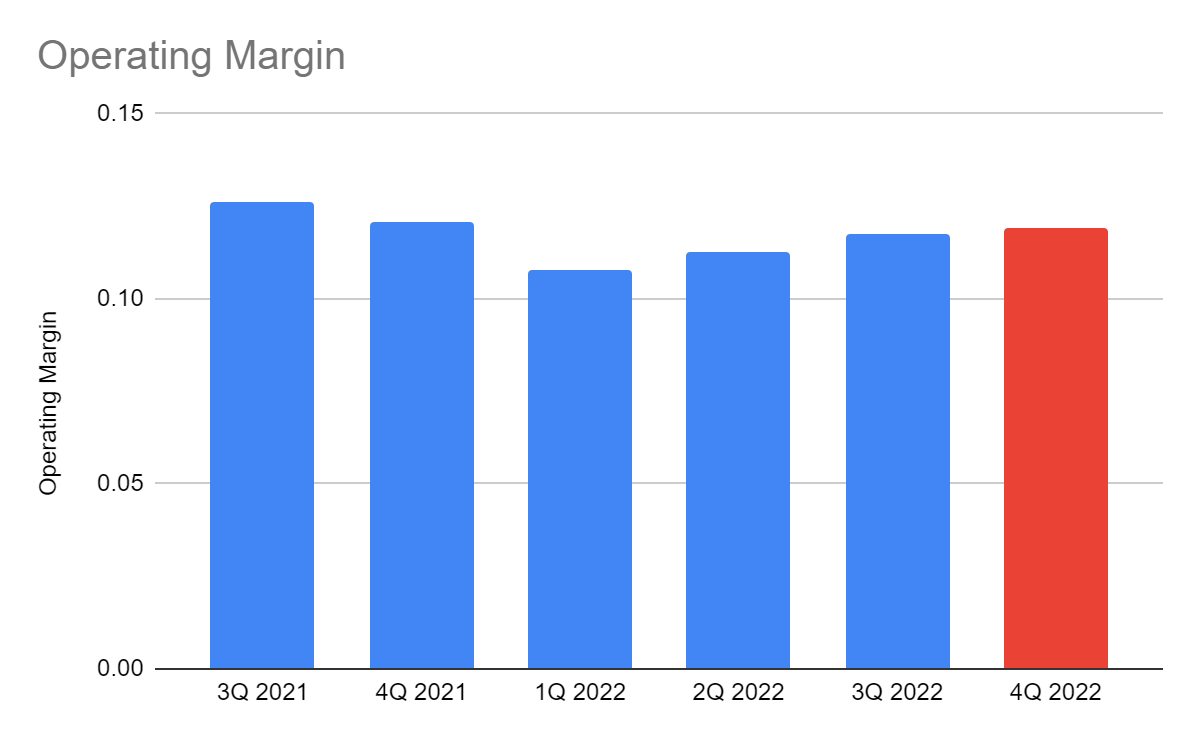

Moreover, Haverty manages its costs and expenses amidst higher price levels well. It keeps its operational efficiency to stabilize margins. The increase in 3Q was still manageable and proportionate to revenues. And even if these were not enough to raise margins, viability remained well-managed. Its operating margin was still impressive at 11.7% versus 12.7% in 3Q 2021. Also, the sequential increase from 1Q at 10.8% and 2Q at 11.2% was evident. With that, the company's core operations generated stable returns to sustain its capacity. This attribute may help HVT cushion the blow of the expected economic downturn.

In 4Q 2022, I believe the demand continued to soften. It is consistent with the company’s expectations amidst inflation. So to be more conservative, I based my estimated 4Q revenue and margin on historical quarterly averages. And as demand continues to normalize, it may have less flexible pricing strategies. As such, near-term patterns may not be robust as they were in 2021-2022. Even so, HVT can stay viable as inflation continues to relax. Transporting and distributing inventories may be cheaper. It may continue executing its cost-reduction strategies if it keeps inventory levels manageable.

Operating Margin (MarketWatch And 4Q Author Estimation)

{kind=link}

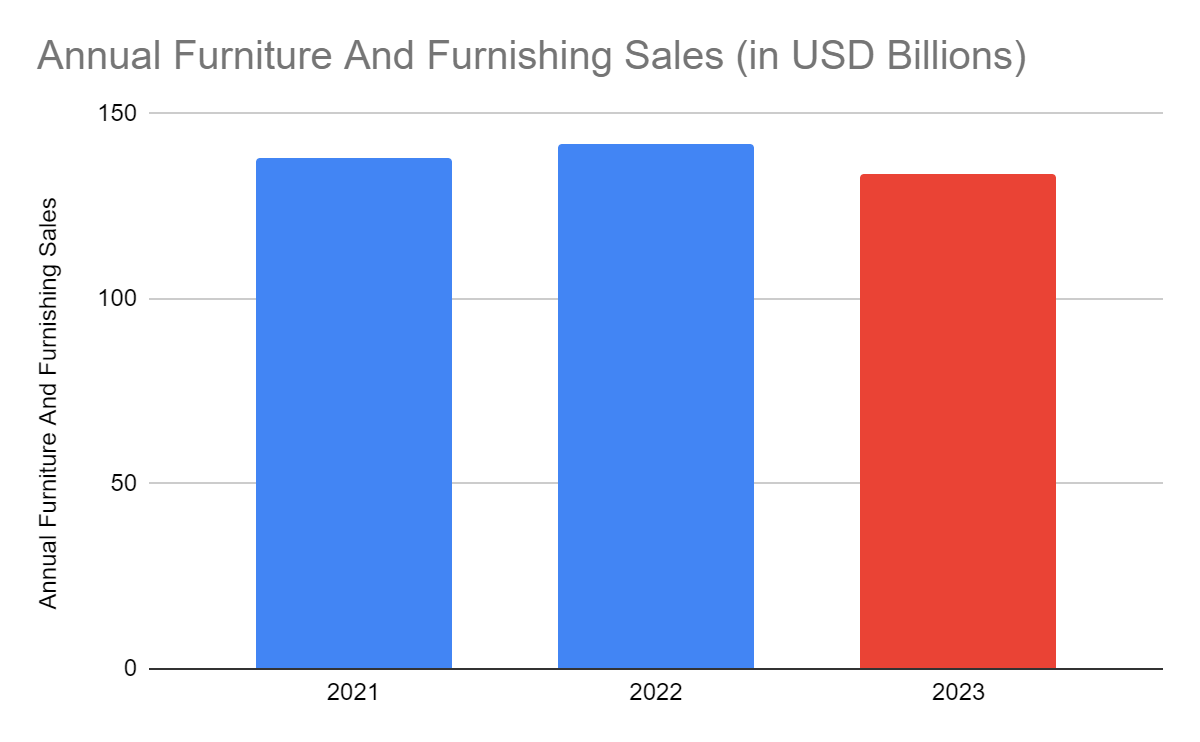

What matters is that HVT remains consistent with the industry as a whole. The twelve-month total sales in the furniture industry reached $143.43 billion , up by 4% from 2021. This year, industry sales may also keep cooling down. This view is consistent with the cooling demand expectations this year. Also, we can see that the monthly sales decreased in 2022. In December, sales showed a 0.3% year-over-year growth but 2.5% lower than in November 2022. Given the current industry demand pattern, the downtrend may continue. Hence, HVT sales may follow its direction.

Annual Furniture Sales (FurnitureToday)

{kind=link}

How Haverty Furniture Companies, Inc. May Fare This Year

Haverty Furniture Companies, Inc. remains a durable figure in home furnishing. In over a century, it has already overcome many market downs. It has already established its reputation as a resilient and secure stock. Despite this, it must beware of the changing market dynamics this year. On a lighter note, inflation continues to relax at 6.5%. I am still optimistic despite the potential economic downturn. After all, the 2022 inflation was more of a demand-pull, not a cost-push. We can also confirm the unemployment rate, which differs from the Great Recession. So, mixed inflation decreases, and stable income levels may strengthen purchasing power.

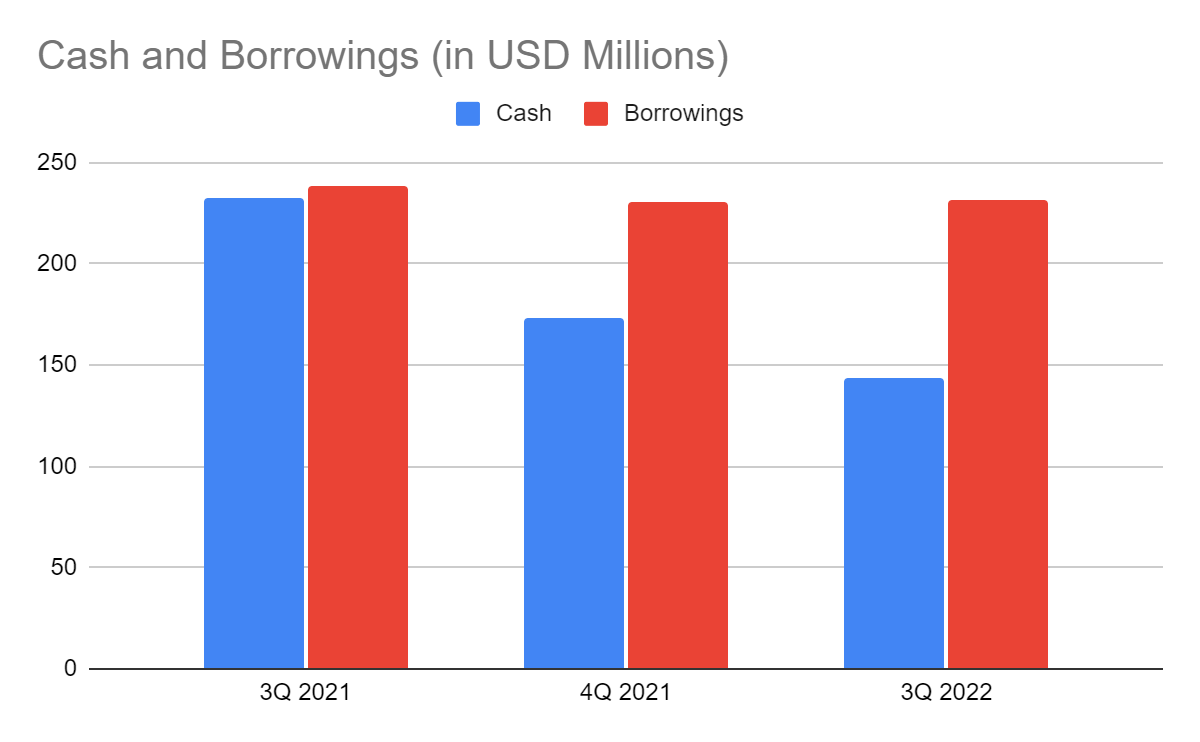

But what makes Haverty solid is its excellent financial positioning. We already discussed its stable inventory levels that could help maintain operational efficiency. Aside from that, liquidity stays in impeccable shape. Its adequate cash reserves are one of its cornerstones. Meanwhile, borrowings are slightly decreasing. Given this, its Net Debt/EBITDA ratio remains low at 2.43x. Haverty is earning enough to cover borrowings. It is an essential aspect since HVT is a capital-intensive company. So, it needs more cash to sustain its capacity. And by the looks of it, the company is still excellent and sustainable.

Cash And Equivalents And Borrowings (MarketWatch)

{kind=link}

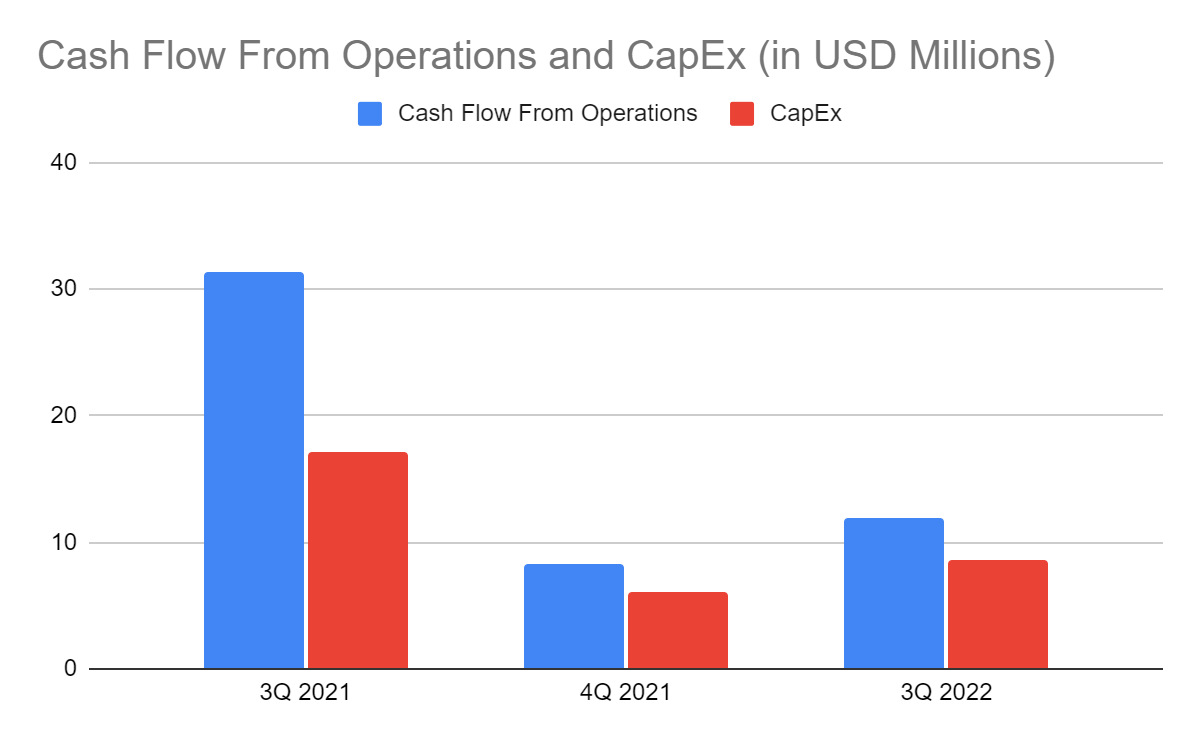

We can verify it by the free cash flow ("FCF") from operations. It amounts to $11.9 million, which is only 30% of the value last year. Even so, it is still enough to cover CapEx, giving an FCF of $3.4 million. With all this information, HVT has enough means to suffice borrowings and dividends. It can also use more cash to improve its intrinsic value by repurchasing shares.

Cash Flow From Operations And CapEx (MarketWatch)

{kind=link}

Stock Price Assessment

The stock price of Haverty Furniture Companies, Inc. sustains its uptrend. It should not be surprising, given its stable fundamentals. At $35, it has already increased by 30% from my previous coverage. However, the continued uptrend already seems excessive. The price-earnings multiple of 6.8x and my estimated EPS of 4.50 gives a target price of $30.6. Meanwhile, NASDAQ estimates EPS at $4.35 , which leads to a target price of $29.58. Likewise, projections using the PTBV ratio convey potential overvaluation. It has a BVPS of 17.56, better than the average in recent years. But given the price, its PTBV ratio of 1.99x is higher than the average of 1.87x. If we use the current BVPS and the average PTBV ratio, the stock price will be $32.76.

Despite this, HVT is an impressive dividend stock with a yield of 3.2%. It is way better than the S&P 600 average of $1.36%. It is also sustainable, given the dividend payout ratio of 20%. To assess the stock price better, we will use the discounted cash flow, or DCF, Model.

FCFF $31,500,000

Cash $143,980,000

Borrowings $231,500,000

Perpetual Growth Rate 4.8%

WACC 9.2%

Common Shares Outstanding 16,148,000

Stock Price $35

Derived Value $32.17.

The derived value confirms the potential overvaluation. There may be a 9% downside in the next 12-18 months. Investors must beware of the risks before buying HVT shares.

Bottom Line

Haverty Furniture Companies, Inc. is still solid despite the lackluster market patterns. Its core operations are stable and viable, so it can withstand headwinds. It has excellent liquidity that helps it sustain its capacity and cover dividends. However, the Haverty Furniture Companies, Inc. stock price is high for its intrinsic value. The recommendation, for now, is that Haverty Furniture Companies, Inc. is a hold.

For further details see:

Haverty: A Solid But Overvalued Company In A Lackluster Market