HVT - Haverty Furniture And Its Real Value

2023-06-26 06:04:26 ET

Summary

- Haverty Furniture benefitted from the stay-at-home trend during the pandemic that boosted revenue for home improvement products like home furnishings.

- Haverty Furniture has produced impressive EPS growth over the past five years and recently increased its quarterly dividend.

- Despite increases in share prices, Haverty Furniture shares may still be undervalued.

- This article focuses on the fundamentals, the real value versus the current share price, and if Haverty Furniture stock is currently worth investing in.

While Haverty Furniture ( HVT ) has reported stellar results in the past few years, its most recent first quarter result for 2023 revealed a decline in EPS and a decline in sales compared to first quarter 2022. Haverty Furniture CEO Clarence H. Smith acknowledged headwinds included spending patterns for consumers and inflationary pressures. The CEO noted a reduction in traffic and acknowledged that the Company is likely to transition from an explosive growth during the COVID pandemic to a more stable and consistent growth in 2023 and in the future.

While sales are down, Haverty Furniture has seen positive news on its average sale size, which the Company believes is driven by its growing free design service . Mr. Smith is confident that quality design and sales services are a differentiator for Haverty Furniture. Special orders which are priced higher have become a key factor to the Company's strategy, and new outdoor furniture lines are expected to help boost sales growth.

Additionally, Haverty Furniture announced a 7.1% increase in its quarterly dividend, which shows that the Company is confident it can drive cash flows and provide value to investors. The Company has paid dividends since 1935 and its dividend yield is much higher than the S&P 500 average.

When considering these current stories about Haverty Furniture, we need to determine which news topics will have a long-term and ongoing effect on the Company and its share price. While the drop in sales is a worrisome development, the Company strongly believes that it can continue to grow. Conversely, Haverty Furniture's free design service, quality product, and growing product line will provide long-term benefits. In addition, its strong dividend provides a return to investors even when HVT stock price does not appreciate.

While current news stories, good or bad can sway our opinion about investing in a company, it's good to analyze the fundamentals of the company and to see where it's been in the past and in which direction it's heading.

This article will focus on the long-term fundamentals of the company, which tend to give us a better picture of the company as a viable investment. I also analyze the value of the company versus the price and help you to determine if HVT is currently trading at a bargain price. I provide various situations which help estimate the company's future returns. In closing, I will tell you my personal opinion about whether I'm interested in taking a position in this company and why.

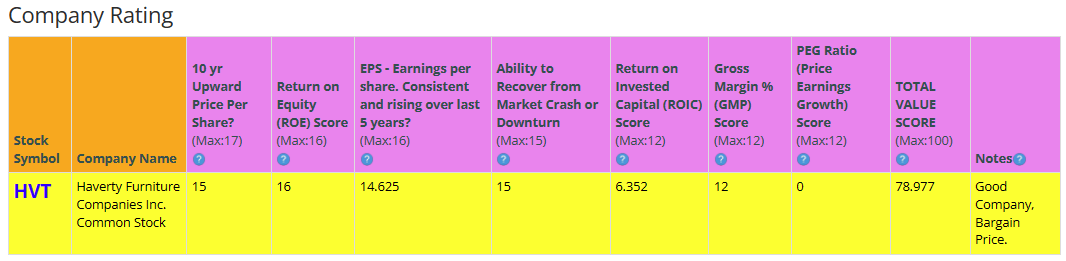

Snapshot of the Company

A fast way for me to get an overall understanding of the condition of the business is to use the BTMA Stock Analyzer's company rating score. HVT has a good company rating score of 79.0 out of 100. In summary, HVT seems to have above average fundamentals since all but two categories produce good scores.

Before jumping to conclusions, we'll have to look closer into individual categories to see what's going on.

{kind=link}

Fundamentals

Let's examine the price per share history first. In the chart below, we can see that price per share remained relatively stable from 2014 until 2021, when the stock experienced a huge increase in price during the COVID pandemic. After a decline in 2022, the stock has increased again in 2023. Overall, share price average has grown by about 116.98% over the past 10 years or a Compound Annual Growth Rate of 8.98%. This is a decent return for this period, but the concerning realization is that most of this price growth was achieved during the COVID surge.

BTMA Stock Analyzer

Earnings

Looking closer at earnings history, we see that earnings tell a story similar to the price history of the stock. Earnings are relatively flat in the years leading up to 2020, and then show significant growth through the past three years.

Haverty Furniture is a full-service home furnishings retailer with a wide selection of merchandise in the middle to upper-middle price ranges, and its earnings story mirrors that of companies who benefited from COVID-19 lockdowns and the benefits of consumers spending more time at home. Home improvement was one category that outperformed during the pandemic as people invested more in their homes. While this trend had positive lift for Haverty, as the pandemic wanes it is expected that spending on home furnishings will decline. A secondary threat faces Haverty as increasing mortgage interest rates could slow new home sales and in effect, sales of new furniture.

On the other hand, Haverty operates over 100 showrooms in the Southern and Midwestern regions. If consumers coming out of the pandemic demand an in-person experience with a high degree of touch, Haverty sales may remain strong.

BTMA Stock Analyzer

Since earnings and price per share don't always give the whole picture, it's good to look at other factors like the gross margins, return on equity, and return on invested capital.

Return on Equity

The return on equity has strongly increased in the period from 2018 to 2022. While ROE sat at around 10% in 2018, that number has increased to above 30%, and average ROE is a strong 22% over the past 5 years. For return on equity (ROE), I look for a 5-year average of 16% or more. So, HVT easily meets my requirements, but my concern is that ROE will fall back to normal levels of 8 to 10, as the COVID effect subsides.

BTMA Stock Analyzer

Let's compare the ROE of this company to its industry. The average ROE of 32 Furniture/Home Furnishing companies is 5.45%.

Therefore, HVT's 5-year average of 22.06% is well above average, and current ROE of 32.77 is stellar.

Return on Invested Capital

The return on invested capital has also seen a strong increase from 2018 to 2022. ROIC grew nearly 9% during the period, and the 5-year average ROIC is around 12.70%. For return on invested capital ((ROIC)), I also look for a 5-year average of 16% or more. So, even with historical growth, HVT does not pass this test.

BTMA Stock Analyzer

Gross Margin Percent

Gross margin percent ((GMP)) has also increased over the last five years. GMP fell in 2018, but then increased each year since then. Overall gross margin percent is at very high levels, with a 5-year GMP around 55.84%. I typically look for companies with gross margin percent consistently above 30%. Even in its weakest year, GMP was above 54.0%, so HVT has proven that it has the ability to maintain acceptable margins over a long period.

BTMA Stock Analyzer

Financial Stability

Looking at other fundamentals involving the balance sheet , we can see that the debt-to-equity is less than 1. This is a positive indicator, telling us that the company owns more than it owes.

HVT's Current Ratio of 1.79 is satisfactory, indicating it has an adequate ability to use its assets to pay its short-term debt. Ideally, we'd want to see a Current Ratio of more than 1, so HVT exceeds this amount.

According to the balance sheet, the company appears to be in good financial health. In the long term, the company has more than enough assets to cover its debts. In the short-term the company is generating enough cash flow, to fulfill its obligations.

HVT has also paid a regular dividend since 1935, and its dividend yield is nearing 4.0%. The company recently announced an increase to its quarterly dividend.

{kind=link}

This analysis wouldn't be complete without considering the value of the company vs. share price.

Value Vs. Price

The company's Price-Earnings Ratio of 6.15 indicates that HVT might be selling at a bargain price when comparing HVT's PE Ratio to a long-term market average PE Ratio of 15.

The 10-year and 5-year average PE Ratio of HVT has typically been 18.1 and 11.7, respectively. This indicates that HVT could be currently trading at a low price when comparing to its average historical PE Ratio range.

{kind=link}

The Estimated Value of the Stock is $42.74, versus the current stock price of $28. This indicates that HVT is currently selling at a bargain price.

For more detailed valuation purposes, I will be using a diluted EPS ttm of 4.88. I've used various past averages of growth rates and PE Ratios to calculate different scenarios of valuation ranges from low to average values. The valuations compare growth rates of EPS, Book Value, and Total Equity.

In the table below, you can see the different scenarios, and in the chart, you will see vertical valuation lines that correspond to the table valuation ranges. The dots on the lines represent the current stock price. If the dot is towards the bottom of the valuation range, this would indicate that the stock is undervalued. If the dot is near the top of the valuation line, this would show an overvalued stock.

BTMA Wealth Builders Club BTMA Wealth Builders Club

According to the valuation analysis based on forward growth, HVT is overpriced.

In my opinion, it's more important to focus on the forward growth valuation of HVT because negative earnings growth of around -22% to -26% is being forecast between now and the end of the year. In addition, earnings may gravitate back to normalized levels since the COVID surge has subsided and inflation and consumer spending cutbacks could also reduce earnings.

In summary, this forward growth analysis shows an average valuation range of around $18 to $24 per share versus its current price of about $28, this would indicate that HVT is overpriced.

Summarizing the Fundamentals

According to the facts, Haverty Furniture is financially healthy in a long-term sense in having enough equity as compared with debt, and in the short-term because the current ratio indicates that it has plenty of cash to cover current liabilities.

This company experienced recent growth in earnings through the pandemic, raising EPS from around 1 to above 5.

Other fundamentals including ROE and Gross Margin are at excellent levels. The only downside of the fundamentals is that although ROIC has grown, it did not pass my test of being above 16%. If the company can continue its strong growth over the past few years, the ROIC metric may rise above 16%.

While Haverty Furniture metrics look stellar, another consideration is that the Company's strong performance began during the COVID pandemic when home furnishings were a priority for many consumers. Recent sales in early 2023 showed signs of slowing growth for the Company, which may be the result of higher mortgage rates, the effect of the ending pandemic, or the combination of the two factors.

As a result, we need to keep an eye on future earnings to see if the exaggerated earnings growth from COVID falls back down to normalized earnings levels seen prior to the pandemic.

In terms of valuation, my forward growth analysis shows that the stock is overpriced.

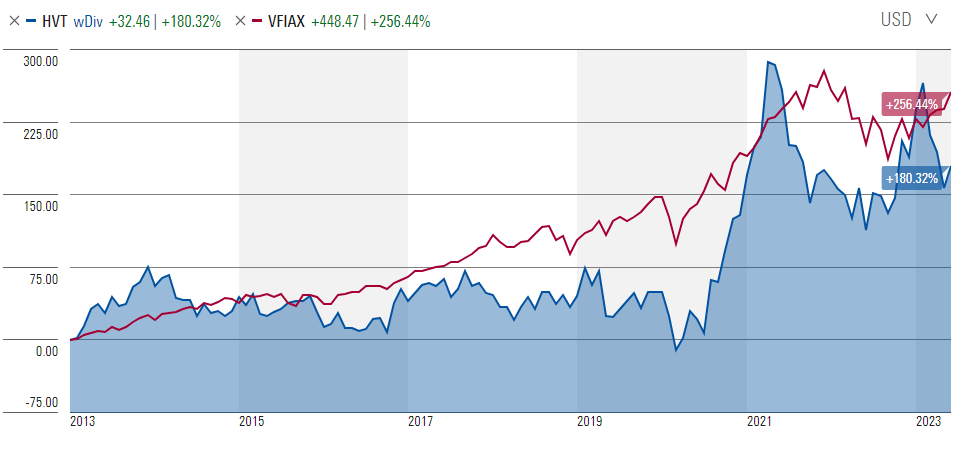

HVT Vs. The S&P 500

Now, let's see how HVT compares versus the US stock market benchmark S&P 500 over the past 10 years. From the chart below, we can see that HVT has underperformed the market benchmark during a majority of the time. In addition, HVT is more volatile than the S&P 500. At times, HVT had more pronounced gains or losses than the benchmark. This tells me that in most cases, I would be better off investing the more consistent, better performing, and more diversified S&P 500 rather than investing in HVT.

However, because of HVT's financial stability and solid fundamentals, it could be a decent investment to buy if it's offered at a low bargain price to capitalize on a short-term gain. HVT's significant dividend at over 4%, could also help to sweeten the deal.

{kind=link}

Forward-Looking Conclusion

Over the next five years, the analysts that follow this company are expecting it to grow earnings at an average annual rate of 13.10% .

In addition, the average one-year price target for this stock is at $40.50 , which is about a 45% increase in a year.

The Expected Annual Compounding Rate of Return is 18.13%.

Does Haverty Furniture Pass My Checklist?

- Company Rating 70+ out of 100? YES (79.0)

- Share Price Compound Annual Growth Rate > 12%? NO (9%)

- Earnings history mostly increasing? NO (EPS was flat until COVID)

- ROE (5-year average 16% or greater)? YES (22%)

- ROIC (5-year average 16% or greater)? NO (13%)

- Gross Margin % (5-year average > 30%)? YES (56%)

- Debt-to-Equity (less than 1)? YES

- Current Ratio (greater than 1)? YES

- Outperformed S&P 500 during most of the past 10 years? NO

- Do I think this company will continue to successfully sell their same main product/service for the next 10 years? YES

Haverty Furniture scored 6/10 or 60%. Although there are some weak areas (periods of flat earnings and low ROIC), Haverty Furniture is worth considering as a potential investment.

Is Haverty currently selling at a bargain price?

- Price Earnings less than 16? YES (6)

- Is HVT's Value greater than Current Stock Price? NO (Value $18 to $24 < $28 Stock Price)

Valuation metrics are mixed. But I feel that COVID definitely inflated earnings and the valuation. Moving forward, the earnings will likely fall to more normalized numbers. Therefore, I am focusing more on the conservative valuation based on the future EPS negative growth forecasts.

Haverty has a lot of good things going for it. It's heavy on cash, has a history of great margins, and a history of stable earnings prior to COVID. As earnings normalize, a further drop in earnings and share price could be expected.

At this time, I'm willing to add Haverty to my watchlist, and if the market offers it for a ridiculously low bargain price, then I will snatch it up to make some short-term gains. If the stock price falls more after my purchase, I can still be confident that I bought a solid company at a bargain price, and I'll just wait patiently for the stock to return to its real value. While waiting, I will gladly collect HVT's dividend of more than 4%.

For further details see:

Haverty Furniture And Its Real Value