CDDRF - Headwater Exploration: Solid Upside At Moderate Risk

Summary

- If you are bullish oil but are worried about stock market volatility due to a recession, what stock should you invest in for 2023?

- In this piece, I will look at Headwater Exploration, a pure-play heavy oil producer in the rapidly-growing Clearwater play in Canada.

- I will show through my analysis how Headwater's steady production growth, high profit margins, strong balance sheet, and undervaluation offer investors an attractive risk-reward profile.

In a recent piece , I argued for investing in energy stocks in the current market by stating

"Going forward, as such artificial manipulative measures as SPR releases and zero-Covid conclude, we will likely find tailwinds gathering strength in the near future... I continue to believe the structural oil bull market is intact in the medium to long term, and the physical oil supply-demand dynamic remains strong in the near term in spite of the apparent weakness in the financial oil market."

However, I will stick to high-quality names in accordance with the stock-picking principles that I discussed in interviews with Seeking Alpha in 2020 and 2021 , and in anticipation of market volatility due to a possible recession. Previously , we selected Magnolia Oil & Gas Corp. ( MGY ) after careful consideration of several U.S. operators, reflecting my belief that investors should adjust their energy portfolio as the oil cycle progresses. Below, I'd like to focus on Headwater Exploration Inc. ( CDDRF ), a Canadian producer.

Headwater Exploration

Let's look at Headwater from the angle of production growth and cost management.

Growth

In the first nine months of 2022, Headwater invested C$184 million of capital, more than doubling that in the same period in the previous year. The company guided toward a CapEx of C$245 million for full-year 2022, up 75% from 2021. Consequently, daily average production grew at a good clip; from 2021 to 2022, production will increase by 75.84% (Fig. 1), which is among the fastest production growth among Canadian small independents. There is more production growth to be expected in the next five years; Headwater is poised to expand production to 25,000 boe/d by 2027.

{kind=link}

Fig. 1. Production profile of Headwater Exploration, by quarter and by year, actual and expected (Laurentian Research for The Natural Resources Hub, based on Headwater financial filings)

Driving the significant increase in production is the company's success in exploration and the secondary oil recovery program:

- In Marten Hills West, Headwater was able to extend the proven pool boundaries by ~3.5 miles by drilling one outpost well in the 3Q2022. A significant amount of road and pad construction dollars spent in Marten Hills West in 2022 will provide the company with the ability to drill the next 100 wells in 2023 and beyond with minimal civil construction.

- In the Marten Hills Central area, Headwater drilled two successful pool extension wells in the 3Q2022. The company brought on-stream an oil processing facility in the area in the 1Q2022, and continued to ramp up the waterflood program for secondary oil recovery. Headwater is on track to have 65% of Marten Hills Central under waterflood in the 1H2023. Waterflood is supposed to lead to shallower natural decline.

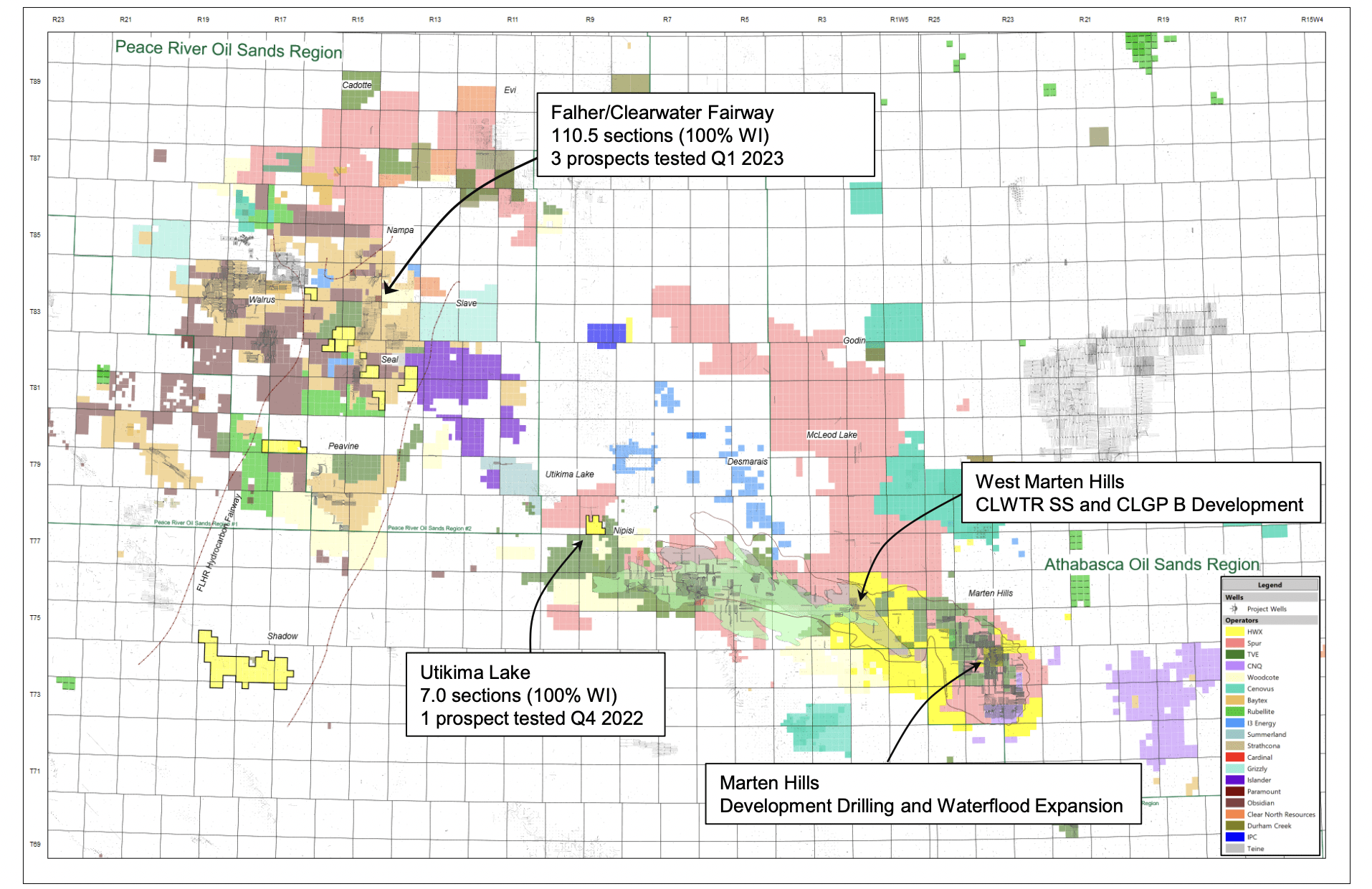

- In the Greater Peavine area, unfortunately, Headwater plugged and abandoned two stratigraphic test wells as dry holes in the Shadow area in the 4Q2022 (Fig. 2).

Based on the successful exploration and waterflood efforts, I am confident that Headwater will report significant growth in reserves for 2022.

{kind=link}

Fig. 2. A map showing the Clearwater play, especially with Headwater's footprint (Headwater Exploration)

Costs

The oil processing facility that was commissioned in the 1Q2022 led to reduced oil transportation costs. Cost savings therefrom, fully realized since the 2Q2022, resulted in annual corporate transportation expenses of ~C$4.00/boe in the 2Q and 3Q2022, down from C$8.21-8.68/boe as in the same quarters one year ago.

In contrast to the increasing royalty due to rising oil prices, Headwater succeeded in reducing per-boe costs substantially through investments in infrastructure and economies of scale driven by production growth (Fig. 3). This enables the company to sustain a high profit margin.

{kind=link}

Fig. 3. Unit cost structure of Headwater Exploration (Laurentian Research for The Natural Resources Hub based on Headwater financial filings and Seeking Alpha)

It is also worth noting that the McCauley gas field, which is only brought on-stream seasonally from November to April and shut-in during summer months, is truly a cash cow. The field is estimated to pull in C$30 million in operating cashflow in the 2022-2023 winter season for a maintenance capital of less than C$0.5 million. The resultant free cash flow (C$29.5 million) is more than enough to offset the ~C$6 million corporate G&A expenses estimated for the entire 2022.

Free cash flow

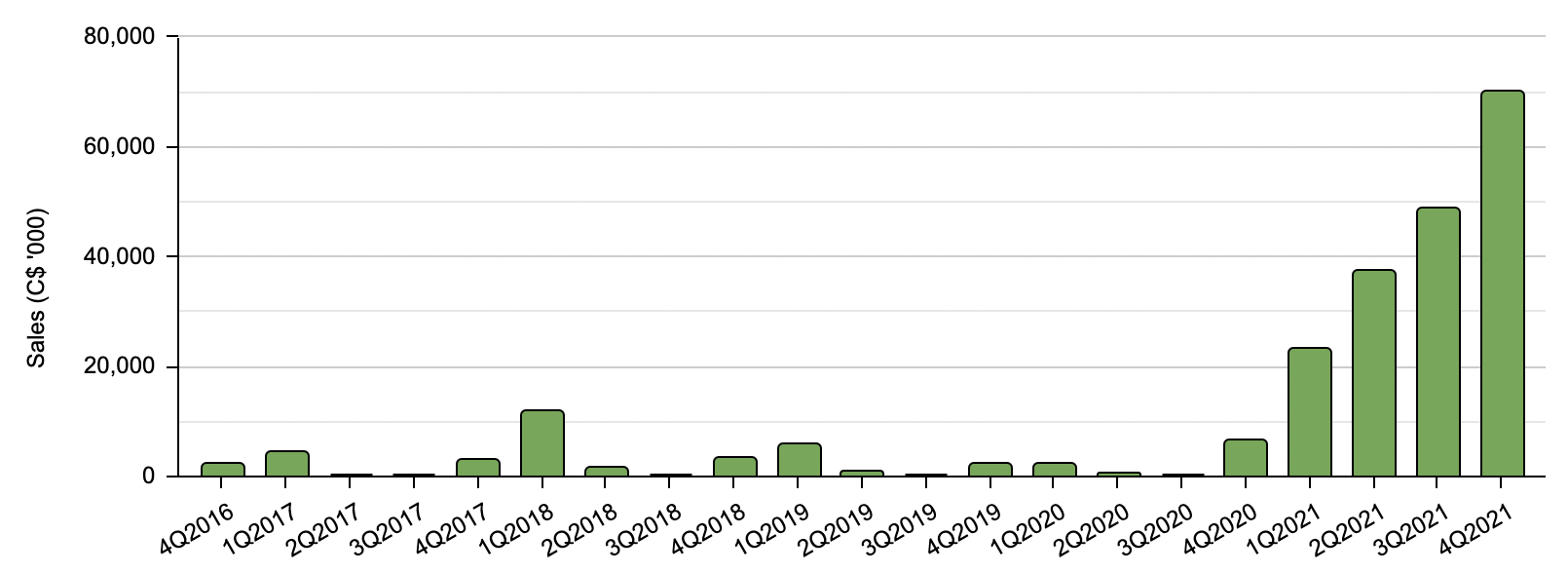

Headwater Exploration made significant capital investments in 2020 and 2021, and in 2022 saw a tremendous increase in revenue and its first positive free cash flow in two years as a result (Fig. 4; Fig. 5).

It is anticipated that the momentum from production expansion and cost savings will continue to drive strong free cash flow in the future. According to its five-year capital program, Headwater expects to increase annual free cash flow from C$42 million in 2022 to C$268 million (under US$75/bo WTI) or C$324 million (under US$85/bo WTI) by 2027.

{kind=link}

Fig. 4. Quarterly oil and gas sales of Headwater Exploration (Laurentian Research for The Natural Resources Hub based on Headwater financial filings and Seeking Alpha)

{kind=link}

Fig. 5. Annual free cash flow of Headwater Exploration, actual and projected (mid-point estimates under assumptions of US$75 and US$85 WTI) (Laurentian Research for The Natural Resources Hub based on Headwater financial filings and Seeking Alpha)

Capital allocation

With the outlook of increasing free cash flow, Headwater declared the inaugural quarterly cash dividend of C$0.10 per share, starting to implement a return of capital strategy. The dividend, payable on January 16, 2023, implies a dividend yield of 6.76%, using the share price of C$5.92 as of December 30, 2022. Headwater indicated that the dividend was safe above US$55 WTI.

Valuation

It is no wonder that Headwater has been able to pull off growing production and revenue rapidly, generating an increasing amount of free cash flow, and transitioning into a decent dividend payer, while maintaining positive working capital with no outstanding bank debt. The incredibly good geology of the Clearwater play makes it the most economical resource play in North America: shallow reservoirs; multilateral wells; open-hole and unstimulated completion; cold flow.

The critical question concerning Headwater, however, is whether all of those favorable attributes justify a C$1.38 billion market cap.

How much can Headwater sell for as a company? On September 12, 2022, fellow Clearwater operator Tamarack Valley Energy ( TNEYF ) acquired Deltastream Energy Corp. , a privately-held pure-play Clearwater oil producer, for C$1.425 billion. At the time, Deltastream produced at ~19,000 bo/d, implying a metric of C$75,000 per bo/d of production. If we use the Deltastream transaction as an analog, at the projected 4Q2022 average production of 16,176 boe/d, Headwater is supposed to grab C$1.213 billion in M&A. Adding cash of C$118 million, Headwater is worth C$1.331 billion or C$5.7 per share.

Apparently, Headwater is more than fully priced by the market at this time. However, we must factor in the highly visible near-term growth. Headwater is expected to exit 2023 at ~19,000 boe/d and add ~C$37 million of working capital. That suggests the stock is worth C$6.77 per share, which implies a 14.35% upside from the current share price or, if the 6.76%-yielding dividends are considered, a total return of 21.11%. That is pretty good considering Headwater shareholders are exposed to relatively low risk.

However, if an investor wants a higher total return, he will need to wait for the share price to drop significantly below the current level. A flash crash of oil prices in the event of a recession, e.g., could cause a selloff of the stock, creating an entry opportunity. However, high-quality names such as Headwater tend to be the first group of stocks to be bid up. So, it is highly unlikely the stock will stay depressed for long.

Risks

The biggest risk for Headwater shareholders is a significant drop in the price of oil below US$55 WTI, which could result in the company suspending dividends and abandoning its capital plan. While it is not impossible for there to be a severe oil market crash, it is highly unlikely that the WTI benchmark will stay below US$55/bo for an extended period of time due to the reasons previously mentioned. Additionally, a wider WCS differential could also negatively impact Headwater's oil price realization (Fig. 6).

{kind=link}

Fig. 6. WTI, WCS and the differential between them (modified from Alberta Government)

Although there may be instances of unsuccessful exploration drilling in specific areas, such as Headwater's experience in the Shadow area, the Clearwater play has been largely de-risked at a regional level with regard to subsurface geological uncertainty (Fig. 8). In terms of jurisdiction, Canada has a royalty system that utilizes a sliding scale linked to commodity prices , which helps to protect investors from the risk of new windfall taxes.

Shareholder takeaways

For investors who expect volatile oil prices in 2023 and beyond, Headwater Exploration is a strong choice at its current share price.

- It has exceptional well economics and a cost structure that is among the best in North America, with a very low breakeven point (~C$32/boe) and high profit margin.

- The company's McCauley gas field generates enough free cash flow to cover its corporate general and administrative expenses, providing additional stability in a low oil price environment.

- The management team, which is highly respected in the oil industry in Calgary, is both highly skilled and focused on maximizing returns for shareholders.

- Unless low oil prices continue after an economic recession, there are few risks that could prevent Headwater from achieving rapid and profitable growth in the coming years.

Investors who are risk-averse and prefer a larger margin of safety may need to wait for a significant event that causes the share price to fall to levels such as below C$5 (Fig. 7). However, this tactic carries the risk of missing out on the opportunity altogether, as high-quality companies like Headwater tend to perform better than low-quality ones during market downturns.

For further details see:

Headwater Exploration: Solid Upside At Moderate Risk