HCA - HCA Healthcare: Q1 Earnings Steady As She Goes

2023-04-23 02:18:07 ET

Summary

- HCA Healthcare has rallied nearly 70% since July last year.

- The company has massive market opportunities and strong competitive advantages that should continue to drive growth.

- The recent earnings were solid with double-digit EPS growth and guidance being raised.

- The current valuation remains attractive.

- I rate the company as a buy.

Investment Thesis

HCA Healthcare ( HCA ) has been an excellent compounder in the past decade with shares up over 640%, significantly outpacing the S&P 500 Index (SPY) which increased by 160%. The share price reached its historical high last week amid upbeat earnings and I think there is still ample room to run.

The company has a dominant position in the healthcare facilities market, which is massive and ever-expanding. The recent earnings continue to be impressive with solid growth across almost all metrics. Despite the huge rally in the past few months, its current valuation remains pretty attractive with multiples below most healthcare peers. Considering its strong market position and steady growth, I believe there should be more upside potential therefore I rate the company as a buy.

Why HCA Healthcare?

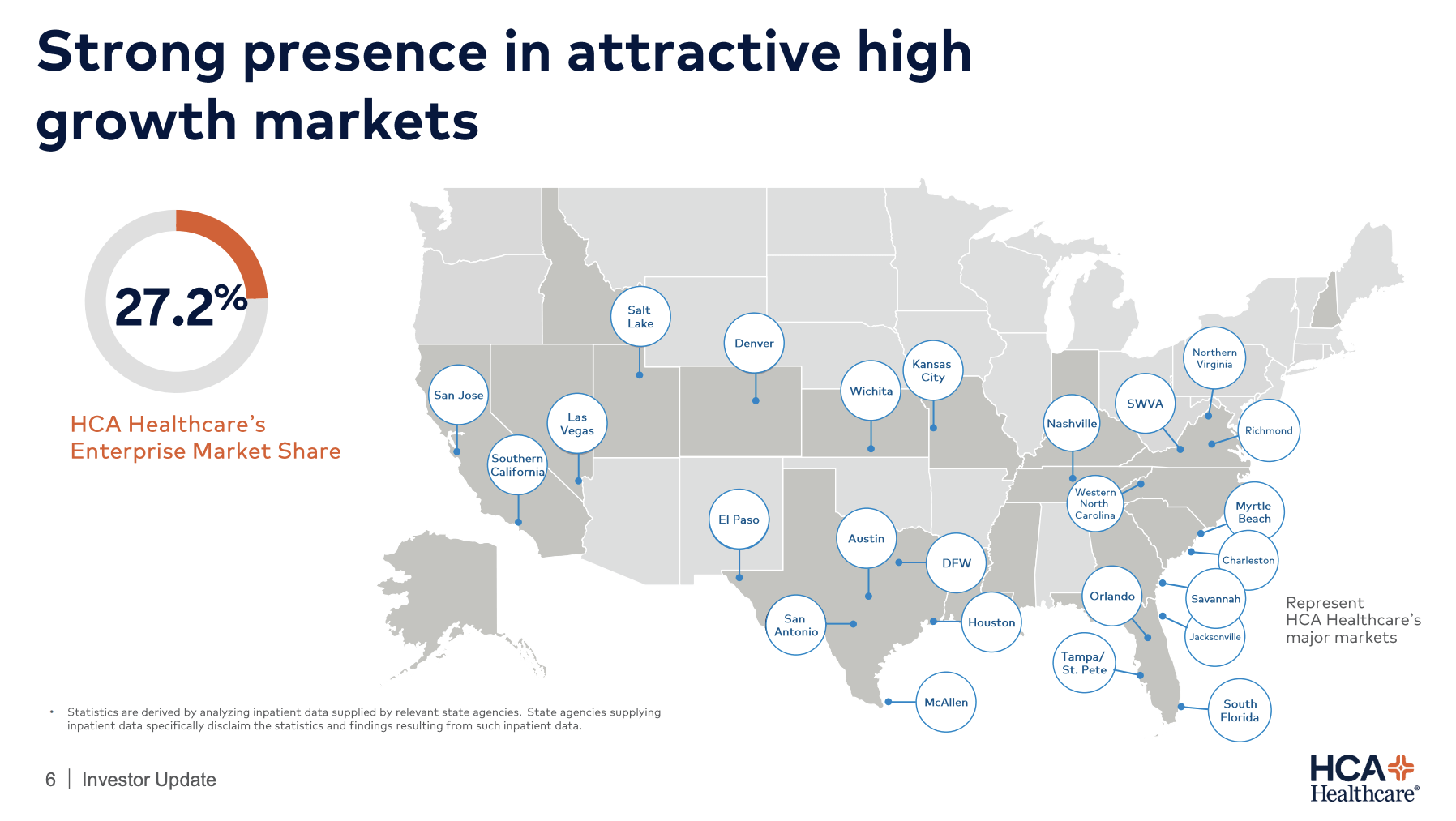

HCA Healthcare is one of the largest healthcare providers in the US that operates over 180 hospitals and 2,000 ambulatory points of care. The sites combined have 45,000 medical staff serving approximately 37 million patients annually. The company currently has a dominant position in the enterprise healthcare facilities market with a significant market share of 27.2%.

The TAM (total addressable market) of the company is massive. According to Grand View Research , the market size of US hospital facilities is forecasted to grow from $1.4 trillion in 2022 to $2.5 billion in 2030, representing a solid CAGR (compounded annual growth rate) of 7.6%. The market continues to expand due to the ageing population and the rising occurrence of chronic diseases, which increases the demand for more and better healthcare facilities. I believe the demand will only continue to rise as the overall life expectancy increases over time thanks to improved technologies. Other than its size, the market is also extremely attractive due to its highly resilient and stable nature, as healthcare remains one of if not the most non-discretionary sectors.

The company also has a strong competitive advantage due to its size. For instance, its huge workforce allows them to provide more comprehensive services compared to competitors. The larger scale also allows them to deploy much more advanced technology such as automation and better clinical system, which further enhances operating efficiency and patients' experience. Considering the ongoing market expansion, dominant position, and strong competitive advantage, I believe the company is well-positioned to generate decent and durable long-term growth rates.

{kind=link}

HCA Healthcare

Upbeat Q1 Earnings

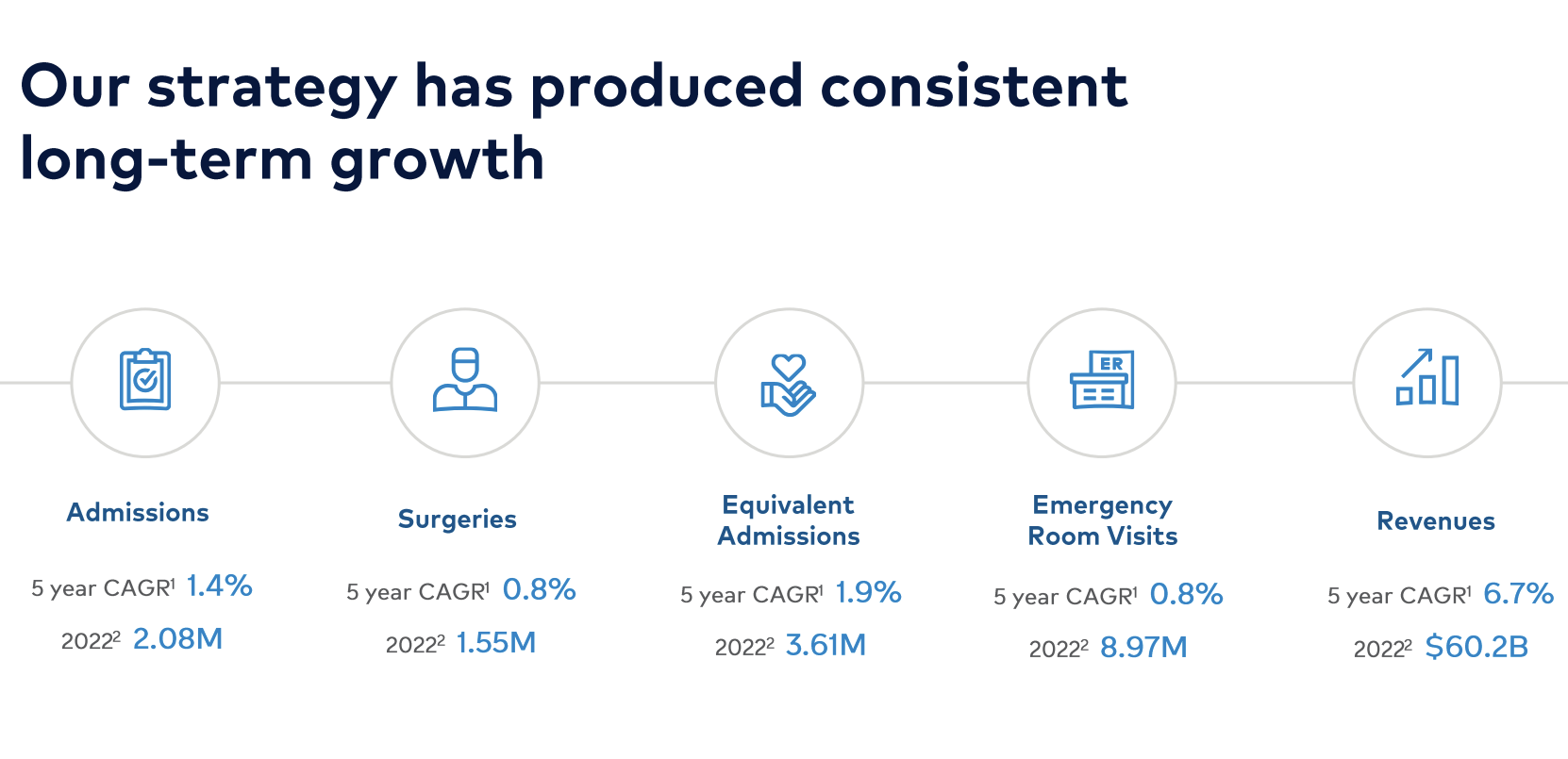

HCA Healthcare announced its first-quarter earnings last week and the results are solid considering the current macro backdrop, especially the bottom line. The company reported revenue of $15.6 billion, up 4.7% YoY (year over year) compared to $14.9 billion. The growth is mainly driven by higher volume.

Same-facility admissions increased 4.4% from 503,101 to 525,235, while equivalent admissions increased 7.5% from 851,247 to 915,485. Non-COVID-related admissions grew by 12%, accounting for 97% of the total volume. The increase in volume was partially offset by the decline in revenue per equivalent admission, which dipped 2.2% from $17,392 to $17,011 due to product mix.

Demand was upbeat across different categories. Same-facility inpatient surgery cases grew 3.6% from 125,894 to 130,460, while outpatient surgery cases grew 5.1% from 241,905 to 254,196. Emergency room visits were also up 10.3% from 2.04 million to 2.25 million.

Sam Hazen, CEO, on Q1 Results

The operational momentum we had at the end of the last year continued into the first quarter of 2023. The company produced solid earnings that reflected strong demand for our services and improvements in our operating costs in particular contract labor expenses.

The bottom line was strong as the increase in spending moderated, particularly in the labor area. Salaries and benefits as a percentage of revenue dropped 100 basis points from 46.4% to 45.4%. Total operating expenses as a percentage of revenue dipped 20 basis points to 87.7%.

The better cost control resulted in the adjusted EBITDA increasing 7.8% YoY from $2.94 billion to $3.17 billion. The adjusted EBITDA margin expanded 60 basis points from 19.7% to 20.3%. The diluted EPS was $4.85 compared to $4.14, up 17.1% YoY. This is largely attributed to the reduction in the share count thanks to ongoing buybacks.

In spite of the solid momentum, the company also raised its guidance for FY23. It now expects revenue to be $63 billion at the midpoint compared to the $62 billion announced previously. The diluted EPS is now forecasted to be $17.9 at the midpoint, up from the $17 announced previously.

{kind=link}

HCA Healthcare

Valuation

Despite the nearly 70% rally since July last year, HCA Healthcare's valuation still looks pretty compelling. The company is currently trading at a PE ratio of 14.1x, which is lower than most large-cap healthcare providers including UnitedHealth Group ( UNH ), Elevance Health ( ELV ), and Humana ( HUM ). As shown in the first chart below, its multiple represents a discount of 23.4% compared to peers' average PE ratio of 18.4x.

As shown in the second chart below, the company also has best-in-class profitability and margins thanks to its dominant position in the healthcare facilities market. I do not think the discount is justified and the company should be trading at a more in-line valuation compared to peers, which should present meaningful upside potential moving forward.

Investors Takeaway

I believe HCA Healthcare will continue to be an outstanding compounder. The company has a leading position in the attractive healthcare facilities market that is massive and highly resilient thanks to its non-discretionary nature. Despite a weakening economy, the latest earnings remain solid with double double-digit EPS growth and guidance being raised. The current valuation is also cheap compared to other healthcare peers, despite having great fundamentals and better profitability. I believe the company presents a compelling investing opportunity and I rate HCA stock as a buy.

For further details see:

HCA Healthcare: Q1 Earnings, Steady As She Goes