HVT - Haverty Furniture: Still Not The Best Time To Go Long

2023-09-27 02:31:37 ET

Summary

- The company's revenue decreased by 18.5% YoY, while operating margin reached 7.2%.

- A decrease in traffic due to pressure on consumers from macro factors has a negative impact on comparable sales.

- I expect pressure on financial performance to continue in the coming quarters, so my recommendation is hold.

Introduction

Shares of Haverty Furniture ( HVT ) have risen 18% YTD. Despite the fact that the stock is relatively inexpensive based on multiples, I believe it is still not the best time to go long. In my article, I would like to analyze current business trends and share my own expectations about future financial results.

Investment thesis

I believe the company's operating and financial performance will continue to be under pressure in the coming quarters. First, I don't expect we'll see a quick rebound in store traffic even if inflation slows because consumers will continue to face higher daily costs. Secondly, while the company continues to effectively pass on higher inflation rates to the end consumer, I believe that the decline in scale effects will continue to have a negative impact on the business's operating margins. Thus, despite the attractive valuation, I do not see additional catalysts for the stock's growth.

Company overview

Haverty Furniture sells residential furniture, home furnishing, mattress and accessories. The main sales channel is offline. As of the 2nd quarter of 2023, the company operates 122 showrooms in 16 states. The company operates in the US market.

2Q 2023 Earnings Review

The company has been a beneficiary of rising demand for household goods during Covid restrictions, but currently revenue growth rates are under pressure as: 1) real consumer incomes are declining due to increased inflation, while the availability of credit instruments is declining due to rising interest rates 2) current financial results are compared with a relatively high historical base 3) people began to spend less time at home as Covid restrictions were lifted

{kind=link}

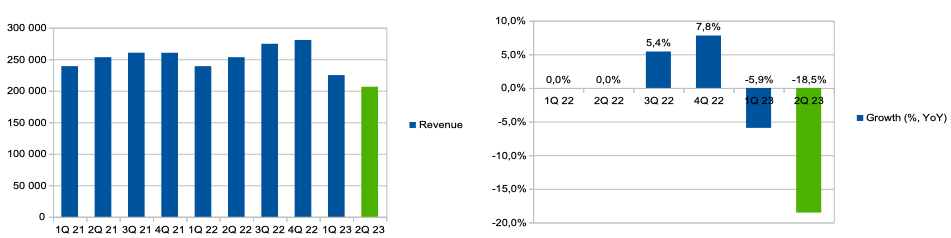

The company reported worse than investors expected . The company's revenue decreased by 18.5% YoY due to a decrease in comparable sales by 19.1%. The company continues to face declining traffic in its stores due to pressure on consumers from macro headwinds. Gross profit margin increased from 57.9% in Q2 2022 to 60.5% in Q2 2023 due to lower freight costs and lower production costs.

Gross profit margin (Company's information)

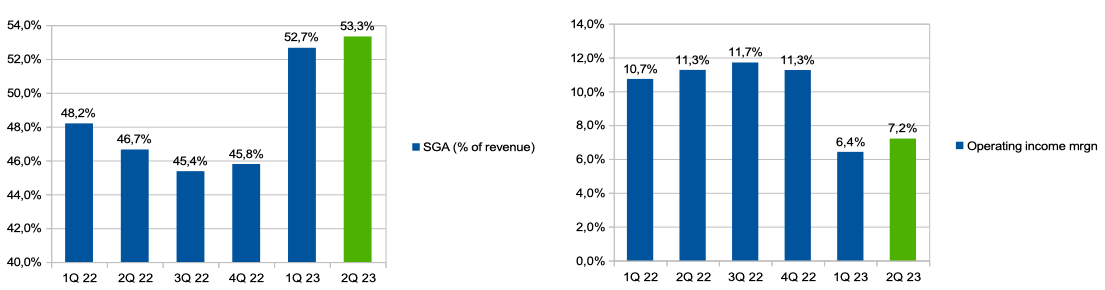

SGA expenses (% of revenue) increased from 46.7% in Q2 2022 to 53.3% in Q2 2023. I believe that the increase in operating expenses is associated with the deleverage effect due to the decrease in business scale, because the share of fixed expenses account for about 63% of SGA expenses.

{kind=link}

Thus, operating margin decreased from 11.3% in Q2 2022 to 7.2% in Q2 2023.

SGA (% of revenue) & operating income margin (Company's information)

{kind=link}

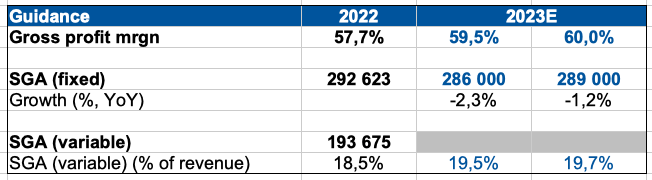

In addition, the company provided guidance for 2023. Thus, management expects that the gross profit margin will be about 59.5% - 60%, and the variable part of expenses for SGA (% of revenue) will increase to 19.5% - 19.7%. You can see the details in the graph below.

{kind=link}

My expectations

I believe that the company's revenue growth rate will continue to be under pressure in the coming quarters due to lower traffic in the chain's stores. On the one hand, as I mentioned earlier, I don't expect we can see a quick traffic recovery even if inflation slows in the second half of 2023 because consumers will continue to face higher costs for interest payments, rent and food. While the company's management said on the Earnings Call following the earnings release that traffic was gradually recovering during Q2, I would like to emphasize that traffic declines continue to be in the double-digit range.

In the second quarter, we saw a pretty big drop in April. We were down 20% in written business, but then we saw some improvement in May. We were down approximately 13% between 12.8% and 13%, and then we're down about 11% in June. So we've certainly seen an improvement from April. I believe Clarence mentioned that in his remarks that April was the most challenging in the quarter, but we've seen kind of more of a leveling back to the low teens in May and June.

In addition, I think that operating margins will continue to be under pressure due to the deleverage effect due to reduced economies of scale, since most of the business' operating expenses (rent, salaries) are fixed. Thus, the company's potential to reduce or optimize costs is limited. If we look at the company's guidance for 2023 in more detail, we will see that management expects a reduction in fixed expenses by 1.2% - 2.3% compared to the previous year, while the decrease in revenue for the first half of 2023 was about 12. 5% YoY. In addition, variable operating expenses, in accordance with the company's guidance, may also increase (% of revenue) from 18.5% to 19.5%-19.7%.

Risks

Margin: reduced economies of scale, increased marketing costs or investments in pricing due to increased competition can lead to a decrease in the operating profitability of the business.

Macro (general risk): high inflation, rising interest rates and declining real incomes may lead to lower consumer spending in the discretionary segment, which may have a negative impact on business revenue growth rates in the future.

Valuation

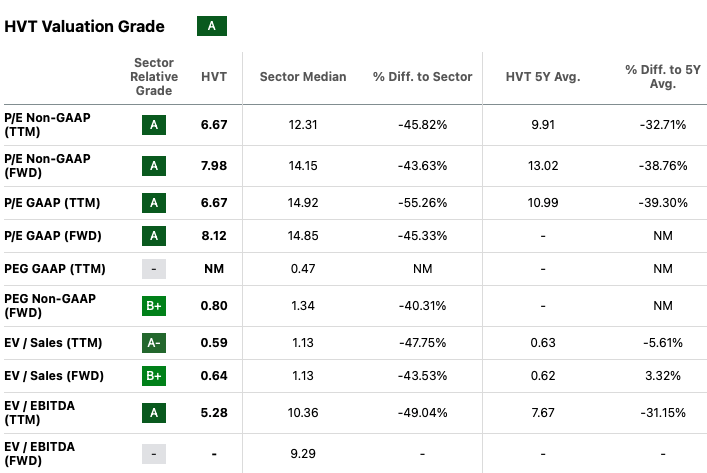

Valuation Grade is A. In accordance with the EV/Sales (fwd) and P/E (fwd) multiples, the company is trading at 0.6x and 8x, respectively, which implies a discount to the sector median of about 43% and 44%, respectively. Despite the fact that the company's shares, in my opinion, are attractively priced, I believe that this is not enough to make a purchase decision due to the lack of clear catalysts/drivers for growth in the coming quarters.

{kind=link}

Conclusion

As such, I expect pressure on both revenue growth and margins to continue in the coming quarters, hence my HOLD recommendation. However, in my opinion, the company's shares are relatively inexpensive based on multiples, so I avoid a sell recommendation. I will happily change my recommendation to buy when I see signals of normalization of traffic and a decrease in macro uncertainty.

For further details see:

Haverty Furniture: Still Not The Best Time To Go Long