HCA - HCA Healthcare: Rx For Success

2023-10-10 17:20:49 ET

Summary

- HCA Healthcare's consistent growth trajectory, ample liquidity, superior profitability, and attractive valuation make it a favorable investment.

- The company's fundamentals have shown consistent growth, with revenue and NOPAT increasing annually.

- HCA's leading market position, economies of scale, and strong cash flow contribute to its profitability and industry leadership.

We previously made HCA Healthcare, Inc. ( HCA ) a Long Idea in June 2020, as part of our See Through the Dip series of reports.

Our thesis highlights HCA’s consistent growth trajectory, its ample liquidity, superior profitability, and attractive valuation. Today, the company’s earnings continue to beat expectations and management is revising revenue and earnings upwards for 2023. Meanwhile, the valuation of the stock implies only modest profit growth and still holds upside.

HCA Offers Favorable Risk/Reward Based on the Company’s:

- Consistent revenue, net operating profit after tax (NOPAT) and free cash flow growth

- Economies of scale

- Superior profitability versus peers

- Cheap stock

What’s Working

Old Faithful: HCA’s fundamentals have shown consistent growth in the last decade. HCA has grown revenue by 7% compounded annually since 2017 and NOPAT by 8% compounded annually over the same time.

Furthermore, the company has been able to expand NOPAT margins from 11% in 2017 to 12% over the trailing-twelve-months ((TTM)), which helped drive return on invested capital ((ROIC)) from 16% to 18% over the same time.

Figure 1: HCA Healthcare Revenue and NOPAT Since 2012

New Constructs, LLC

Sources: New Constructs, LLC and company filings

Same-Facility Admissions Rising: HCA’s same-facility metrics showed impressive growth in 1Q23, which led the company to lift previous guidance for both revenue and net income for 2023. Same facility equivalent admissions jumped 8% YoY in 1Q23, with emergency room visits rising 10.3% YoY. COVID-related admissions dropped from 10% of same-facility admissions in 1Q22 to 3% in 1Q23. Lower COVID admissions and reimbursements drove revenue per equivalent admission to fall 2% YoY.

Moving forward, the company continues to expect strong demand in same-facility admissions, as non-COVID admissions were up 12% YoY in 1Q23. See Figure 2.

Figure 2: HCA’s YoY Change in Admissions

New Constructs, LLC

Sources: New Constructs, LLC and company filings

Healthy Cash Flow: HCA’s leading market position helps it generate ample cash flow to fund its operations. Over the past five years, HCA generated $23.3 billion (19% of enterprise value) in free cash flow ((FCF)) and has generated positive FCF in each of the past 15 years.

Figure 3: HCA’s Cumulative FCF Since 2017

New Constructs, LLC

Sources: New Constructs, LLC and company filings

Industry Leader: The healthcare industry is highly competitive and vulnerable to changes in regulation, rising labor costs, and fast-moving technological disruption. HCA’s profitability metrics were far superior to peers’ when we wrote our original report and have remained so.

Over the TTM, HCA boasts a 12% NOPAT margin and 18% ROIC. These metrics, especially ROIC, surpass those of publicly traded competitors such as Encompass Health (EHC), Tenet Healthcare (THC), Universal Health Services (UHS), and others, per Figure 4.

Figure 4: HCA’s Profitability Vs. Peers: Trailing Twelve Months ((TTM))

New Constructs, LLC

Sources: New Constructs, LLC and company filings

Qualitatively, HCA’s sheer scale remains a competitive advantage and a flywheel of growth for the company. The company is the largest health network in the U.S. with 180 hospitals, 2,300 ambulatory sites of care, and over 50 years in business. HCA’s size allows it to benefit from economies of scale and to invest heavily in technology, patient satisfaction , and its long-trusted brand – all of which further widen its moat.

The fundamentals reflect HCA’s position as an industry leader: the company’s TTM revenue is higher than that of all of its competitors in Figure 4 combined. HCA’s TTM NOPAT exceeds the total NOPAT of the peer group by 75%. More interestingly, the advantage of scale has allowed HCA to outgrow its competitors on both the top and bottom lines. HCA is much larger and is also growing much faster than its competitors.

From 2018 to the TTM, HCA grew revenue and NOPAT at 6% and 8% compounded annually, respectively. Its peer group, on the other hand, could barely break 2% compound annual growth. See Figure 5.

Figure 5: HCA’s Revenue and NOPAT Growth: 2018 – TTM

New Constructs, LLC

Sources: New Constructs, LLC and company filings

What’s Not Working

Skilled Labor Is Still Scarce: Like other industries dealing with labor shortages and rising wages, HCA has struggled to hire and retain enough skilled workers to staff its hospitals and consistently deliver high-quality care. According to management, 1Q23 was a period of renewed efforts in hiring, with headcount up 2% from 2022 and the utilization of contract labor down 21%. Contract labor currently makes up 7.1% of the company’s salaries, which is still up from 6% pre-COVID. The company’s labor expenses have grown 7% compounded annually since 2018 – faster than revenue – but in line with NOPAT growth.

Though management paints a rosy picture of the company’s treatment of its workers, HCA’s workforce does not seem to agree. In April 2023, workers rallied outside of the company’s headquarters for better staffing and worker treatment. Workers complain about burnout and patient care failures. The issue is not restricted to HCA. According to a survey conducted by AMN Healthcare in January 2023, one-third of nurses plan to quit their jobs, as a result of burnout from the COVID pandemic. However, HCA must address this challenge effectively or risk tarnishing its brand and compressing margins from higher wages.

Shares Have Upside at Current Levels

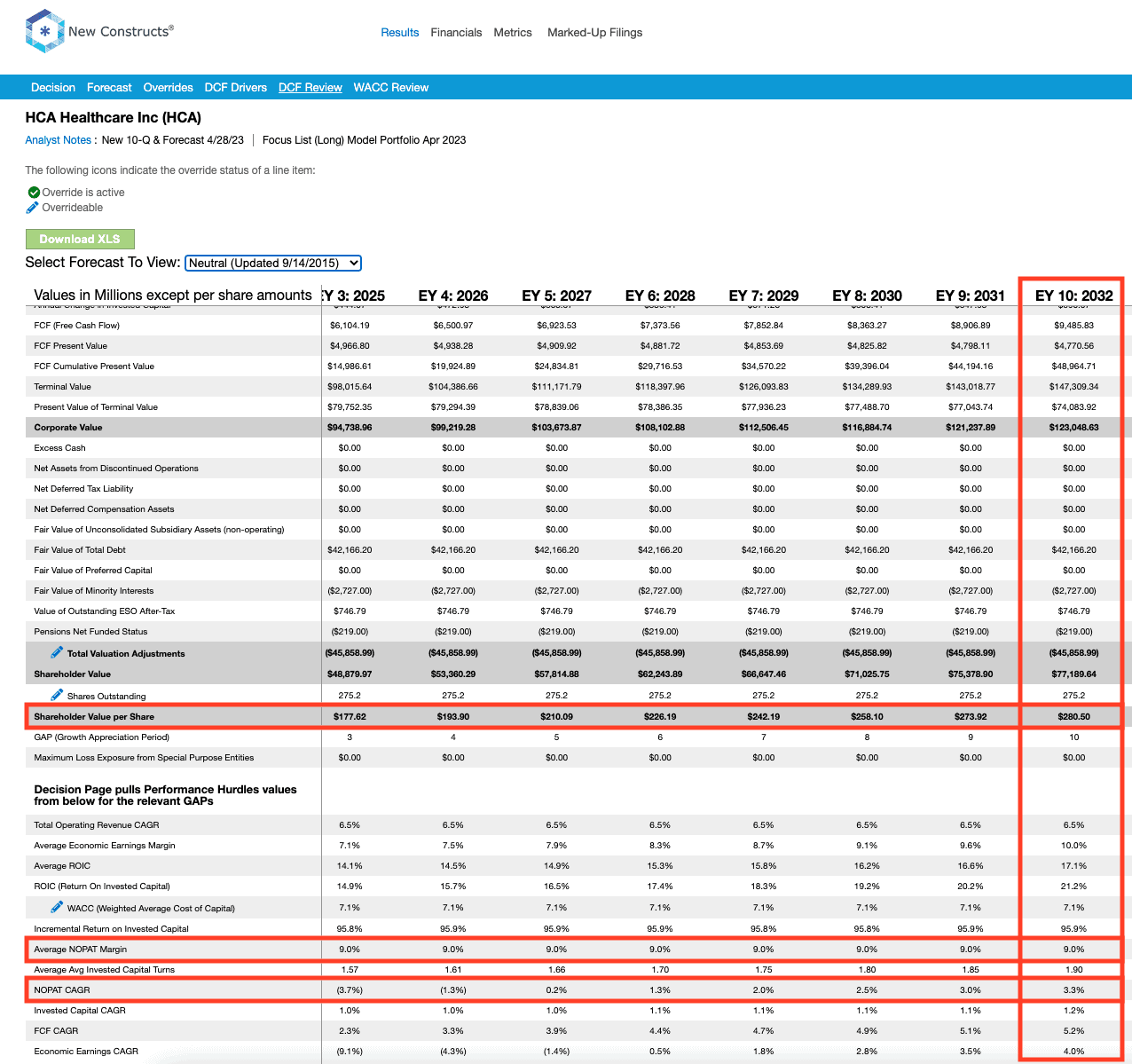

Below, we use our reverse discounted cash flow ((DCF)) model to analyze expectations for different stock price scenarios for HCA. At its current price, HCA’s price-to-economic book value (PEBV) ratio is 1.3, which means the market expects its NOPAT to permanently rise 30% from current levels.

In the first scenario, we quantify the expectations baked into the current price. If we assume:

- NOPAT margin falls to 9% (versus 12% average in the past five years) through 2032, and

- Revenue grows at 6.5% a year through 2032 (compared to 7% compounded annually since 2017), then

The stock is worth $281/share today – nearly equal to the current stock price. In this scenario, HCA’s NOPAT grows 3% compounded annually from 2023–2032. For reference, HCA has grown NOPAT by 8% compounded annually from 2017–2022 and 7% compounded annually over the past decade.

{kind=link}

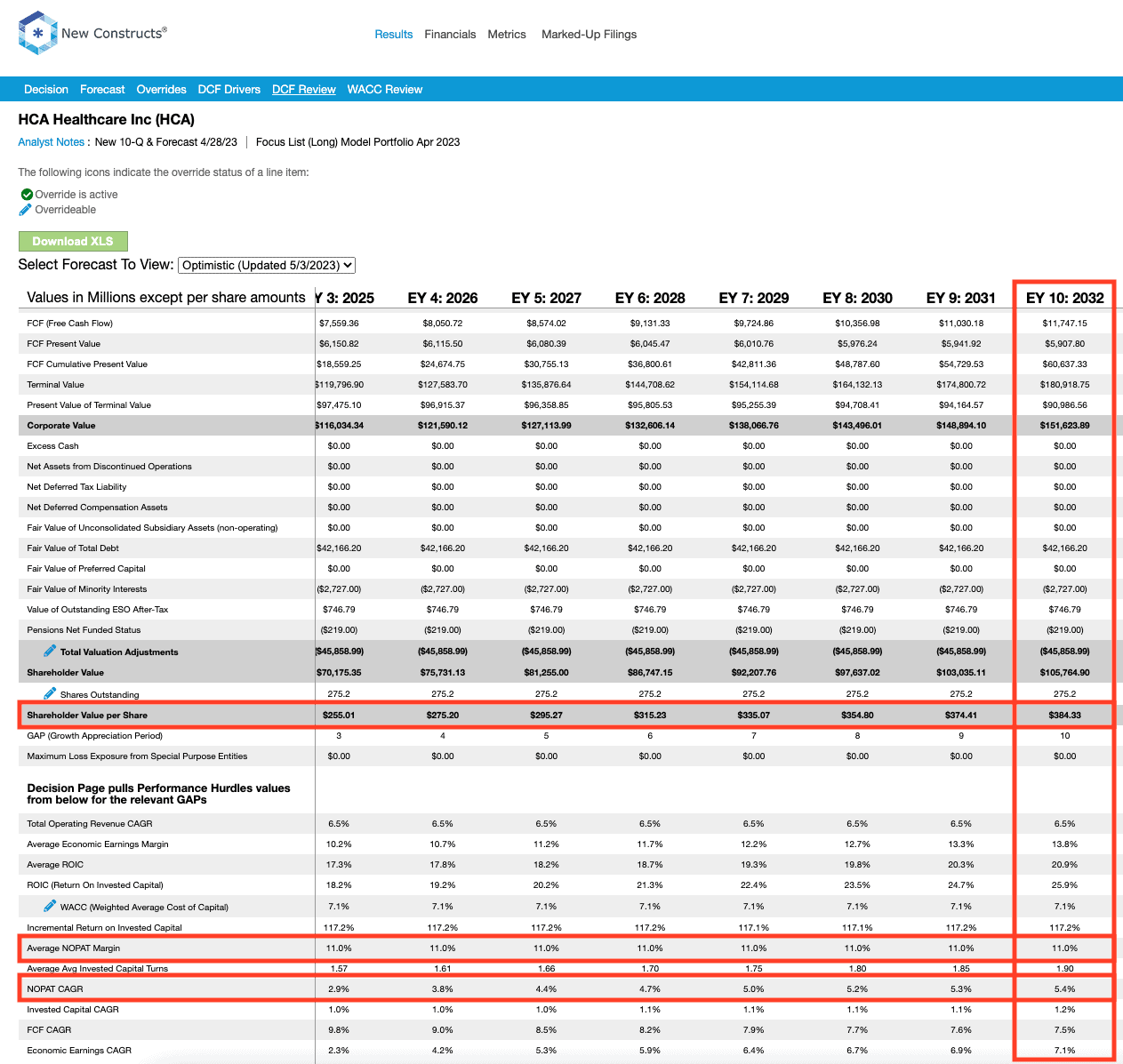

Shares Could Go At Least 35% Higher

If we instead assume:

- NOPAT margins falls to 11% from 2023 – 2032,

- revenue grows by 6.5% compounded annually from 2023 – 2032, then

The stock is worth $384/share today – a 35% upside to the current price. In this scenario, HCA’s NOPAT would grow 5% compounded annually from 2023 to 2032. For reference, HCA has grown NOPAT by 8% compounded annually from 2017–2022 and 7% compounded annually over the past decade. Should the company’s NOPAT grow more in line with historical levels, the stock has even more upside.

{kind=link}

Figure 6: HCA Historical and Implied NOPAT: DCF Valuation Scenarios

New Constructs, LLC

Sources: New Constructs, LLC and company filings

Disclosure: David Trainer, Kyle Guske II, and Italo Mendonça receive no compensation to write about any specific stock, sector, style, or theme.

For further details see:

HCA Healthcare: Rx For Success