HDB - HDFC Bank: Merger Done A New Chapter Begins (Rating Downgrade)

2023-09-09 01:30:41 ET

Summary

- HDFC Bank closes its merger with former parent company HDFC.

- There are clear scale economies here long term, but in the initial phases of integration, expect some P&L headwinds.

- The stock has de-rated, but rightly so, given HDFC's lower margin book and the increased complexity of the pro-forma entity.

Having developed into India's largest private sector bank under mortgage finance company HDFC's umbrella, HDFC Bank (HDB) has finally merged with its parent company to create one of the world's largest retail and corporate banking franchises. While the stock has traded down post-merger, the combination strikes me as a synergistic one, given access to a larger customer base and more cross-selling opportunities off the combined HDFC/HDFC Bank product suite.

But the increased complexity is a drawback - post-merger, the bank's financial profile will look much like other Indian banking conglomerates (e.g., peer ICICI (IBN)), eroding its overall ROEs and the significant P/B premium HDFC Bank has benefited from in the past. And with the Reserve Bank of India (the 'RBI' or India's central bank) ultimately headed for monetary easing once India's supply-driven inflationary pressures clear (note the central bank pre-emptively withdrew system liquidity last month), expect more net interest margin pressure ahead. At ~2.6x book , the stock isn't cheap either, and there are probably better ways to play the Indian growth story from here.

Q1 Offers First Insight into Post-Merger Economics

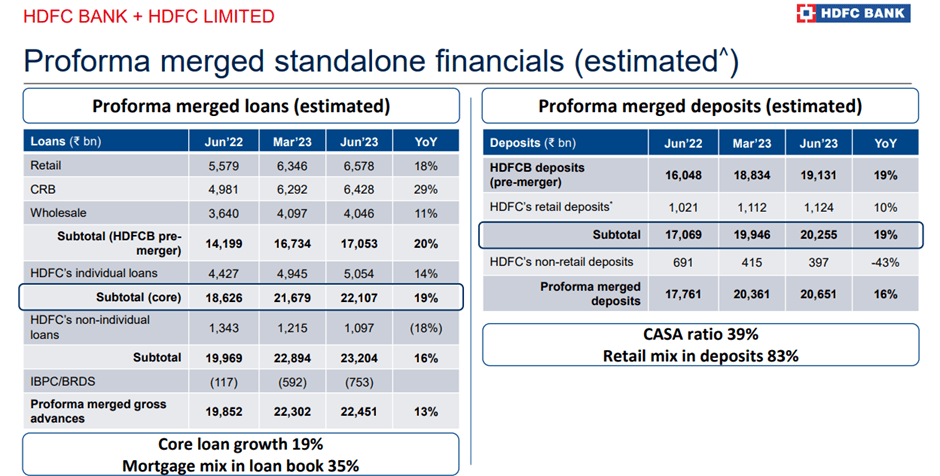

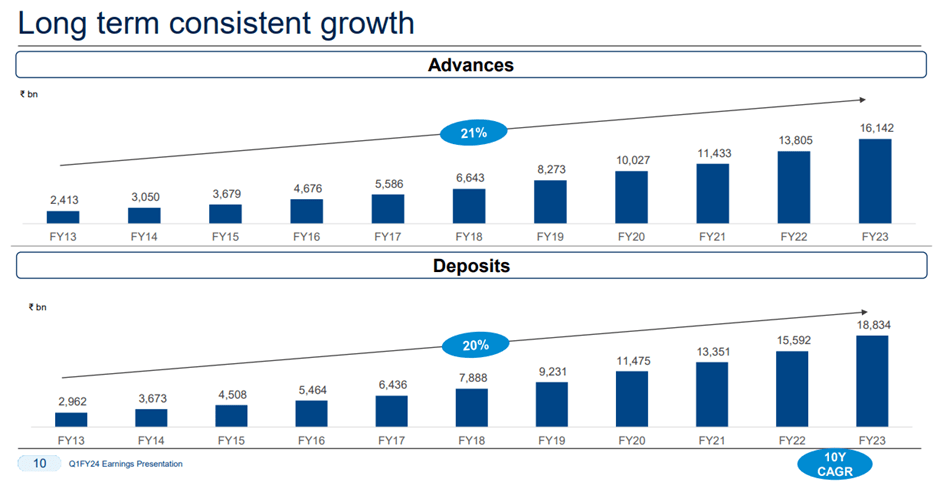

HDFC Bank's first quarter of fiscal 2024 saw headline loan growth rise +16% YoY, though net of wholesale loan sell-downs and transfers through inter-bank participation certificates (i.e., a short-term money market instrument for inter-bank sales of bank loan assets), growth was closer to a more impressive +20% YoY. More pertinently, the merged loan book (i.e., pro-forma HDFC/HDFC Bank) grew at a slower +13% YoY pace, largely weighed down by HDFC's wholesale and corporate loan books; excluding these, loan growth would have been up +19% YoY for the merged entity. While a further run-down of the wholesale book is still expected, it has been scaled down significantly and should, thus, pose less of a headwind for overall loan growth going forward.

{kind=link}

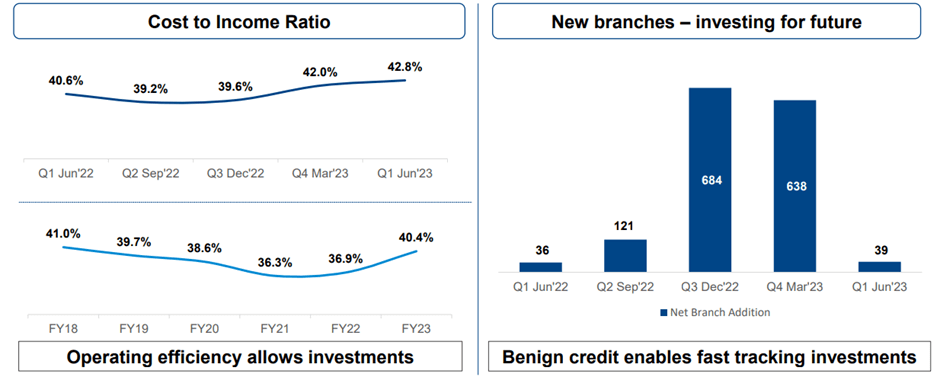

On the other side of the balance sheet, deposit growth hasn't been too great overall. While standalone HDFC Bank posted +19% YoY growth in Q1 2024, parent company HDFC's deposit base was a major drag at -43% YoY for non-retail and +10% YoY for retail. Relative to system growth, this implies overall market share gain in deposits may be slowing down. Expect more churn as the post-merger integration plays out, though deposit growth tailwinds from HDFC Bank's branch additions (accelerated over the last year or two) should also provide some offset. Similarly, the cost-to-income ratio might see some upward pressure from an already elevated 42.8% Q1 2024 base as the integration plays out and as management continues to grow its physical branch footprint.

A More Diversified Loan Book Post-Merger

As the Q1 report highlighted, the shift in portfolio mix post-merger will be the most striking change for HDFC Bank. Given parent company HDFC's concentration on mortgages, expect an increased share of home and property-secured loans in the overall book, along with a longer average tenor. The timing is good amid a property upcycle backdrop in India backed by fundamental residential demand rather than speculation. But a more mortgage-heavy book also comes at the expense of net interest margins - note HDFC runs a lower-margin mortgage business and, by extension, sustains lower net interest margins through the cycles.

Also concerning is that regulatory reserves from HDFC's balance sheet will come onto HDFC Bank after the merger, at least in the initial years. But the RBI allowing HDFC Bank to term out some of the incremental priority sector lending requirement ('PSL') over three years, for instance, also reduces the overall regulatory P&L drag somewhat. Depending on how much near-term balance sheet stress HDFC Bank comes under amid ongoing weather headwinds (particularly agricultural loans, which drove the non-performing share of loans slightly higher in Q1), investing behind its branch expansion and digital initiatives could slow for now. But over the mid to long term, HDFC Bank's best-in-class risk management remains intact, and I expect the merged entity will continue outpacing the overall system (albeit by a smaller margin).

{kind=link}

Leaning into Cross-Selling Opportunities

While taking on the lower-margin HDFC book will be dilutive initially, the merger could unlock some P&L synergies. For one, home loans tend to be 'stickier' and come with a longer duration, allowing for more cross-selling opportunities over the life of the relationship. Per management, deposits associated with these loans are also lower beta, facilitating an accretive shift away from an increasingly competitive wholesale funding backdrop toward retail. So, assuming management successfully executes this shift and keeps opex down post-merger, there's a clear path to HDFC Bank recovering its net interest margins over time.

Another key piece of the puzzle is management's disclosure that ~70% of HDFC's customers do not bank with HDFC Bank. Hence, the size of the cross-selling accretion could still surprise to the upside, particularly with direct access to a comprehensive fee-paying suite comprising insurance, brokerage, and asset management to offer customers. This should supplement its ongoing investments in digitalization and branch expansion, with continued branch additions in Q1 2024 signaling management isn't slowing down anytime soon. While another ~1.5k/year of branch additions is in the pipeline for the next few years (matching the pace pre-merger), I wouldn't be surprised to see some pullback in growth while the integration takes place.

{kind=link}

Merger Done, a New Chapter Begins

Having finally closed its merger with parent company HDFC Limited, HDFC Bank stock has traded down in recent months against a broader rally in Indian equities. The merger rationale still applies, in my view - the synergies from cross-selling into an expanded customer base, as well as a housing-driven shift on both sides of the balance sheet, remain key drivers of the long-term accretion potential. But in the near term, the increased regulatory costs post-merger (mainly related to priority sector lending) is an issue, along with the increased complexity of the conglomerate structure (subsidiaries include insurance, brokerage, asset management arms, etc.). So, while I still like HDFC Bank's share gain prospects within a growing system, the current relative valuation discount to ICICI Bank (albeit still at a wide premium to other Asian banks at ~2.6x book) seems justified.

For further details see:

HDFC Bank: Merger Done, A New Chapter Begins (Rating Downgrade)