HWKN - Hawkins: Modest Upside Potential Despite Positive Growth Outlook

2024-01-02 18:17:49 ET

Summary

- Despite 2Q24 result showing modest decline in revenue due to the sales of its consumer bleach packaging business, margins expanded in the double-digit range. In addition, debt was drastically reduced.

- The expected recovery in chemical volumes is anticipated to drive future revenue growth for HWKN.

- Management's strategic acquisitions are set to further strengthen its water treatment segment, which demonstrated robust growth in the quarter.

- Despite the positive outlook, my target price indicates modest upside potential. Therefore, I am recommending a hold rating as of now.

Synopsis

Hawkins’s ( HWKN ) historical financial results have shown robust revenue growth and strong bottom-line margins. For its 2Q24 results, there was a slight decline in revenue growth due to the sale of its consumer bleach packaging business. However, margins grew at double-digit rates, resulting in an increase in diluted EPS. Looking ahead, its acquisitions aimed at strengthening the water treatment segment, along with the expected recovery in chemical volumes, are anticipated to drive future revenue growth. Despite these positive factors, the current share price lacks a sufficient margin of safety compared to my target price. Therefore, in this post, I am recommending a hold rating for HWKN.

Historical Financial Analysis

Based in Minnesota, HWKN is an established leader in manufacturing and distributing specialty chemicals and ingredients across a broad range of industries. It operates in three business segments: Industrial, Water Treatment, and Health and Nutrition. As of fiscal 2023, the Industrial segment accounts for 50% of the revenue, Water Treatment accounts for 33%, and Health & Nutrition [Stauber] accounts for 17%. The Water Treatment portfolio is experiencing robust growth, which may be attributed to its strategic focus on this segment and recent related acquisitions in October 2023. HWKN's typical end markets include industrial manufacturers, pharmaceutical companies, agricultural operations, food processors, and surface finishers.

Author's Chart

Over the last four years , HWKN's revenue growth has demonstrated recovery and acceleration. In 2020, it was negative 2.90% due to the impact of COVID-19. After the pandemic started to soften, revenue growth began accelerating at double-digit rates. As of 2023, the growth rate was 20.73%, marking a drastic difference from 2020.

{kind=link}

In terms of profitability, HWKN has been robust at the bottom line. Despite a decrease in gross profit margin due to the impact of rising inflation , the company has managed to maintain its operating income and net income margins over the years.

{kind=link}

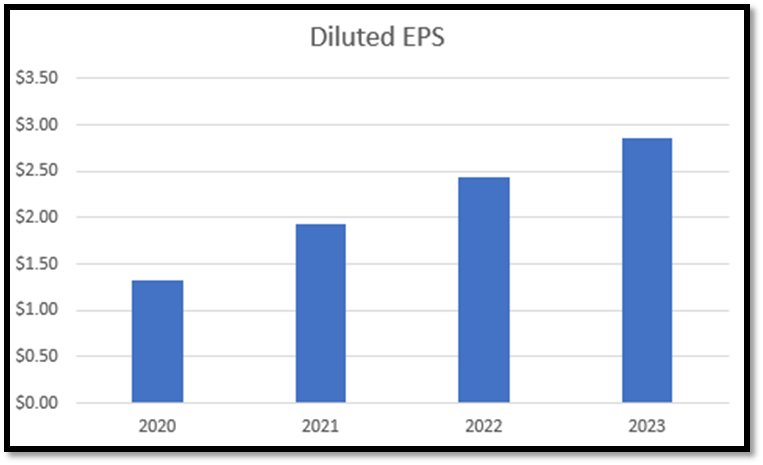

As a result of its growing revenue and robust net income margins, HWKN has managed to grow its diluted EPS annually. In 2020, the diluted EPS was $1.33, and by 2023, it had grown to $2.86. This represents a growth rate of 115%.

{kind=link}

Analysis of 2Q24 Earnings Results

HWKN reported robust 2Q24 earnings results despite a 2% year-over-year decrease in revenue. Management attributed the overall decrease to falling sales in its industrial and health and nutrition segments, which more than offset the strong growth in the water treatment segment. The weakness in the industrial segment was due to the sale of HWKN’s consumer bleach packaging business, resulting in $4 million lower sales. Adjusting for these sales, revenue growth would have been nearly flat. In the water treatment segment, there was strong 17% year-over-year growth driven by solid volumes and pricing.

Despite the slight decrease in revenue, HWKN reported a record quarterly gross profit margin of ~22%, representing a growth of ~16% year-over-year. Additionally, its operating income margin also grew by ~25% year-over-year to ~14% for the quarter. As a result of robust margins amid the revenue decline, which is driven by an extraordinary event, HWKN managed to increase its diluted EPS from $0.86 to $1.10, representing a growth of ~28%.

In terms of the debt-to-equity ratio, there has been a drastic improvement over the years compared to 2021 and 2022, when it was in the 40-45% range. In 2Q24, a portion of HWKN's quarterly operating cash flow was used to reduce debt by $28.6 million . With improved collections on receivables, effective inventory management, and higher net income, the outstanding debt has been significantly reduced to $60 million.

{kind=link}

Strategic Acquisitions to Strengthen its Water Treatment Segment

HWKN’s has been going in line with their business strategy to add more water treatment facilities annually and to expand this segment. On October 2023 , HWKN acquired Water Solution Unlimited Inc. and Miami Products. Water Solutions is the leading supplier of industrial chemicals in the Midwest and provides solutions mainly to municipal clients. They supply bulk chemicals to various sectors, such as water treatment, agriculture, industrial, and hospitals. They have strategic locations in the Midwest, expanding HWKN Water Treatment locations.

Miami Products , or SANYGEN, is similar but focuses more on treatment in swimming pools. These two acquisitions add six more locations for their water treatment operations, expanding HWKN’s water treatment portfolio. These acquisitions will continue to expand HWKN’s geographic territory, product offerings, and solidify its position in the market.

Recovery in The US Chemical Volumes

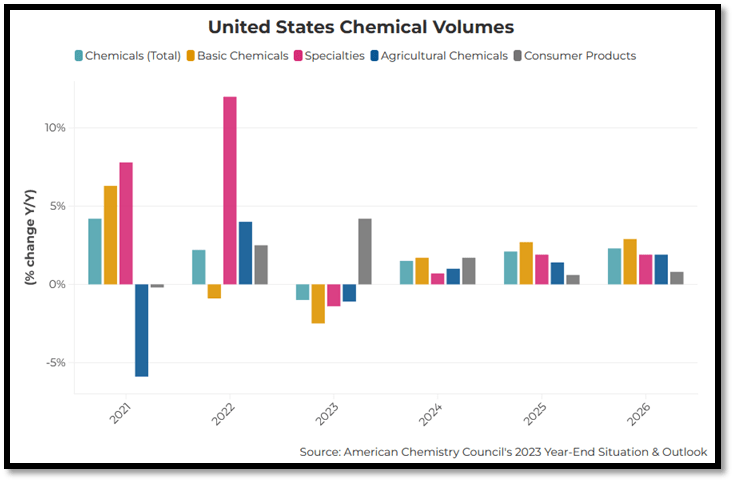

The chemical industry expects a moderate rebound in production from 2023 onwards. There was excessive ordering of chemicals in 2021 and 2022. This led to abnormally high levels of inventory. This has led to a destocking phase, which is likely to be resolved by the end of 2023. In 2024, it is estimated to rebound its volume production in all chemical segments.

According to the American Chemistry Council’s Economic Sentiment Index , chemical production companies experienced falling demand in 3Q23. However, they were expecting a rebound in the next six months. Since these production firms sit close in the early stages of the supply chain, we can anticipate a rebound in this sector prior to growth in the broader economy.

{kind=link}

Strong Growth in Chemical Distribution Market

{kind=link}

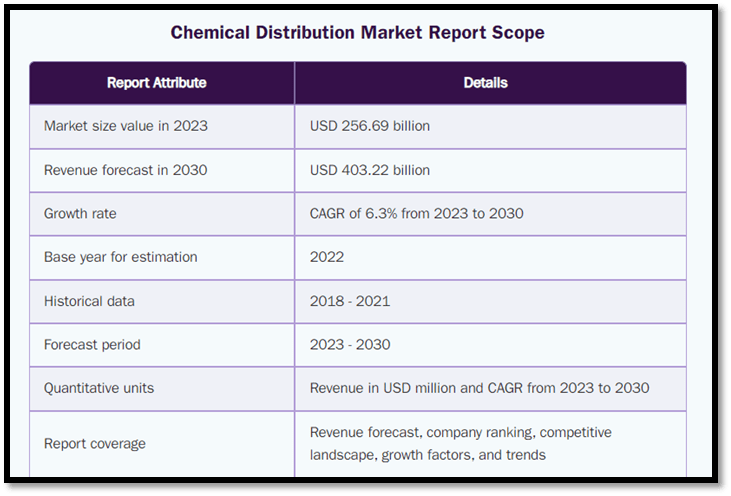

Based on the above report , the global chemical distribution market size is valued at ~$257 billion in 2023. Moving ahead, this market is expected to grow annually at ~6.3%, reaching ~$402 billion by 2030.

The chemical distribution industry is expected to grow with rising consumption by various end users, where the industrial sector accounts for 85% of basic and specialty chemicals. This growth is also attributed to the increased outsourcing of services such as storage, inventory management, chemical blending, and waste treatment, which involve the distribution of chemicals.

In addition, one of HWKN's biggest differentiators in the industry would be its value-added services. Services include inventory management, custom manufacturing, and packaging. This projected growth trend in the chemical distribution market aligns with HWKN’s capabilities in production and distribution, further bolstering HWKN’s position in the industry.

Comparable Valuation Model

For the following comparable valuation model, I will analyze HWKN against its competitors in terms of revenue growth outlook and profitability margins. In terms of market size, HWKN's market capitalization is only 0.46x that of the median. HWKN’s market capitalization is ~$1.4 billion vs. the median of ~$3.2 billion. Despite being about half their size, HWKN’s forward revenue growth is in line with the competitors' median of 4.43%.

Despite its smaller size, HWKN has outperformed its competitors in terms of net income margin TTM. HWKN's net income margin TTM is 7.38%, slightly better than the median of 6.45%. Impressively, HWKN achieves this with a lower gross profit margin TTM. Its gross profit margin is 19.02% vs. the median of 35.05%, which is nearly double that of HWKN.

Even though HWKN has forward revenue growth in line with its competitors and generates higher net income margins with a lower gross profit margin, its current forward EV/Sales ratio of 1.64x is trading lower than the median of 2.3x. Given its smaller size, it seems fair for HWKN to trade at this lower multiple, as smaller companies typically have a higher growth outlook due to the base effect. However, HWKN's growth is in line with the competitors' median.

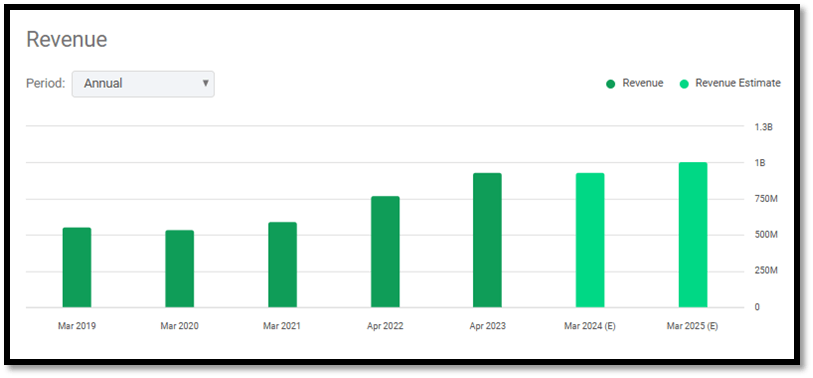

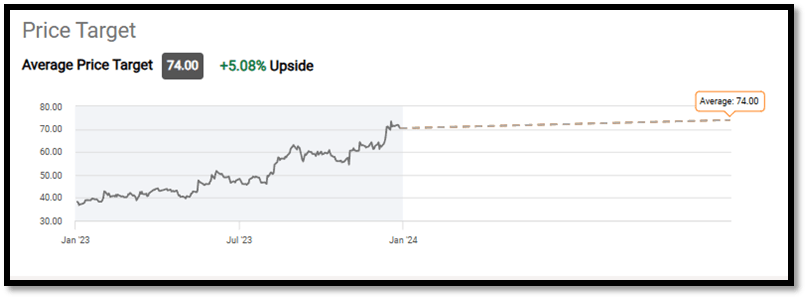

The market revenue estimate for HWKN is expected to reach $933.37 million in 2024 and $1.01 billion in 2025. Based on my analysis and discussion of its strengths and growth catalysts, I believe these estimates are reliable. By applying its current EV/Sales ratio to its 2025 revenue estimates, my 2025 target price is $76.32, representing a modest upside potential of ~8%. Additionally, my target price aligns with Wall Street’s estimate of $74, helping ensure that my valuation is conservative and free from under or overvaluation biases in my opinion.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Upside Risk

As discussed above, if HWKN's strategic acquisitions and the anticipated recovery in the chemical volumes and distribution market lead to higher revenue in the upcoming quarters and surpass market estimates, this could drive its share price higher, especially considering its outperformance in net income margins compared to competitors.

Additionally, its 2Q24 earnings results demonstrated robust margin growth. If the margins continue to grow in the upcoming quarters and are combined with the potential revenue beat, this could also drive the share price higher.

Conclusion

In conclusion, HWKN’s past four years have demonstrated strong revenue growth and a recovery from the impact of COVID-19. Despite falling gross profit margins, its operating and net income margins have remained robust, resulting in an annual expansion of diluted EPS.

For 2Q24, although revenue declined year-over-year, this was partially due to the sale of its consumer bleach packaging business. Adjusting for this sale, the growth is flat. Despite the flat growth, its margins grew at double-digit rates, which led to growth in diluted EPS.

Looking ahead, its strategic acquisitions are expected to further strengthen its water treatment segment, which reported strong growth in 2Q24. Additionally, the anticipated recovery in chemical volumes is expected to drive its future revenue growth higher.

Although HWKN's financial performance is in line with its competitors, its smaller size should generate a higher forward revenue growth outlook due to the base effect. Therefore, I argue that its lower EV/Sales ratio compared to its competitors is justified and reasonable.

With only single-digit upside potential, my target share price lacks a sufficient margin of safety. Furthermore, this target price aligns with Wall Street’s estimates, further solidifying its conservativeness. Therefore, I am recommending a hold rating for HWKN, despite its positive growth outlook.

For further details see:

Hawkins: Modest Upside Potential Despite Positive Growth Outlook