FND - Headwaters Capital Q1 2023 Investor Letter

2023-05-01 16:03:00 ET

Summary

- Headwaters Capital Management is an actively managed, concentrated investment strategy focused on small and mid-capitalization stocks.

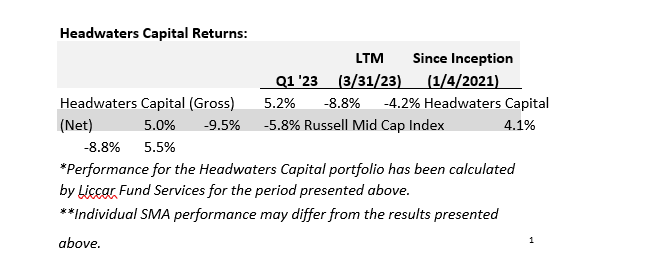

- The Headwaters Capital portfolio gained +5.2% (5.0% net) for the first quarter of 2023 compared to +4.1% return for the Russell Mid Cap Index.

- In terms of the outlook for the market and global economies going forward, the absence of a coordinated business cycle across industries and geographies continues to be the dominant theme.

Dear Investors ,

The Headwaters Capital portfolio gained +5.2% (5.0% net) for the first quarter of 2023 compared to +4.1% return for the Russell Mid Cap Index. A brief discussion of the performance and trading activity during the quarter is presented below.

Headwaters Capital Returns:

{kind=link}

Q1 2023 Performance Discussion

The first quarter of 2023 will be remembered for the fastest bank run in the history of the industry. The rapid collapse of Silicon Valley Bank (SIVBQ) fanned broader concerns for the banking industry as a whole and led to significant share price weakness for banks during the quarter (KRE Regional Bank Index -25% during Q1). While there were many unique issues at SIVB (and Signature Bank/First Republic/Silvergate) that are unlikely to permeate the broader banking industry, the reality is that banks are collectively suffering from declining profitability as balance sheets shrink and funding costs increase. This is all the result of the fastest Fed tightening cycle in history, an exogenous factor outside of a bank's control. Banks are likely to face further profitability headwinds as credit losses normalize at higher levels than have been experienced over the last decade. The absence of banks in the Headwaters portfolio was an active decision that has been discussed previously: the cyclical nature of these businesses can make for great trades, but they don't fit well for a portfolio designed to consistently grow capital. While I certainly didn't foresee a bank run occurring in Q1, the cyclical downturn for banks was inevitable. The lack of bank ownership was the biggest cause of relative outperformance during the first quarter.

In terms of the outlook for the market and global economies going forward, the absence of a coordinated business cycle across industries and geographies continues to be the dominant theme. The divergence in performance across industries should come as no surprise given that COVID had unprecedented impacts on global businesses, which led to uneven recoveries through the pandemic. The ongoing normalization has left some industries booming (service industries, hospitality, leisure) while others are arguably already in a recession (consumer/capital goods, logistics, semiconductors, pockets of industrial, residential housing). This economic bifurcation continues to make the Fed's job difficult as business cycles and inflation vary across industries. Compounding the difficulty are the potential lagged impacts from a rapid monetary tightening cycle that have yet to fully manifest themselves in the economy. These economic crosscurrents have left the market largely rangebound as a whole, but are presenting numerous opportunities at an individual company level.

Q1 '23 Portfolio Review:

Top Contributor: Floor & Décor (FND): The outperformance during the quarter was primarily due to oversold conditions experienced during the fourth quarter. Q4 financial results and the outlook for the full year 2023 were broadly in line with previous expectations and the stock rallied on these better than feared results. While remodeling activity continues to normalize from post-pandemic highs, the long-term outlook for FND remains bright. FND is the category leader in residential flooring, a market that has long-term structural tailwinds thanks to an aging and growing US housing stock. Individual stores generate high returns on capital, enabling the company to internally fund location growth that will ultimately more than double the current store count.

Top Detractor: National Vision Holdings (EYE): National Vision is a low-cost optical retailer operating under the brands America's Best and Eyeglass World. Results have been negatively impacted by a combination of spending normalization following a stimulus fueled boost to sales in 2021/2022 and staffing challenges that are pressuring both sales and margins. Despite these issues, I continue to believe that EYE's position as the low-cost optical retailer will enable the company to gain market share and that sales will eventually normalize given the medical necessity of eyewear. Staffing challenges could prove more durable, especially in the short term, but the company is rolling out remote eye exam capabilities to address these issues. It's also worth noting that the company has experienced private equity ownership twice in the past and I believe any ongoing challenges would likely result in renewed private equity interest.

Trading Activity

Buys (Undisclosed Technology Company): I began buying a position in an undisclosed technology company during the March sell-off. Given that I am still adding to the position, I will discuss the company in more detail in the next letter.

Sells: Insurance Auto Auctions (IAA): IAA was sold during the quarter as the proposed acquisition by Ritchie Brothers Auctioneers closed at the end of March. The acquisition was disappointing as I believe management could have created more shareholder value by either remaining independent or finding a more suitable buyer. The purchase price included a heavy mix of stock and given the unclear strategic rationale for the deal on the RBA side, I elected to sell our shares when the deal was ultimately approved by RBA shareholders.

This letter is shorter than usual as the market is currently presenting more exciting investment opportunities than I can remember in a long time. I'm hopeful that the ongoing volatility will present opportunities to buy a few of these companies in the near term.

As always, if you have any questions about the portfolio or the market, please do not hesitate to contact me.

Christopher Godfrey

Important Disclosure

This report is solely for informational purposes and shall not constitute an offer to sell or the solicitation to buy securities. The opinions expressed herein represent the current views of the author(s) at the time of publication and are provided for limited purposes, are not definitive investment advice, and should not be relied on as such. The information presented in this report has been developed internally and/or obtained from sources believed to be reliable; however, Headwaters Capital Management, LLC (the "Firm") does not guarantee the accuracy, adequacy or completeness of such information.

Predictions, opinions, and other information contained in this report are subject to change continually and without notice of any kind and may no longer be true after the date indicated. Any forward-looking statements speak only as of the date they are made, and the firm assumes no duty to and does not undertake to update forward-looking statements. Forward-looking statements are subject to numerous assumptions, risks and uncertainties, which change over time. Actual results could differ materially from those anticipated in forward-looking statements. In particular, target returns are based on the firm's historical data regarding asset class and strategy. There is no guarantee that targeted returns will be realized or achieved or that an investment strategy will be successful. Investors should keep in mind that the securities markets are volatile and unpredictable. There are no guarantees that the historical performance of an investment, portfolio, or asset class will have a direct correlation with its future performance. The composite performance ("portfolio" or "strategy") is calculated using the return of a representative portfolio invested in accordance with Headwaters Capital's fully discretionary accounts under management opened and funded prior to January 1, 2021. The performance data was calculated on a total return basis, including reinvestments of dividends and interest, accrued income, and realized and unrealized gains or losses. The returns also reflect a deduction of advisory fees, commissions charged on transactions, and fees for related services. For further information about the total portfolio's performance, please contact Headwaters at www.headwaterscapmgmt.comor via phone at (404) 285 -0829

Investing in small- and mid-size companies can involve risks such as less publicly available information than larger companies, volatility, and less liquidity. Investing in a more limited number of issuers and sectors can be subject to greater market fluctuation. Portfolios that concentrate investments in a certain sector may be subject to greater risk than portfolios that invest more broadly, as companies in that sector may share common characteristics and may react similarly to market developments or other factors affecting their values.

Headwaters Capital is a registered investment adviser doing business in Texas and Georgia. Registration does not imply a certain level of skill or training. For additional information about Headwaters Capital, including its services and fees, please review the firm's disclosure statement as set forth in Form ADV and is available at no charge at IAPD - Investment Adviser Public Disclosure - Homepage.

Past performance does not guarantee future results.

Footnotes

[1] The composite performance ("portfolio" or "strategy") is calculated using the return of a representative portfolio invested in accordance with Headwaters Capital's fully discretionary accounts under management opened and funded prior to January 1, 2021. The performance data was calculated on a total return basis, including reinvestments of dividends and interest, accrued income, and realized and unrealized gains or losses. The returns also reflect a deduction of advisory fees, commissions charged on transactions, and fees for related services. For further information about the total portfolio's performance, please contact Headwaters at the email address listed.

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Headwaters Capital Q1 2023 Investor Letter