HDB - HDFC Bank: A Bet On The Rapid Emergence Of India

2023-07-04 01:55:16 ET

Summary

- HDFC Bank has performed very well in the past year, as India continues to lead the world in real GDP growth.

- The company is well-positioned to benefit from India's fast-growing economy amid its young population and rising foreign investments.

- HDB's leading payment business should also be a growth driver, as the adoption and spending for credit cards continues to increase.

- The current valuation looks very reasonable when considering its strong earnings growth.

Investment Thesis

HDFC Bank ( HDB ) has performed very well in the past year with the share price up over 25% and is now back near its 52-week high. The company is at the heart of India's economy and should continue to benefit from the country's rapid expansion. It also has a great payment business that is well-positioned to benefit from favorable trends such as rising affluence and increasing technology adoption. I believe the company is a great option for investors to gain some exposure to the fast-growing Indian economy.

The Rapid Growth Of India

HDFC Bank is India's largest private bank with over 80 million customers and nearly 8,000 branches across the country. Banks' performance is generally highly correlated to the country's economy and I believe the company should benefit meaningfully from the rapid emergence of India.

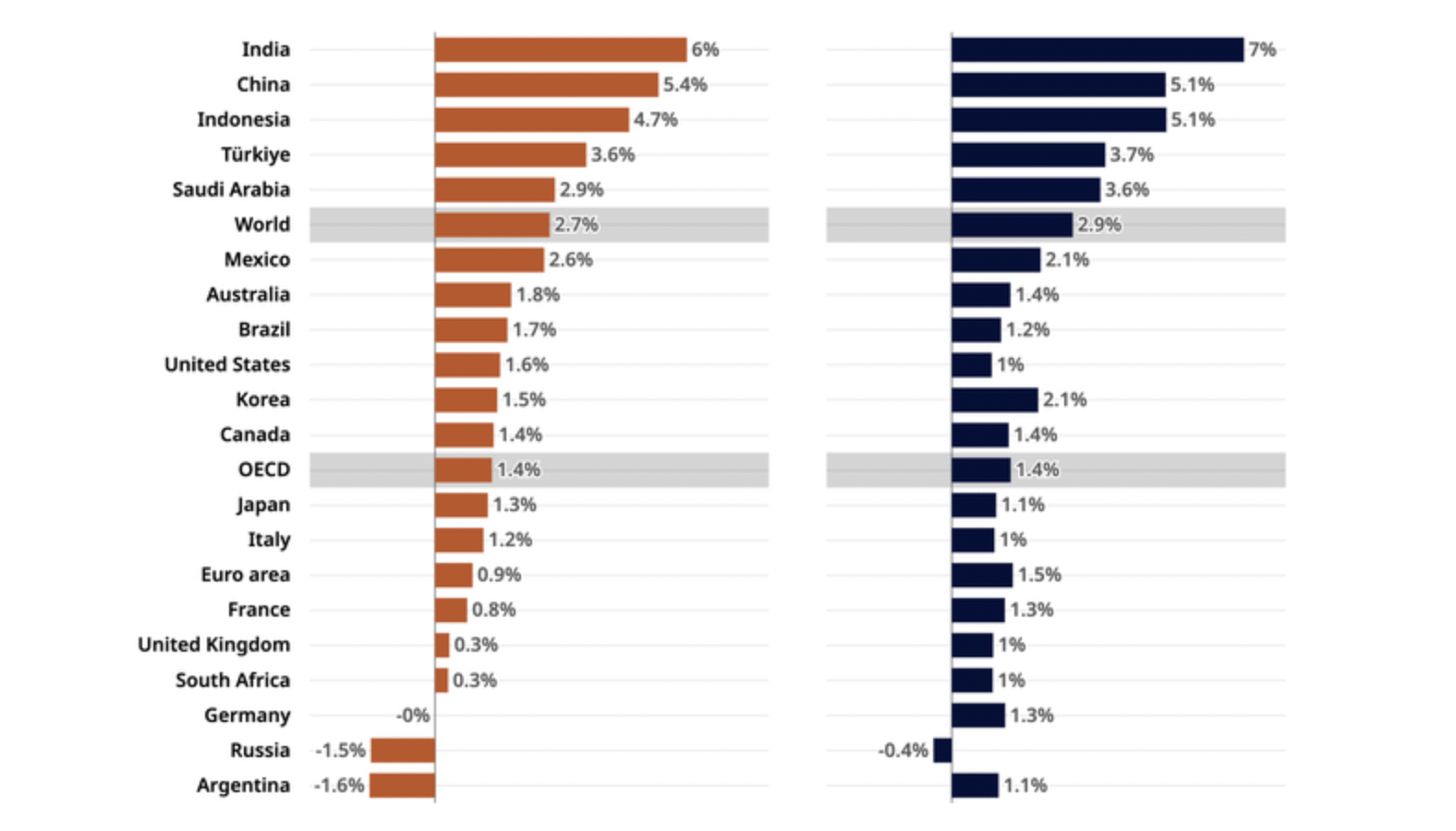

While the global economy has been slowing amid elevated inflation and rising interest rates, India continues to be an outlier with exceptionally strong economic growth. As shown in the chart below by OECD (Organisation for Economic Co-operation and Development), the country's Real GDP is forecasted to grow by 6% in 2023 and 7% in 2024, the highest among all countries. This is also significantly higher than the world's average Real GDP growth of just 2.7% and 2.9% for 2023 and 2024 respectively.

{kind=link}

The country should have a long runway for expansion as most of its population is young, with a median age of only 28. For instance, this is substantially lower than the US and China's median age of 38. This alongside improving urbanization, growing technology & infrastructure development, and rising affluence should continue to drive the country's economic growth.

India is also benefiting from the rising conflict between China and the US. Due to rising political concerns, many companies have been diversifying their supply chain and production into other countries. India's large population and land size make it one of the top alternatives for companies.

For instance, Apple ( AAPL ) has been pushing its suppliers away from China, and Foxconn Technology ( FXCOF ), its largest supplier recently announced a $500 million investment to build a new plant in India. The country now has 14 production sites for Apple and the number will only continue to grow in the future. The rapidly increasing foreign investments amid geopolitical tensions in China should be a major economic growth driver moving forward.

Strong Payment Business

HDFC Bank's payment business should be another major growth driver moving forward. According to the company , it is the largest issuer of credit cards in India with a solid market share of 28.6%. It is also the leader in off and online card acceptance, currently with a market share of 46% and 47% respectively. The strong payment penetration allows the company to benefit significantly from the rising affluence of the country. For instance, the company's credit card spending in FY22 grew 57% YoY (year over year).

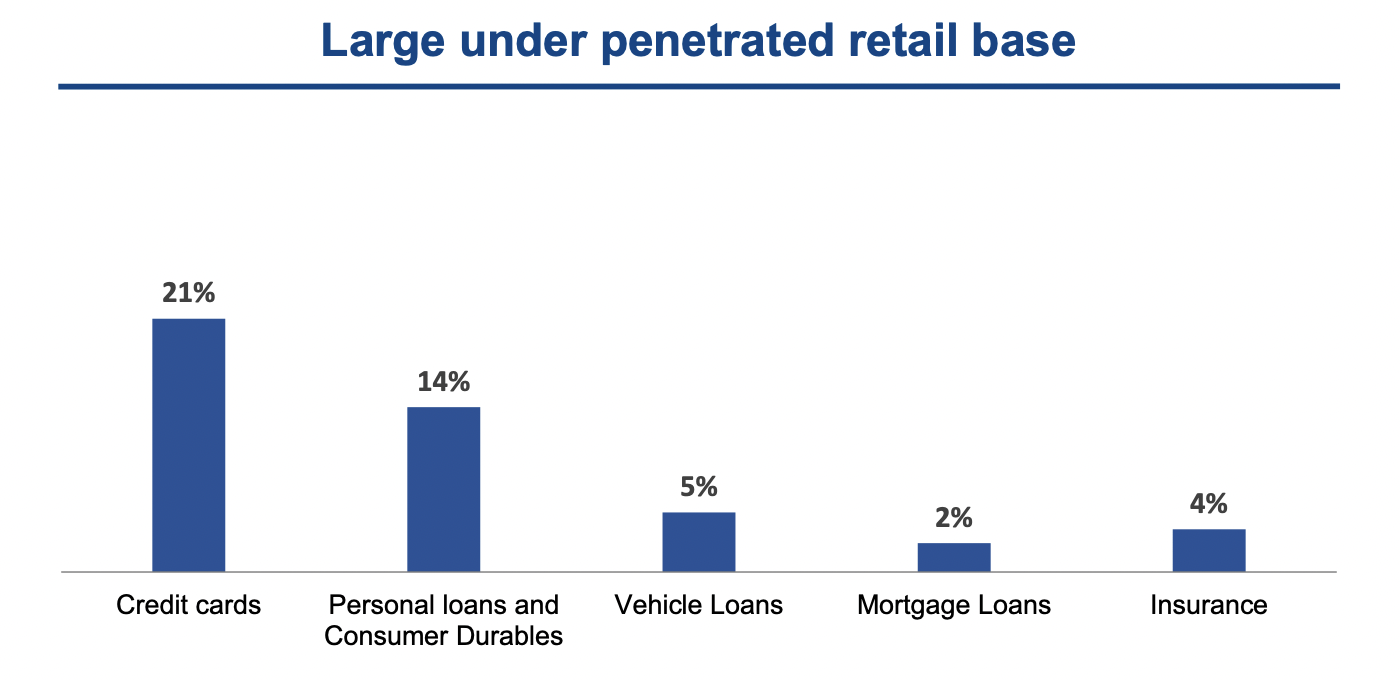

Despite the recent momentum, the overall adoption rate of credit cards remains extremely low in India. According to Forbes , only 5.5% of the country's population currently owns a credit card. Within HDFC, 21% of retail customers own a credit card. This should provide ample expansion opportunities for the company, as the popularity of credit cards continues to grow amid the ongoing increase in the population's spending power.

{kind=link}

Valuation

Despite trading near its 52-week high, the valuation of HDFC Bank is still very reasonable in my opinion. The company is currently trading at an fwd PE ratio of 19.8x, which is elevated compared to traditional banks such as Bank of America ( BAC ) and Wells Fargo ( WFC ). However, I believe we also have to factor in growth as HDFC Bank has been growing rapidly amid the fast-growing Indian economy.

According to Seeking Alpha's estimates , Bank of America and Wells Fargo are expected to grow EPS by 6.5% and 6% in the coming year, which gives them an fwd PEG ratio (PE ratio/ EPS growth) of 1.3x and 1.5x respectively. On the other hand, HDFC Bank is expected to grow EPS by 22%, which translates to an fwd PEG ratio of just 0.9x. Therefore, HDFC Bank is actually cheaper if we take the growth rate into consideration.

Risk

While India's economy has been doing well, it may still be impacted by the slowdown in other countries. For instance, Germany recently entered a recession while China's reopening is also running out of steam. As mentioned above, a part of the country's growth comes from the rapid increase in foreign investments. If the economy in other countries worsens meaningfully, companies will likely become much more cautious and slow down on spending. The decline in global demand will likely also impact the country's export.

Investors Takeaway

I believe HDFC Bank is a compelling bet on the Indian economy. India is forecasted to lead the world in real GDP growth in the next two years and it should have a long runway as most of its population is still very young. The political tension between China and US is also pushing a lot of companies' production into India, which should further boost growth.

The company's leading payment business should also be a meaningful growth driver as the adoption and spending for credit cards continue to increase. The favorable backdrop should enable the company to generate strong growth moving forward, therefore I rate it as a buy.

For further details see:

HDFC Bank: A Bet On The Rapid Emergence Of India