HCA - HCA Remains Attractive Despite A JV Misstep

2023-11-20 17:11:08 ET

Summary

- HCA Healthcare's shares have risen 8% from last year but fallen 15% from their summer high.

- The company's earnings have undershot expectations due to slower margin recovery and a joint venture mishap.

- Despite these challenges, recent guidance for 2024 is positive, pointing to potential upside for shares if operating issues are resolved.

Shares of HCA Healthcare ( HCA ) have risen about 8% from last year, but they have fallen about 15% from their summer high. Since recommending investors buy HCA last October , shares have risen by about 20%. That said, the company has undershot my expectations for about $19.25 in earnings as margins have recovered more slowly amid a joint venture mishap. Still, recent guidance for 2024 is positive and does point to more upside for shares, particularly if it can work through some lingering operating issues.

{kind=link}

Seeking Alpha

In the com pany’s third quarter reported on October 26th, it e arned $3.91 in adjusted EPS, missing consensus by $0.05 even as revenue of $16.2 billion beat by $400 million. Earnings were surprisingly down by 0.5% even as revenue rose by 8.3%. Similarly, adjusted EBITDA of $2.88 billion was down 1% from last year. One of the primary reasons for being bullish on HCA last year was the fact that margins should expand. This simply has not materialized as hoped.

Adjusted EBITDA margins were down 160bp to 17.8%. Labor costs rose to 46.6% of revenue from 46.1% while other operating expenses rose by 170bps at $3.4 billion. This rise in labor costs is surprising given management on the call said that the use of contract labor (which is more expensive) has fallen as turnover has stabilized and nurse hiring conditions have improved meaningfully.

Now it may be that while wage growth has slowed, headcount has risen from understaffed levels so that the ratio of procedures to employees is coming down, increasing labor’s share of revenue. That loss of operating leverage would not seem consistent with the fact that same facility admissions were up 3.4% and pricing per admission was up 3.6%. These strong growth rates should more than offset the fact more lucrative inpatient procedures were up a more modest 1.6%.

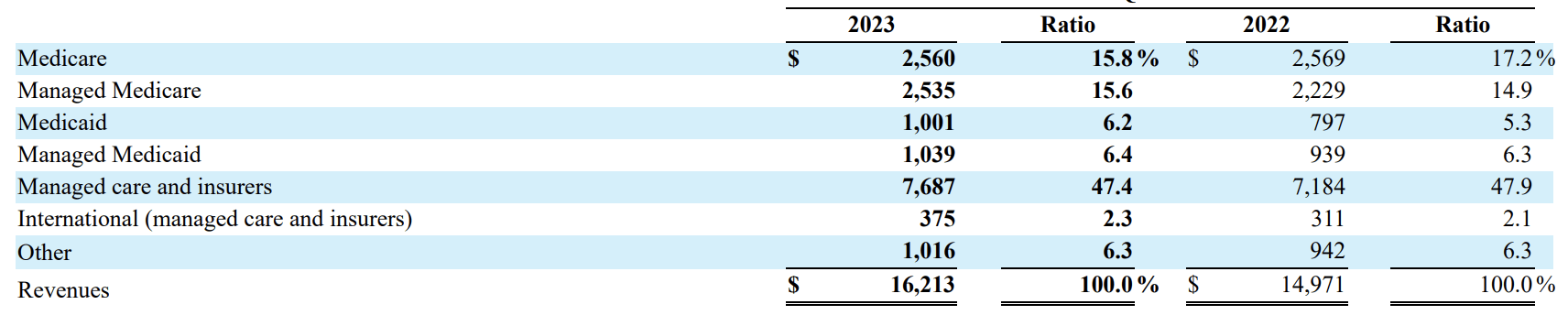

I do think one negative impacting HCA’s margins has been unfavorable payer mix. Hospital pricing is a bit of a black box for patients, and there are complex negotiations with the different payers for procedures. But in general, private insurance pays the most, followed by Medicare, and then Medicaid pays the least. Well, last quarter, private insurance accounted for 50bp less of revenue than last year while total Medicaid increased by 100bp. This unfavorable mix shift is surprising given pandemic support programs that boosted Medicaid enrollment have expired while a strong jobs market should limit Medicaid growth. These factors should be reducing Medicaid’s share. I am inclined to look through this headwind, which could have reduced EBITDA margins by 40-60bp, as likely an anomaly rather than a new trend. It does bear ongoing monitoring by investors, though.

{kind=link}

HCA Healthcare

This however does not explain the entire shortfall. The other problem has been Valesco, its physician staffing joint venture, of which it now owns 90% from 50% previously. This unit reduced EBITDA by $100 million and margins by 80bp as revenue is undershooting expectations. Valesco helps provide hospitals and emergency rooms that are short-staffed with doctors, billing them for the labor. Once it was consolidated onto HCA’s financial midyear, this unit was supposed to bring in about $1 billion of incremental revenue with negligible EBITDA impact.

To be clear, this $100 million shortfall essentially represents two quarters of impact as claims are sent on a lagging basis. Valesco was consolidated into HCA’s financials during the last quarter , and it estimated $250 million of claims. That proved $50 million too high, which continued in Q3, resulting in a $100 million hit. As it maintains the same staff and just has seen them utilized far less than expected, this revenue shortfall has dropped straight to the bottom line. The magnitude of this miss from expectations is pretty jarring; as one analyst sa id on the call , “I've never seen a business kind of be off this far.”

For the full year, Valesco will take out $150 million of EBITDA and about $0.40 per share of EPS. Now, next year, because Valesco will be on the books for four quarters rather than three, HCA will see a year over year drag of $50 million in EBITDA and $0.13 in EPS. Just given the magnitude of the miss here, I am hesitant to model any incremental improvement and believe this unit will be a “show-me” story where evidence needs to be seen before it can be assumed.

Given this headwind, HCA tightened revenue guidance to $63.5-$64.5 billion from $63.25-64.75. It reduced the top end of its EBITDA guidance by $200 million to $12.3-12.6 billion while tightening EPS to $17.8-$18.5 from $17.7-$18.90. Excluding Valesco’s incremental impact, guidance is largely unchanged. EPS likely to be about $18.50-$18.75 ex-Valesco, results are still about 3-5% below the $19.25 in EPS I had expected as margin recovery has been weaker than anticipated, given persistent labor expense and unfavorable payer mix.

These headwinds have been offset partially by the fact the share count is down 5% from last year. HCA spent $1.14 billion of buybacks in the quarter. So far, HCA has generated $3.2 billion of free cash flow this year--$3.4 billion excluding working capital. For the full year, it should generate about $4.5 billion in free cash flow, which it is fully returning to shareholders via buybacks and its 1% dividends. The company carries $39.3 billion of debt from $38.1 billion at the start of the year. While it has $2.6 billion of debt maturing within 1 year, its debt has an average life of 9.6 years , significantly reducing its exposure to higher rates.

Even with its underperformance vs expectations, the company still has an under 14x P/E, and management has provided an optimistic outlook. At the company’s investor day in November, it announced an EBITDA growth target of 4-6% and 8-12% EPS growth. Now given the fact the company can continue to repurchase about $3-4 billion in stock from its free cash flow, thereby reducing its share count by 5-6%, this EPS outperformance relative to EBITDA makes sense. The question is what level of EBITDA growth can we expect.

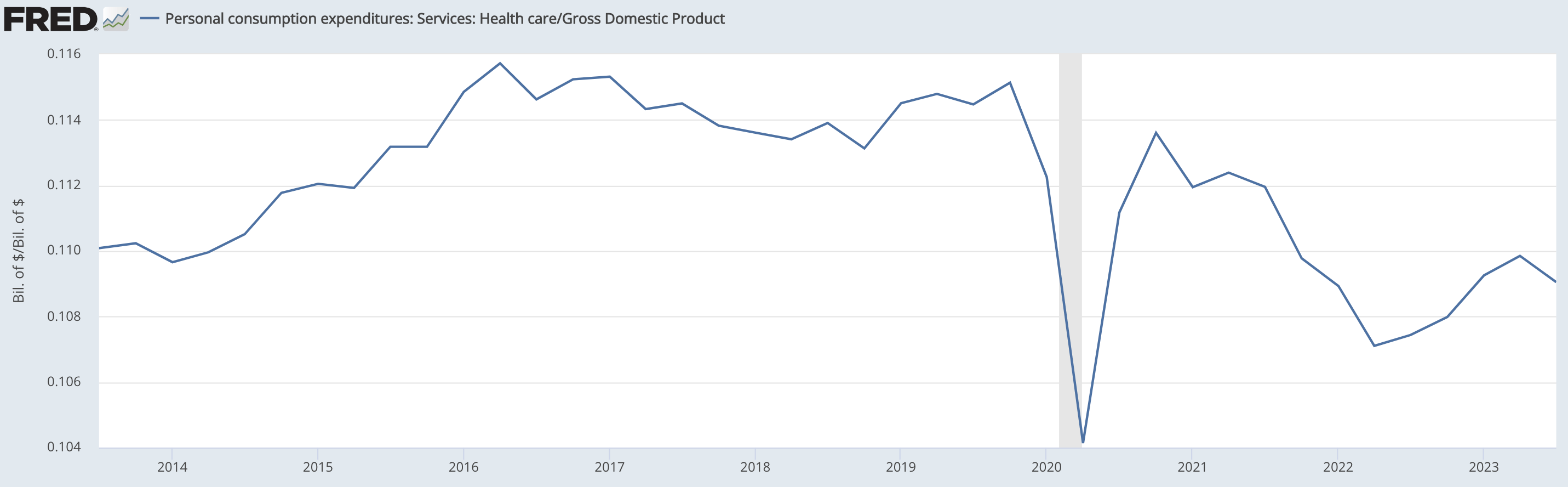

The incremental $50 million impact from Valesco is just about 0.45% of EBITDA. Whether the rest of the business can grow EBITDA by at least 4.5% is therefore the question. One reason I remain optimistic is that health care spending relative to GDP remains depressed. It is perhaps one of the more shocking aspects of the pandemic that health care services spending fell (as non-essential surgeries were limited) and never fully recovered. Particularly with an aging population, one would expect health care spending’s share of GDP to be stable or flat, at worst. Despite last quarter’s drop, spending has moved up from its 2022 low.

{kind=link}

St. Louis Federal Reserve

As such, I would expect health care services spending to rise at least as much as nominal GDP, if not a bit more as there is room for health care to recapture share of GDP. Even if one assumes just 1% growth and 2% inflation, that provides a 3% floor for next year’s health care spending growth. Health care is also less discretionary, in general, so its spending should hold up relatively well in a recession.

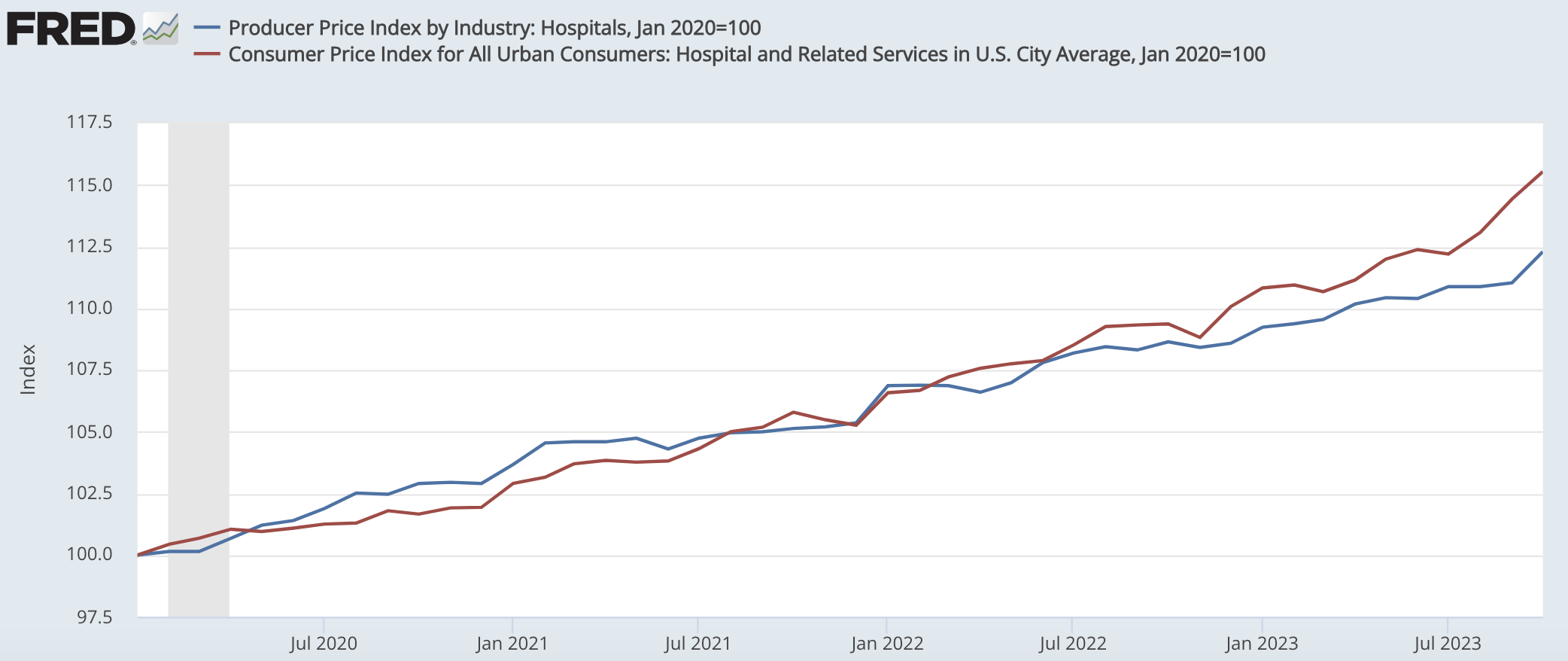

If we assume revenue growth of at least 3%, to get to 4.5% EBITDA growth, we would need to see HCA recover some lost margin, ex-Valesco, next year. With continued improvement in labor availability, I would expect labor costs to improve somewhat. It is also important to note that hospital CPI is now outpacing hospital PPI. When output prices are rising faster than input prices, this should widen margins for providers. From 2020 to June of 2022, they were matched. Now CPI is 3.2% higher. This should start to accrete to HCA’s margins, particularly if payer mix begins to stabilize, which it should with pandemic Medicaid policies having now rolled off.

{kind=link}

St. Louis Federal Reserve

I view 3% of revenue growth as a floor, and there should be some margin expansion. If we assume at least 20bp of margin expansion (or at least 1/3 of its Q3 unfavorable mix), EBITDA will grow 1% faster than revenue, or 4%. With the Valesco drag, EBITDA growth should be at least 3.6% next year. I would emphasize I view this as the floor, as I would not be surprised to see health care spending rise more quickly, though I concede the recovery has taken longer to materialize than expected. There should also be room for margins to expand even further.

Based on my view of 3.6-6.6% EBITDA growth, EPS growth should be at least 8.6% given my expectation for about 5% share count reduction. As such, I would expect HCA to earn at least $19.77 next year. That is just a 12.5x forward P/E. That is also my more cautious EPS estimate, given the slower recovery in health care spending and margin recapture. If we see more margin recovery, EPS could be closer to $20.25, but I believe some caution is merited given the underperformance in 2023 vs my expectations.

Given the company’s strong cash flow and long-term tailwinds for health care spending, I view that as an attractive multiple. While its $39 billion debt load does limit the scope for multiple expansion, I do see shares moving towards $280 next year, or about 14x earnings as we start to see further progress on margins, and the company deliver on high-single-digit earnings growth. I would stay long HCA.

For further details see:

HCA Remains Attractive Despite A JV Misstep