HCI - HCI Group: Impressive Margin Improvements But Unimpressive Price Point

2023-10-12 02:30:18 ET

Summary

- HCI Group Inc has consistently maintained solid and consistent margins in the insurance industry, with an average ROE of over 12%.

- The company specializes in residential insurance solutions and is well-positioned to benefit from the current real estate boom.

- HCI has been returning capital to shareholders through dividends and share buybacks, and its steady ROE enables continued practices in this area.

Introduction

The insurance space is not an easy industry to operate in as the companies have to constantly and consistently manage the risk profile and hedge against natural disasters and other weather-related events that could cause a surge in claims. This makes earnings reports possible to have quite different results sequentially. But that is the nature of the industry. One company in the industry that seems to have managed very well in regards to maintaining solid and consistent margins is HCI Group, Inc. ( HCI ). Over the last decade, it has averaged an ROE of over 12%. Right now though, the company is valued a little over my comfort zone and I don't think it exhibits such a strong buy currently. This makes me have a more neutral stance on the company and rate it a hold for now.

Company Structure

HCI along with its subsidiary companies, operates within the realms of property and casualty insurance, reinsurance, real estate, and information technology, primarily in the state of Florida. The company specializes in offering residential insurance solutions, including homeowners, fire, flood, and wind-only insurance, catering to a diverse range of clients, including homeowners, condominium owners, and tenants. Additionally, HCI extends its services to provide reinsurance programs, contributing to its comprehensive offerings within the insurance industry.

Market Growth (Investor Presentation)

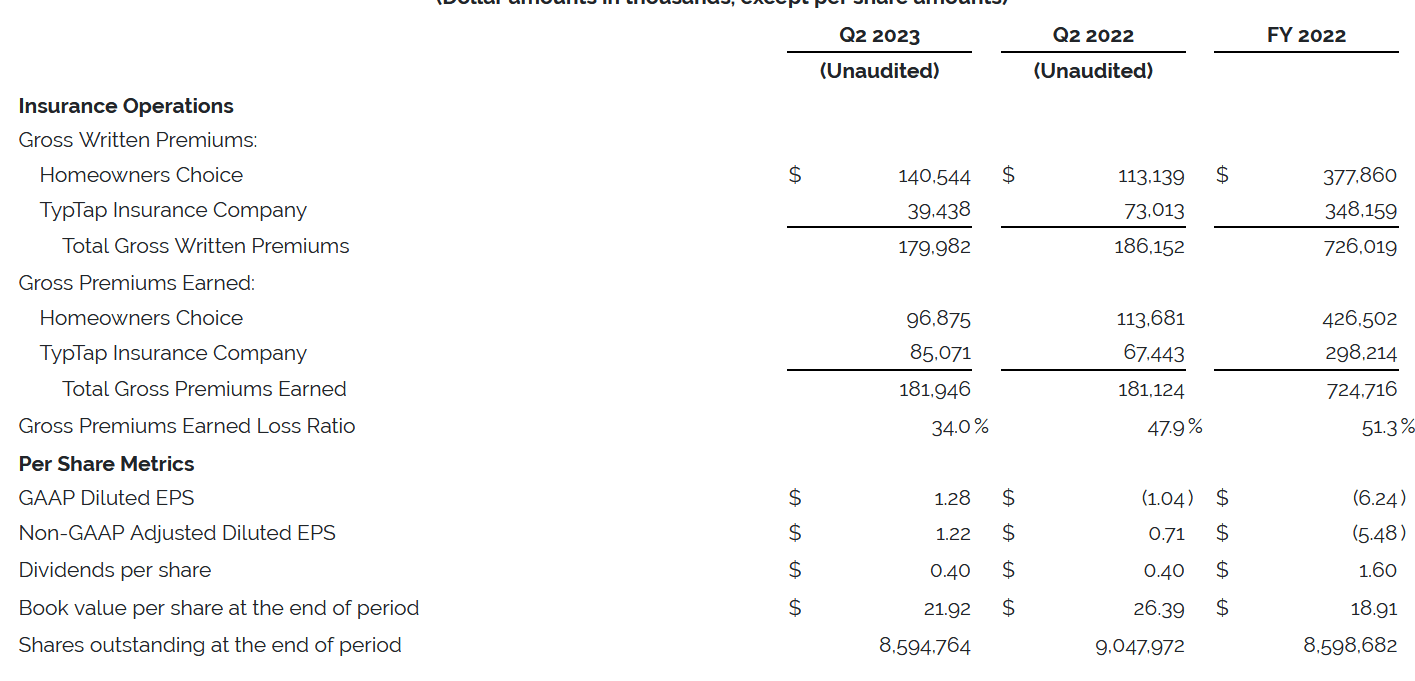

The current real estate boom could further stimulate demand in the housing market. A survey has revealed that a staggering 26 million Americans are interested in purchasing homes this year. This figure is significantly higher, about five times more, than the average number of homes sold annually, which typically ranges between 5 to 6 million units. This surge in potential homebuyers indicates a robust appetite for real estate investments in the market. Right now the company seems to have managed very well regarding improving the loss ratio and delivering a better margin. I think that given the ever-demanding real estate market there will always be buyers. That could be a dangerous statement to make, as we have previously seen crashes in the market, which came from bad loans rather than an overpriced market. Right now I think prices will remain elevated because of the lack of housing and the sizable amount of people willing to enter the market as well.

{kind=link}

The company has also managed to make strong progress on the front of returning capital to shareholders. Most recently the company continued to distribute its dividend and I expect it to continue doing so, but on a YoY basis, it has also been buying back large amounts of shares. From Q2 FY2022 to now they have gone down by roughly 6%. The steady ROE that HCI has been able to have I think is a key contributor here and something that will enable the management to continue having these practices in place.

Earnings Transcript

From the last earnings call that was held on August 8, the CEO of HCI Pareshbhai Patel had the following to say about the quarter and where the company is heading right now as well.

So overall, while earned premium has been roughly level year-over-year, the profitability of the business has improved considerably. And all of this is important as a backdrop because we now have a healthy stable business. We can now look to the future, and the obvious thing to do is to expand and grow the business, especially in Florida, and that is exactly what we plan to do".

This comment underscores very well why the company still can offer so much value to investors right now as it aims to grow the net written premiums but still ambient the margins. Margin retention in times like these is perhaps an even greater achievement than just simply growing premiums but the lack of growth in the bottom line because that expansion trickled down to increase operating expenses instead. It seems that HCI is on its way to delivering organic and sustainable growth over the long term and I am here to see more of it, just at a better price point hopefully in the near term.

Valuation & Comparison

p/b (Seeking Alpha)

I think that for HCI the rich valuation that I have mentioned reaches beyond just the earnings multiple, which is 63% above the rest of the sector. The book value of the company also seems quite rich at 2.4. In most cases, I am looking for companies in both the insurance space and the banking industry to exhibit a p/b or ideally under 1 to let me get the necessary margin of safety that I want. That is of course not the case with HCI right now and this leads me to have a less bullish stance on it in the near term. The price needs to drop significantly if I am to rate it a buy.

Risk Associated

One of the concerning factors associated with HCI at the moment is the notably high level of short interest in the company, which currently stands above 20%. This elevated short interest could exert downward pressure on the share price in the upcoming quarters. The market's pessimistic sentiment regarding the company's future earnings potential has contributed to this high short interest. It's important to note that going against the prevailing sentiment can sometimes result in investment losses. Given the substantial short interest, it's reasonable to adopt a more neutral stance when evaluating HCI's prospects.

Short Interest (Ychart)

Like all insurance companies, HCI faces the inherent risk of weather-related and natural disaster events that could lead to a surge in insurance claims and potentially impact the company's earnings. However, it's worth noting that HCI is currently a robust and well-established business that has consistently delivered steady returns over the past decade. Nevertheless, if a future earnings report were to reveal a lack of margin retention and a high volume of claims, it could lead to a market response in which the company's valuation is reduced by approximately 15% to 20%. This would bring its valuation more in line with the sector's median earnings, reflecting the potential impact of adverse events on the company's financial performance.

Investor Takeaway

The market seems quite conflicted on the prospects of HCI right now. On one side the share price has appreciated by over 30% in the last 12 months alone, but it also holds a short interest of over 20%. I don't like the valuation of the business right now and would prefer a significantly lower entry point. Nonetheless, the value of the business has to be admitted that the operational performance of HCI has been solid as they have held tight onto their margins. This leads me to rate it a hold for now.

For further details see:

HCI Group: Impressive Margin Improvements, But Unimpressive Price Point