NSIT - Headwaters Capital - Insight Enterprises: Cheap Valuation Improving Financials A Compelling Opportunity

2023-07-28 12:00:00 ET

Summary

- NSIT is a technology solutions integrator that enables digital transformation for large corporations through consulting, procurement, implementation, and maintenance services.

- The company's market share gains are driven by its scale of product distribution, breadth of vendor relationships, and depth of IT expertise.

- NSIT's shift towards higher-margin software and services revenue, along with its potential for multiple expansion, is expected to improve margins and ROIC.

The following segment was excerpted from this fund letter.

Architect and General Contractor Enabling Digital Transformation

Thesis

- Ongoing IT innovation and increasing IT complexity serve as secular tailwinds for NSIT’s solutions integrator business model.

- Market share gains driven by scale of product distribution, breadth of vendor relationships and depth of IT expertise.

- Margin and ROIC improvement from portfolio mix shift to a greater proportion of software and services revenue, augmented by specific margin improvement efforts in each product line.

- Multiple expansion potential as revenue contribution from higher margin and less cyclical software and services revenue grows.

Company Overview

Insight Enterprises ( NSIT ) is a technology solutions integrator serving Fortune 500 companies globally. NSIT defines solutions integrator as a partner that can leverage technical expertise to deliver products, software and services that solve a client’s needs. I think it is easier to think of the company as an end-to-end enabler of digital transformation for large corporations. NSIT’s team of 4,500 IT experts can provide upfront consulting services to design a project roadmap to solve a client’s IT needs. NSIT then leverages the company’s roots as an IT reseller, where it’s relationships with over 6,000 OEMs and expertise with supply chain procurement and customization is a key differentiator versus traditional consulting firms. NSIT’s IT experts can then implement the project for the client and provide ongoing maintenance services following completion. This full life cycle management differs from pure IT resellers who don’t have the technical expertise for complex projects and from pure consulting firms who don’t have the supply chain procurement expertise. Specific digital transformation focus areas for NSIT include cloud migrations, infrastructure modernization, cybersecurity, modern apps and data/AI.

Source: Insight Enterprises Investor Presentation (Q2 2023)

{kind=link}

A representative project helps to provide a more concrete overview of the business. NSIT has used the example of a global airline that is introducing in-flight payments for food and beverage (slightly dated example, but helpful in understanding the business). While this seems like a simple project, it is far more complex than it appears on the surface. NSIT might be engaged upfront through a consulting project where the company’s IT experts can provide advice on appropriate hardware and software for the project. NSIT would then be hired to procure the hardware and customize the devices with credit card readers and customized corporate packaging. Devices must also be configured with software that ties into existing corporate systems as well as cybersecurity protection. Given the volume of devices for a project of this size, customization is performed at one of NSIT’s integration centers. Once the devices have been configured, NSIT handles the distribution of these devices globally. Finally, NSIT can manage the maintenance and replacement of these devices once they have been distributed. In this example, global scale, product breadth and supply chain management are critical to this complex IT solution.

Like the example above, NSIT’s business has historically revolved around procurement, customization, and management of client devices (laptops, desktops, etc). However, through a series of acquisitions and internal human capital development, NSIT has built a team of IT experts focused on consulting and implementation for data centers and cloud migration. Cloud migrations, specifically, are complex projects that require upfront consulting engagements and the procurement of multiple hardware, software and infrastructure products.

Following implementation, these IT projects carry more back-end maintenance and service revenue for NSIT. As discussed in detail below, this shift to more software and services will benefit margins and ROIC going forward and is a critical piece of the NSIT investment opportunity.

IT Distribution Industry & Competitive Positioning

The solutions integrator business model is a bit of a gray area in the IT distribution and services landscape. NSIT has overlap with customers/competitors in the IT reseller space, IT distribution, business process outsourcing and IT consulting. NSIT’s differentiation lies in its IT reseller background combined with a deep pool of IT experts.

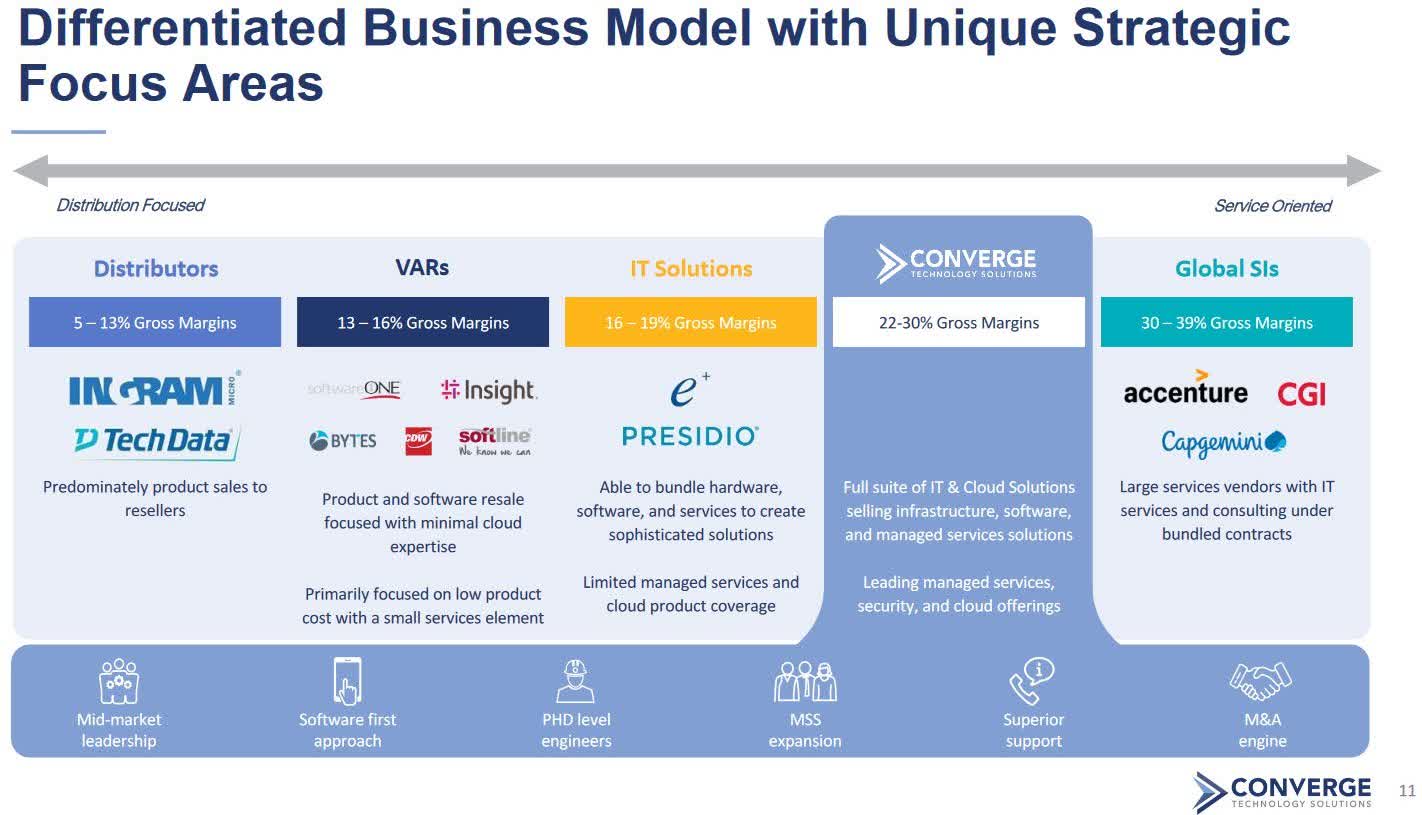

Converge Technology provides a good overview of the competitive landscape and where each company fits in the value chain.

Source: Converge Technology Solutions Investor Presentation (June 2023)

{kind=link}

NSIT’s role in the IT value chain is important to both vendors and customers. NSIT serves as an outsourced sales and implementation provider for OEMs, who can’t profitably operate a competitively scaled sales and service infrastructure (especially smaller OEMs). From a client perspective, NSIT offers a similar outsourced service in that they provide objective consulting, procurement and implementation expertise to customers across an extensive range of products (6,000 OEM relationships). As the IT landscape becomes more dynamic and complicated, the broad expertise of NSIT’s IT specialists only grows in importance. NSIT noted that an average project has ten different partners, which highlights the value that NSIT can provide to both OEMs and customers via coordinating these complex digital transformation projects. Hence the construction analogy: NSIT serves as the architect on the project upfront and then acts as the general contractor, overseeing the implementation of the roadmap through to completion.

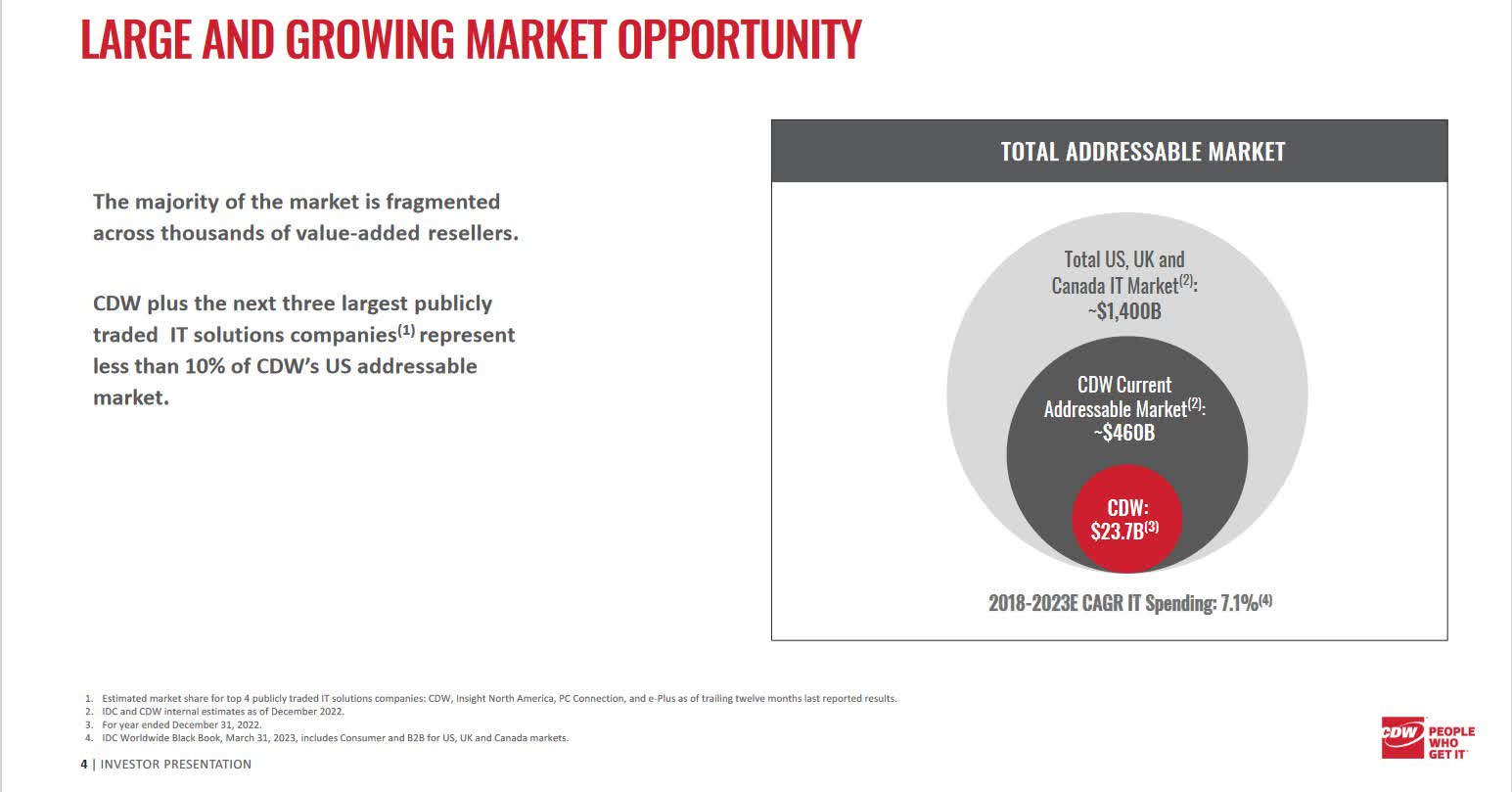

The IT solutions market is highly fragmented, with the top 4 players representing only 10% of the market.

Source: CDW Investor Presentation

{kind=link}

NSIT has a significant scale advantage relative to the fragmented set of smaller competitors, which is even more important for large corporate customers. Smaller competitors do not possess the geographic footprint required to serve these global customers. Additionally, few companies have the breadth and depth of NSIT’s vendor relationships, again positioning NSIT well when serving the diverse needs of large corporations.

CDW is the closest competitor to NSIT, but primarily competes in the SMB space and doesn’t have significant overlap with NSIT in the large corporate market. CDW’s focus on SMB enables higher margins and lower working capital requirements as payment terms are shorter for SMB customers versus large enterprises. Smaller publicly traded peers and a fragmented landscape of private competitors that typically have a specific vendor or customer relationship present limited competition for NSIT in the large enterprise space.

Given the fragmented competitive landscape combined with the sheer size of the market, the industry has historically seen steady consolidation. Acquisitions are strategically attractive as smaller companies often fill product and/or geographic gaps, thus increasing the scale advantage of larger players. Additionally, M&A is financially accretive as there are often significant expense synergies realized through consolidation.

IT Industry Growth

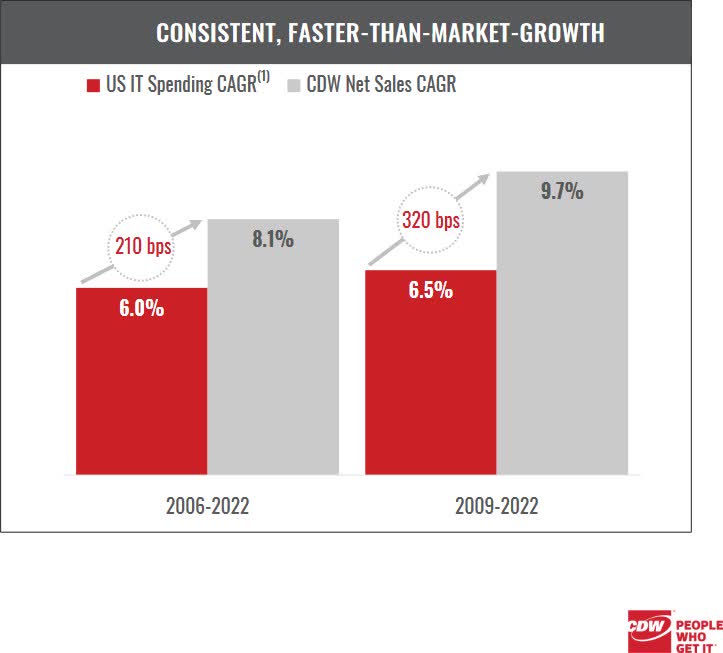

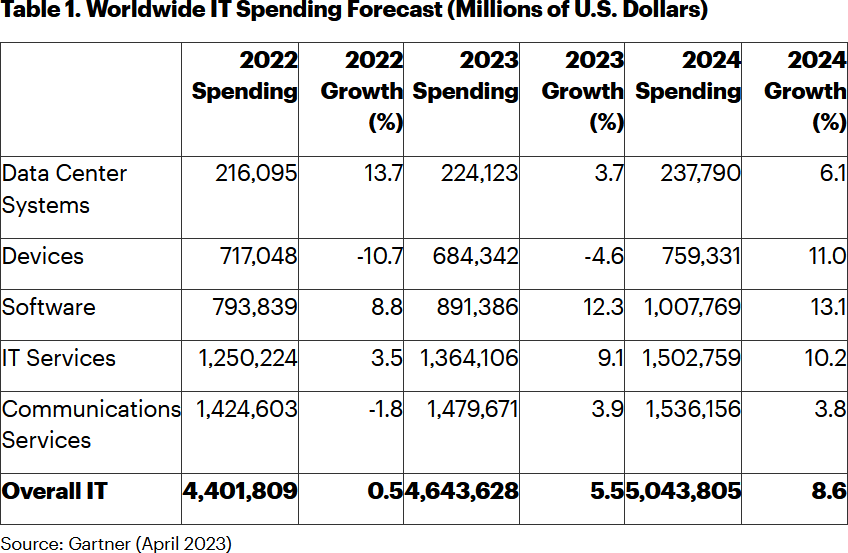

Through a cycle, IT industry growth generally outpaces GDP by 200-300bps. Although backward looking, CDW provides good data on historical IT spend that has averaged ~6%. Given a growing focus on broad digital transformation combined with growing complexity in the IT landscape, I would expect this to be a floor growth rate for the industry going forward.

Source: CDW Investor Presentation, IDC Worldwide Black Book December 31,2002

{kind=link}

NSIT is focused on the fastest growing areas of IT spending, which should enable the company to organically outgrow broader IT spending through a cycle. Additionally, faster growth of software and services will enable margin expansion and reduced capital intensity.

{kind=link}

NSIT’s largest OEM partner is Microsoft, which accounts for 14% of NSIT’s total revenue. NSIT’s partnership with MSFT also supports industry outperformance as a result of Azure’s leading position in the cloud migration trend. Interestingly, legacy MSFT relationships provide a pipeline for future cloud conversions (as opposed to AWS/Google Cloud which don’t have the legacy on-prem infrastructure).

Financials

Initially, the margin profile and inherent cyclicality of the hardware business appear to be a poor fit for the Headwaters portfolio. However, NSIT’s cheap valuation combined with an improving financial profile due to broader industry trends and internal initiatives make NSIT a compelling opportunity. As described above, hardware sales previously accounted for the majority of NIST’s revenue. Hardware revenue carries lower gross margins, which depressed overall gross margins. The hardware business is also capital intensive given the significant inventory required to support this business and extended payment terms from large enterprise clients. As the software and services mix of NSIT’s business grows, margins will naturally improve due to this mix shift.

NSIT has also outlined specific steps that will improve the gross margins within hardware, software and services in addition to the positive mix shift. Furthermore, software and services sales are capital light, which will support an improved ROIC. Management laid out long-term guidance that incorporates these dynamics and is expected to lead to a significantly improved financial profile by 2027.

Source: NSIT Investor Day Presentation October 2022

{kind=link}

Given different revenue recognition (gross and net) for different products/services, NSIT correctly guides investors to think about gross profit dollar growth instead of revenue growth. Management is forecasting a low double digit organic gross profit CAGR through 2027.

Source: NSIT Investor Day Presentation October 2022

{kind=link}

OPEX discipline should allow for positive operating leverage from the gross profit growth, enabling ~15% EBITDA CAGR over the next 5 years.

Free cash flow for NSIT is cyclical as the company invests heavily in working capital during periods of hardware growth. However, the counter-cyclicality of NSIT’s cash flow is attractive given that the business generates a substantial amount of cash when revenue growth slows, which can be utilized for share repurchases when the stock is cheap or M&A when targets are cheap.

NSIT’s 2027 forecast is all organic and given the strong free cash flow profile of NSIT, I expect M&A to supplement these LT targets. M&A is an attractive use of capital given that targets often command low multiples given narrow product or company relationships but can fill important gaps in a diversified portfolio such as NSIT’s. Examples of acquisitions that were important strategically include the acquisition of Datalink, which brough NSIT data center implementation expertise, and PCM, which gave NSIT a deeper presence in large corporates (below Fortune 500). Additionally, NSIT usually recognizes significant cost savings as part of any transaction, making the deals highly accretive financially. The balance sheet has ample capacity for M&A given leverage will end the year at ~0.5x net debt/EBITDA.

Management, Comp Structure, Activist Investor

Admittedly, the targets above seem aggressive, so an assessment of leadership and their incentives is important to ensure that shareholders and management are well aligned. Joyce Mullen took over as CEO at the beginning of 2022 after a long career at Dell. Her background in the hardware market is valuable in terms of managing these critical relationships, but arguably is less applicable to the LT objectives of growing cloud and services gross profit. To address this part of the growth algorithm, NSIT hired a new head of North America from Capgemini, a leading consulting organization, who has extensive global experience with software and services.

In terms of compensation, management is well aligned with shareholders. LT performance based RSU’s are tied to ROIC hurdles and relative total shareholder return. ST performance bonuses are tied to cloud and services gross profit growth. NSIT has pushed these RSU’s down to the sales force and tied incentive compensation metrics to services gross profit growth and overall gross margin improvement.

ValueAct, an activist hedge fund, owns a 13% stake in NSIT and has a seat on the board, providing additional shareholder alignment within the company. ValueAct arguably still sees a compelling investment opportunity in NSIT given that the fund was purchasing shares at all-time highs during Q1 ’23.

Valuation

As this portfolio transition materializes, I expect investors will reward the company with a higher multiple. NSIT has historically traded in a range of 8-10x EBITDA compared to CDW, which has traded in a range of 13x-18x. CDW has a structural advantage over NSIT by serving the SMB segment, which allows for better pricing, higher margins and more favorable payment terms. As such, I don’t expect the valuation gap to CDW to close entirely. However, I do believe that NSIT could easily trade in a 10x-12x EBITDA range over the next few years as the quality of the portfolio improves and returns on capital grow. Assuming a 10X EBITDA multiple on 2027 EBITDA $783mm (6.5% margin), yields a price target of $260, or a +16% annualized return from today’s price. A 12x multiple on 2027 EBITDA yields a price target of $322, or a +20% annualized return. EV/EBITDA is the appropriate valuation metric given that NSIT’s balance sheet is under-levered compared to peer CDW, which operates with leverage between 2- 3x, thus boosting EPS. Optimization of NSIT’s capital structure through a combination of M&A/share repurchases provides an opportunity for further EPS growth.

Summary

NSIT is effectively a tax on the secular growth of IT spend combined with increased complexity of IT deployments. The advent of cloud delivery, specifically, has increased IT complexity as this drives a need for decisions around on- premises v. off-premises (or hybrid) and coordination among multiple hardware and software vendors. NSIT’s role as a solutions integrator becomes more important in this dynamic technology landscape as clients increasingly rely on outside IT experts for advice and management of a complex network of vendors. While the secular growth drivers are attractive, the opportunity for NSIT’s stock lies in an improved financial profile as growth from higher margin software and services revenue outpaces hardware revenue growth, leading to structurally higher profit margins and higher returns on capital. Over time, I expect the improved financial profile of NSIT to materialize into a higher multiple for the business.

Important DisclosureThis report is solely for informational purposes and shall not constitute an offer to sell or the solicitation to buy securities. The opinions expressed herein represent the current views of the author(s) at the time of publication and are provided for limited purposes, are not definitive investment advice, and should not be relied on as such. The information presented in this report has been developed internally and/or obtained from sources believed to be reliable; however, Headwaters Capital Management, LLC (the “Firm”) does not guarantee the accuracy, adequacy or completeness of such information. Predictions, opinions, and other information contained in this report are subject to change continually and without notice of any kind and may no longer be true after the date indicated. Any forward-looking statements speak only as of the date they are made, and the firm assumes no duty to and does not undertake to update forward-looking statements. Forward-looking statements are subject to numerous assumptions, risks and uncertainties, which change over time. Actual results could differ materially from those anticipated in forward-looking statements. In particular, target returns are based on the firm’s historical data regarding asset class and strategy. There is no guarantee that targeted returns will be realized or achieved or that an investment strategy will be successful. Investors should keep in mind that the securities markets are volatile and unpredictable. There are no guarantees that the historical performance of an investment, portfolio, or asset class will have a direct correlation with its future performance. The composite performance (“portfolio” or “strategy”) is calculated using the return of a representative portfolio invested in accordance with Headwaters Capital’s fully discretionary accounts under management opened and funded prior to January 1, 2021. The performance data was calculated on a total return basis, including reinvestments of dividends and interest, accrued income, and realized and unrealized gains or losses. The returns also reflect a deduction of advisory fees, commissions charged on transactions, and fees for related services. For further information about the total portfolio’s performance, please contact Headwaters at www.headwaterscapmgmt.com or via phone at (404) 285 -0829 Investing in small- and mid-size companies can involve risks such as less publicly available information than larger companies, volatility, and less liquidity. Investing in a more limited number of issuers and sectors can be subject to greater market fluctuation. Portfolios that concentrate investments in a certain sector may be subject to greater risk than portfolios that invest more broadly, as companies in that sector may share common characteristics and may react similarly to market developments or other factors affecting their values. Headwaters Capital is a registered investment adviser doing business in Texas and Georgia. Registration does not imply a certain level of skill or training. For additional information about Headwaters Capital, including its services and fees, please review the firm’s disclosure statement as set forth in Form ADV and is available at no charge at IAPD - Investment Adviser Public Disclosure - Homepage . Past performance does not guarantee future results. |

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Headwaters Capital - Insight Enterprises: Cheap Valuation, Improving Financials, A Compelling Opportunity