HBT - HBT Financial: A Well-Positioned Bank That Comes At A Cheap Price

2023-04-29 03:49:05 ET

Summary

- HBT Financial, Inc. started the year strong with its steady revenue growth.

- Its solid financial positioning and capitalization on expansion remain its cornerstones.

- Near-term prospects are quite bleak but improvements may gradually materialize.

- It is an ideal dividend stock with its consistent payouts and attractive yields.

- The stock price has been in a downtrend since last month, making it cheap.

In 2022, banks faced mixed market conditions as macroeconomic volatility intensified. Risks increased as inflation and interest rate hikes persisted. Today, The Fed anticipates a mild recession that may weaken consumption, borrowings, and investments. Despite this, HBT Financial, Inc. (HBT) shows it can get through these headwinds. It sustained its revenue growth while expanding its operating size. Although margins contracted last quarter, the company stayed viable. Even better, its operations are founded on its excellent financial positioning. It has stable liquidity levels to sustain its expansion, borrowings, and capital returns.

Moreover, it has adequate capacity to sustain its dividends. Payouts are consistent and well-covered, matched with enticing yields. Meanwhile, the stock price has been in a noticeable downtrend for more than a month already. Yet, it opens more opportunities to purchase shares at a lower price. There is decent upside potential as the stock price remains lower than the intrinsic value of the company.

Company Performance

Banks have a higher risk exposure these days. They operate in a highly volatile macroeconomic landscape today. And HBT Financial, Inc. is no exemption. Yet, it continues to show it can sustain and stabilize its operations amidst disruptions. In fact, it started the year with a larger operating capacity and well-balanced growth and margins. Note that I did not reflect the adjustments in 1Q and 4Q 2022 for consistency. It will be easier to analyze since the acquisition was completed last quarter.

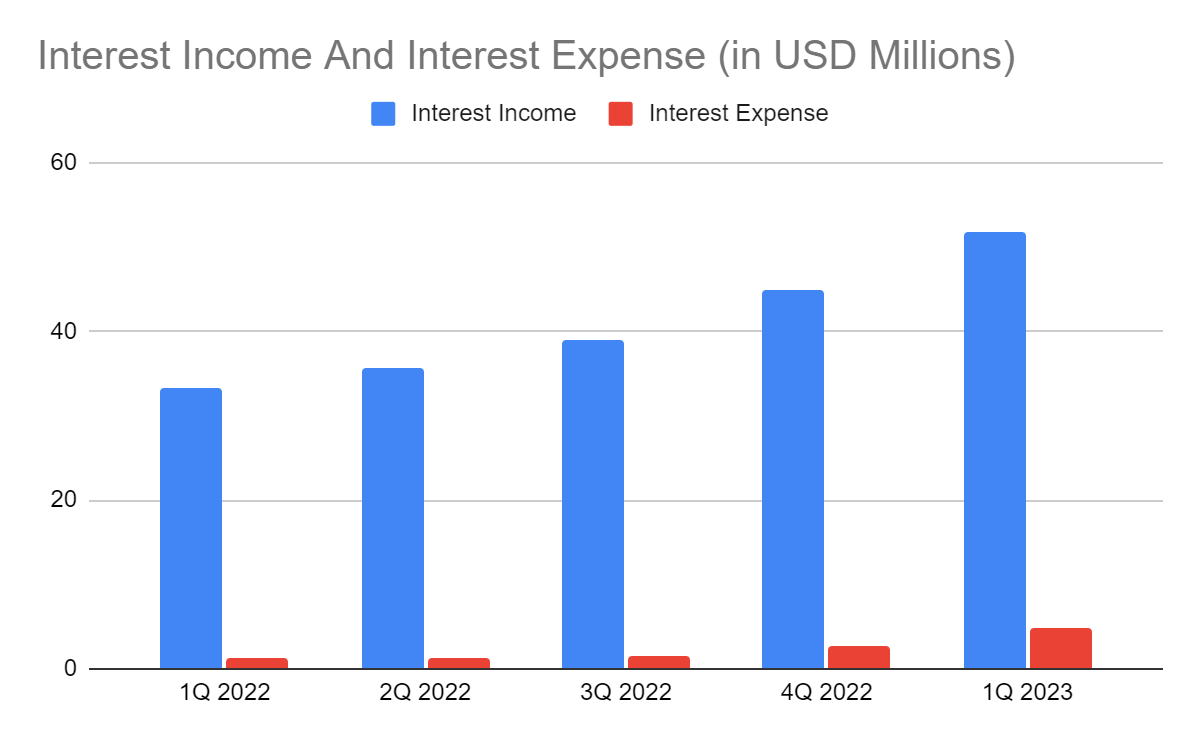

As a holding company for Heartland Bank and Trust Company, its primary revenue streams are loans and securities. Its operating revenue reached $51.78 million , a 55% year-over-year increase. Various factors contributed to this massive growth. First, HBT has capitalized on continued expansion over the years. Its increased operating capacity allowed it to cater to more clients and borrowers. It also helped increase its domestic market presence to attract more demand. Second, it maintained strategic loan repricing amidst interest rate hikes. This move allowed it to keep its loan volume at a manageable level while ensuring reasonable yields. We can see the continued organic loan growth, leading to higher interest and other loan fees. In 1Q 2023, it reached $43.11, or 83% of the total interest income. It increased by 55%, which was crucial for its steady revenue growth. Third, it kept its asset quality solid, with non-performing loans-to-total loans staying low at 0.20%. Although it was higher than in comparative quarters, it was still reasonable due to the acquisition of Town And Country. So as the company grew, it remained cautious to keep default and delinquency risk levels tolerable. To have an extra layer of protection, it increased its allowance for credit losses from 0.97% to 1.21%. Fourth, it capitalized on prudent loan portfolio diversification. It had various loan segments, which could be risky to manage. Yet, the actual composition of each loan showed where the company had the highest concentration. Its commercial loans were 59% of the total loans, while the remaining 41% went to residential and agricultural segments. More specifically, its CRE loans comprised 82% of the total commercial loans. The remaining 18% are C&I loans. It may have to be more careful this year, given the expected changes in the real estate market. We will discuss it further in the following section.

Interest Income And Interest Expense (MarketWatch)

{kind=link}

The fifth growth driver was its investment securities and bank deposits. Although they were only 17% of the total revenue, the 46% year-over-year increase was substantial. Higher interest rates played a vital role in bank deposit yield growth. For investment securities, the story was quite different due to the inverse relationship between interest rates and debt securities. But since 42% of the securities were treasury and municipal bonds, yields remained manageable. We can attribute it to the fact that government-backed securities have better hedges against inflation and lower valuation.

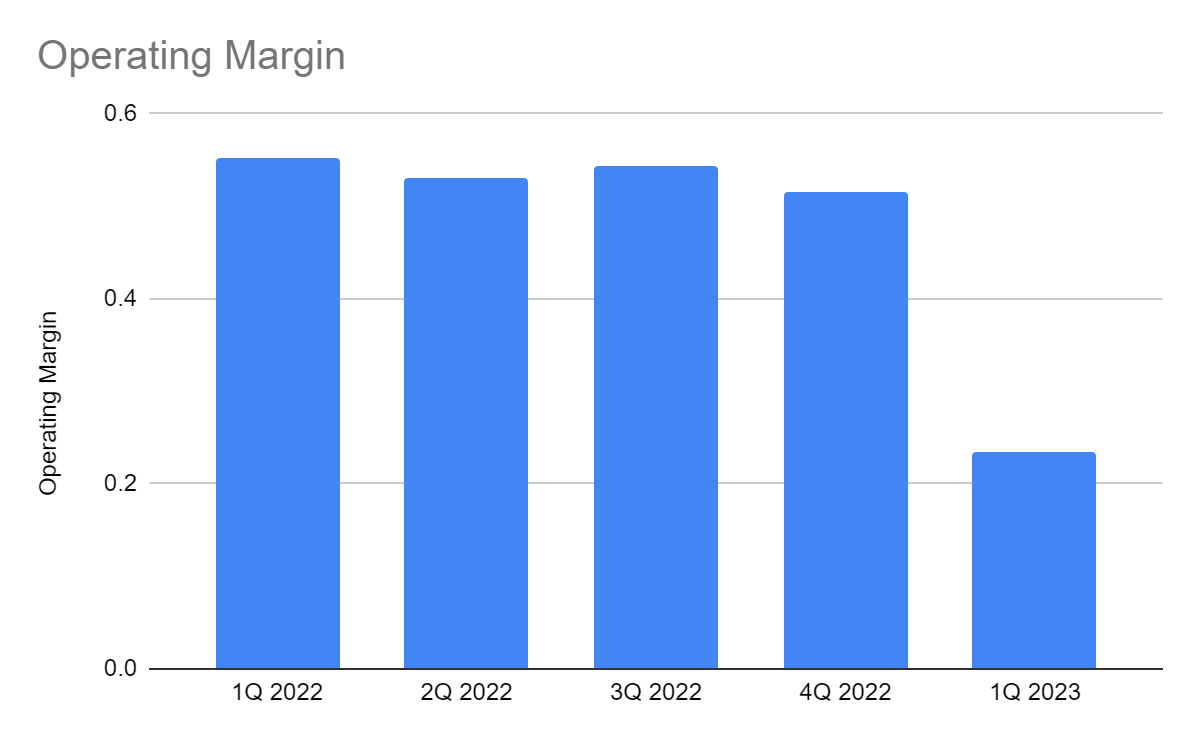

Likewise, inflation and interest rates affected interest and non-interest expenses. Deposits and borrowings became more expensive. Despite this, the sequential change from 4Q 2022 to 1Q 2022 remained stable. Also, the increased interest expenses were consistent with company expectations. Thankfully, its overall cost of funds rose by only 19 bps versus the national rate of 25 bps for the quarter. We can also attribute the massive increase to the acquisition, which reached $13.06 million. The operating margin dropped to 24% versus 55%. We can also see that the unfavorable impact of inflation offset revenue growth, given the decreasing margin. Despite this, the fact the company remained profitable amidst inflation and acquisition completion was impressive. If we exclude the impact of acquisition-related expenses, margins will more than double.

Operating Margin (MarketWatch)

{kind=link}

This year, the company may have a complete grasp of its larger operating capacity. Its acquisition will allow it to cover more clients and borrowers. However, it comes at a higher risk as interest rates continue to increase. But improvements start to become evident, which can help it stabilize its operations. As such, we will discuss it further in the following section.

Why HBT Financial, Inc. May Stay Solid This Year

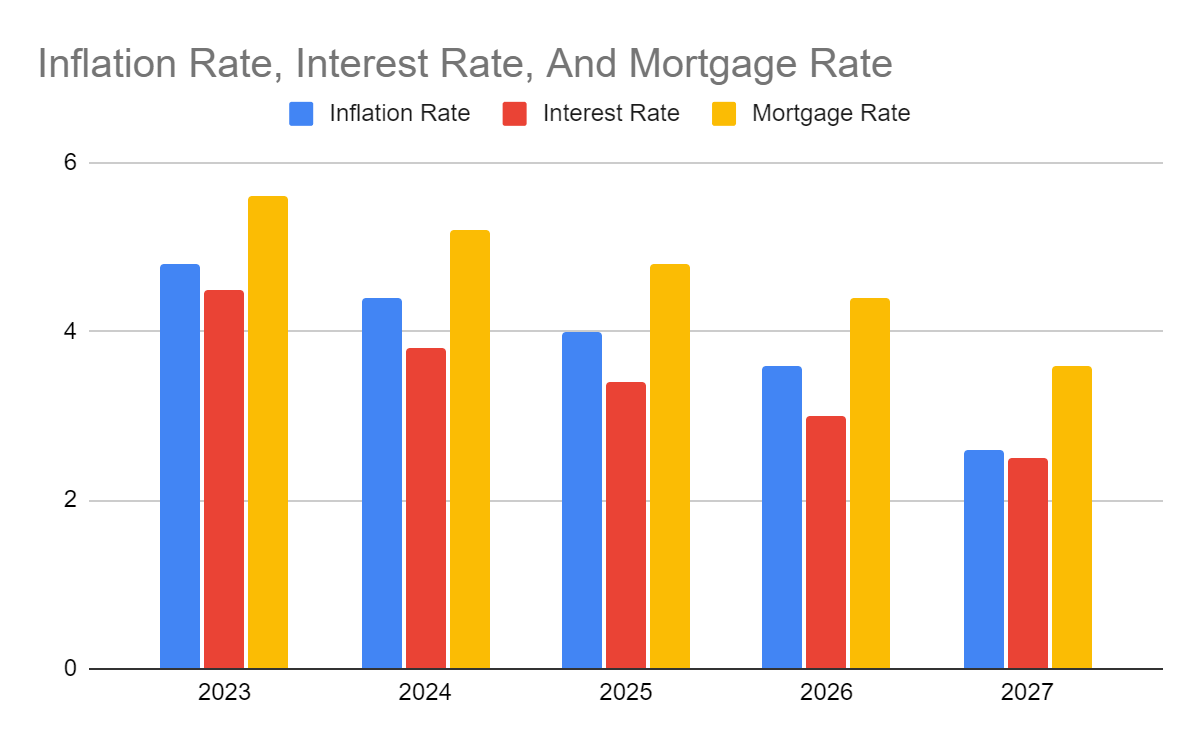

Inflation has become a double-edged sword for many banks. It led to higher interest rates that attracted more clients and raised loan yields. Yet, the impact was quite more on the unfavorable side as margins contracted. The good thing was that the company sustained its revenue growth to stay viable. However, it may not heave a sigh of relief this quarter as macroeconomic risks remain evident. As The Fed continues to stabilize inflation, it may have to increase its interest rates further. It may have to stay conservative to keep inflation lower than in 2022. So as interest rates increase, it may affect investment yields, discourage borrowers, and increase delinquency risks. Deposits and borrowings may have higher interests. It may increase the probability of a recession.

On a lighter note, the decrease in inflation was faster and further than expected. It is now 5%, which is 45% lower than the 9.1% peak in 2022. It is also 17% lower than the previous month. With that, the potential recession may be milder and shorter than expected. Interest rates may keep increasing in line with the tight monetary policy of The Fed. But increments may start to cool down in the second half. During the last meeting, interest rates only increased by 25 bps compared to the 75 bps increment in four consecutive quarters. It may still lead to higher interest expenses in HBT. But the company may manage loans, deposits, investments, and borrowings better. It may be easier for the company to reprice and diversify them to maximize their potential. Also, lower inflation means lower non-interest expenses, which can partially offset the increase in interest expense.

Inflation Rate, Interest Rate, And Mortgage Rate (Author Estimation)

{kind=link}

Concerning its CRE loans, HBT must still watch out for the current changes in the property market. Since mid-2022, property sales have cooled down. It must be more careful with its residential mortgages. Despite this, I don't think that the current pattern will lead to a massive market crash. Property shortage is one of the reasons home prices may remain stable. At the start of the year, the US housing market was short of 6.5 million units. But a more recent report of the Wall Street Journal revealed a 12% increase in shortages in only a quarter. The US housing market is short of 7.3 million houses. It shows that demand continues to outweigh supply, and more individuals become interested in buying homes. Wages are now higher, while unemployment stays low, increasing purchasing and borrowing power. The decreasing inflation and stable labor market conditions became a catalyst for the rebound. It should be unsurprising since the primary price increase driver was demand, not any cost-push factors like materials and labor. It started in 2020 when the US started to recover from the recession by setting interest rates to near zero. Lower borrowings and mortgages and employment and wage rebound drove property demand influx and price increases. Moreover, property builders remain careful in fear of another Great Recession. This behavior helps avoid overselling and speculative mania that can lead to massive price changes and valuation losses.

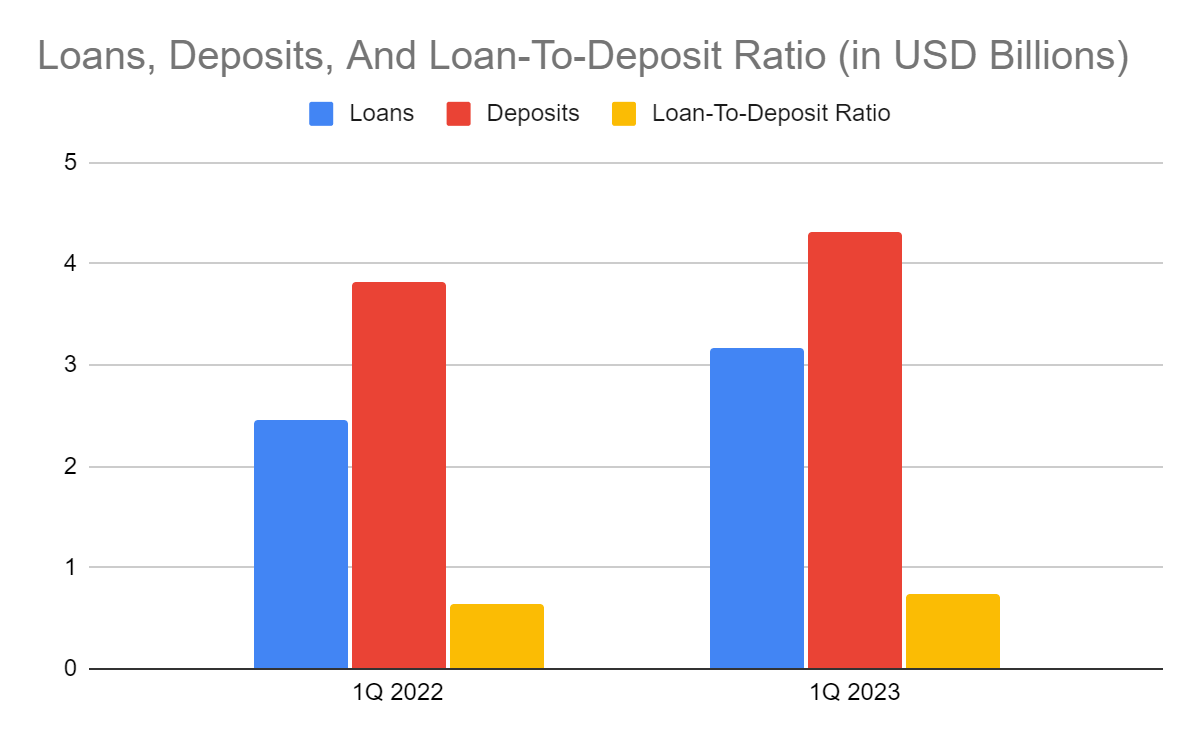

But what makes HBT secure is its solid financial positioning amidst expansion. It also maintains solid asset quality and prudent portfolio diversification. With its excellent loan quality and active repricing, it continues to stabilize loan volume and yields. And after completing its M&A with Town And Country, loans and deposits increased substantially. It now has a higher operating capacity and market presence. The best part of it is that despite the organic loan growth, the company stays careful to maintain liquidity levels. Its loan-to-deposit ratio of 73% remains lower than the standard 80-90% ratio. Unlike many banks with ratios of 90-95%, the company makes sure it has more than enough reserves. Doing so will help it cover potential defaults and delinquencies.

Loans, Deposits, And Loan-To-Deposit Ratio (HBT 4Q Financial Release)

{kind=link}

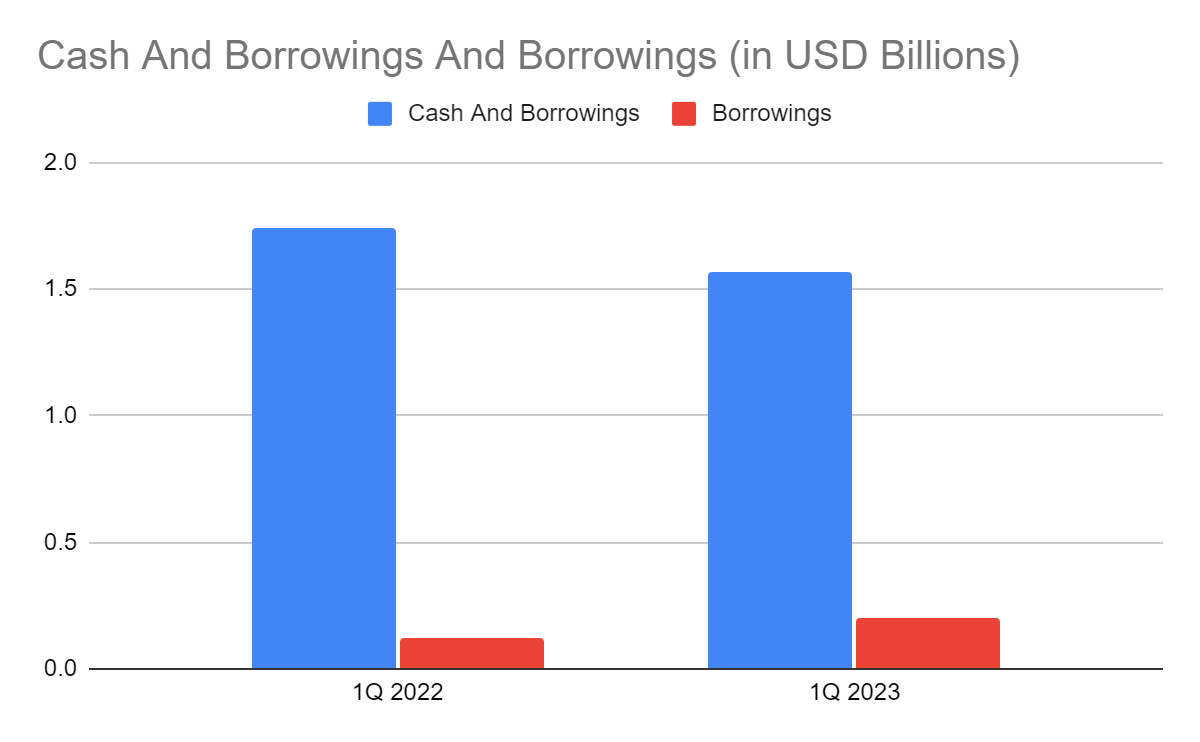

Also, its cash reserves increased, which we can attribute to maintained viability. Despite lower income, the company continues to generate returns. This aspect allowed it to complete its acquisition without burning so much cash or relying solely on its financial leverage. We can see it in the manageable increase in borrowings. The combined value of cash and investments comprises 31% of the total assets, making HBT very liquid. More importantly, its Net Debt/EBITDA Ratio of less than 1x confirms the adequate capacity of the company to sustain its operations while covering borrowings. It continues to balance its viability with liquidity and sustainability.

Cash And Investments And Borrowings (HBT 4Q Financial Release)

{kind=link}

Stock Price Assessment

The stock price of HBT Financial, Inc. has been in a downtrend for over a month already. It remains low, which we can attribute to lower income and bleak near-term market prospects. At $17.81, the stock price is 4% higher than last year's value but 22% lower than the March peak. Yet, the downward trend opens more opportunities to buy shares at a discount. It may be attractive using the PE Ratio of 8.95x and EPS estimates by NASDAQ , giving a target price of $21.38. The PB Ratio agrees, given the current BVPS and PB Ratio of 14.02 and 1.22x. If we use the average PB Ratio of 1.36x, the target price will be $19.24.

Moreover, HBT is an attractive dividend stock, given its consistent payouts. It has yields of 3.74%, way higher than the S&P 600 and NASDAQ average of 1.41% and 1.57%. Payments are also well-covered, given the Dividend Payout Ratio of 56%. Even better, cash reserves are high, which are about seven times dividends if set at $0.17 per share. The company also sustains its capital returns through share repurchases. Using either cash or net only, it can cover dividends and stock repurchases for the quarter. To assess the stock price better, we will use the DCF Model.

FCFF $41,430,000

Cash $35,244,000

Borrowings $202,250,000

Perpetual Growth Rate 4.4%

WACC 9.2%

Common Shares Outstanding 32,095,370

Stock Price $17.81

Derived Value $24.01

The stock price adheres to the potential undervaluation of the stock price. There may be a 34% upside in the next 12-18 months. So, investors may see it as an opportunity to buy shares at a discount.

Bottomline

HBT Financial, Inc. remained a solid company after sustaining its revenue growth while remaining viable amidst inflation. It has an excellent financial positioning that can sustain its larger operating capacity and capital returns. It is also an ideal dividend stock, given the consistent payouts and high yields. Even better, the stock price remains cheap relative to the intrinsic value of the company. The recommendation is that HBT Financial, Inc. is a strong buy.

For further details see:

HBT Financial: A Well-Positioned Bank That Comes At A Cheap Price