HSTM - HealthStream: Asset Intensity Not Translating To Profitability Reiterate Hold

2023-08-24 12:15:42 ET

Summary

- HSTM underwent a comprehensive overhaul in 2023, but the stock has decreased by 14% this year.

- Q2 revenues increased by 5%, with a gain of 30% in earnings per share.

- Subscription services contributed 96% of turnover, while revenues from professional services declined by 15%.

- Despite the financials, the firm's economic characteristics languish and aren't conducive to a buy rating.

- Net-net, reiterate hold.

Investment Updates

Following my June publication on HealthStream, Inc. ( HSTM ) the company has pushed further to the downside. It now sells ~11% lower than the previous coverage, but unfortunately, multiples haven't re-rated to a more attractive level. Last time I opined, there were concerns to the company's profitability and efficiency going forward.

The latest investment findings appear to corroborate this view. The posture on HSTM's capital base remains unchanged, and you'll note this is a fairly asset-heavy business with respect to intangibles and acquisitions. As such, you've got ~$340mm in capital at risk rotating just 6.5% trailing return to the business, below long-term market returns on capital. This report will dive into these points in greater detail, with attention to adjacent factors in the investment debate. Net-net, reiterate hold.

Figure 1

{kind=link}

Critical Facts Underpinning Investment Debate

As a reminder, HSTM operates in software-as-a-service ("SaaS") based healthcare applications. Its offerings help healthcare establishments address their ongoing clinical necessities, across development, talent management, training, education, and so forth.

At the end of last year, HSTM reached a pivotal juncture in its One HealthStream model, such that, as of 2023, it underwent a comprehensive overhaul, aligning operations, technology, accounting, and other facets into a unified, enterprise-wide structure. We haven't observed the net benefits of this just yet, with the stock selling ~14% lower this YTD at the time of writing. Presuming the market is a reasonably accurate judge of fair value over this time, this speaks volumes.

1. Q2 insights

HSTM booked Q2 revenues of $69.2mm , showing a 5% increment, on adj. EBITDA of $15.3mm, up 17% YoY. It pulled this to earnings of $0.13 per share, a gain of ~30%. Alas, the operating and earnings leverage is something to consider here.

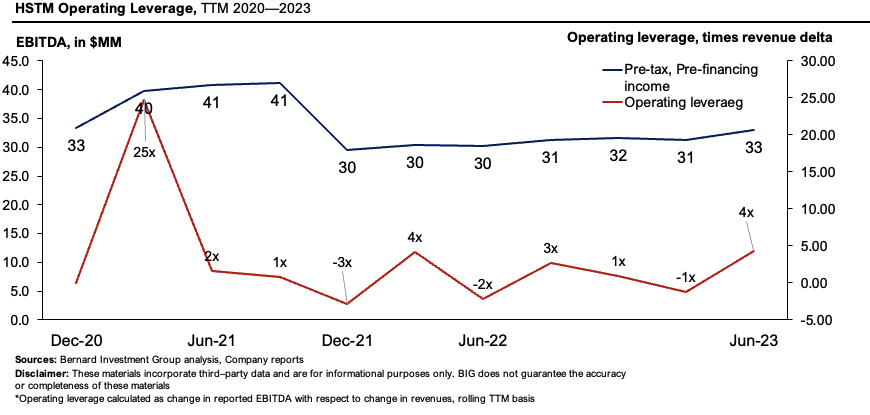

Figure 2 illustrates the turns in reported EBITDA from each turn in sales on a rolling TTM basis. The change in pre-tax income is recorded with respect to the change in revenues each period. It shows the company enjoys a reasonable amount of leverage, both on the upside and downside. It came to ~4x last quarter, or 3.4x using the non-GAAP figures. It suggests that for every new $1 in sales, it booked $4 in pre-tax income. The problem is, the actual prints on EBITDA haven't curled up at the pace you'd expect with this kind of leverage, and this is explained by the mathematics. A change of 4x revenues is less meaningful when sequential sales growth was just 1% and EBITDA grew 3%. Hence, whilst it serves as good data, without the absolute growth percentages, I'd question how much of a bullish point this is for HSTM moving forward.

Figure 2

{kind=link}

Growth was underscored by 400bps of upside in the core business, with the remaining 140bps of growth obtained from its CloudCME and Electronic Education Documentation ("eeds") acquisitions. As to the breakdown, subscription services contributed 96% of turnover and were up 6% YoY to $66.5mm. Conversely, revenues from professional services amounted to $2.7mm, a 15% decline. The firm's YTD revenues are shown below, with similar percentages noted.

Figure 3

{kind=link}

Moving down the P&L, the following takeouts are relevant:

- It pulled the $69mm to gross of 65.9%, ~20bps compression on last year. On inspection, higher royalties and augmented cloud hosting expenses moderately impacted this margin. In a paradox, these factors were fueled by revenue growth, and more so the changes in revenue composition. This could be a risk moving forward and displays a potential loss of leverage on revenue costs.

- Capitalized labour costs increased ~$0.7mm incrementally from Q2 last year as HSTM scaled up investment in its unified platform strategy.

- The firm also gained ~500bps leverage at the G&A line. Nothing special here-typical cost savings in things like lousy debt charges, external recruiting services, professional service fees, and so on.

It left the quarter with cash and marketable securities of $56mm, after a $6.2mm CapEx and $1.5mm dividend payout. This is after $84mm in earnings were retained from investors in the last 12 months. There's no debt on the balance sheet, and you're looking at ~$11.10 in book value per share, reducing to $1.14/share in book value, stripping out $191mm in goodwill and $114mm in intangible assets.

Management guide to FY'23 revenues of $277.5mm-$283mm on adj. EBITDA of $57.5mm-$60.5mm. It looks to allocate ~$29mm to CapEx and could realize ~$25-$30mm in net cash flow on these assumptions.

2. Cash flow analytics

Quarterly operating cash flows were down $2.5mm YoY to ~$26mm, and it recognized $10mm in free cash flow to the firm. But that's treating FCF as a rudimentary calculus as OCF less CapEx, and not representative. More on this a bit later.

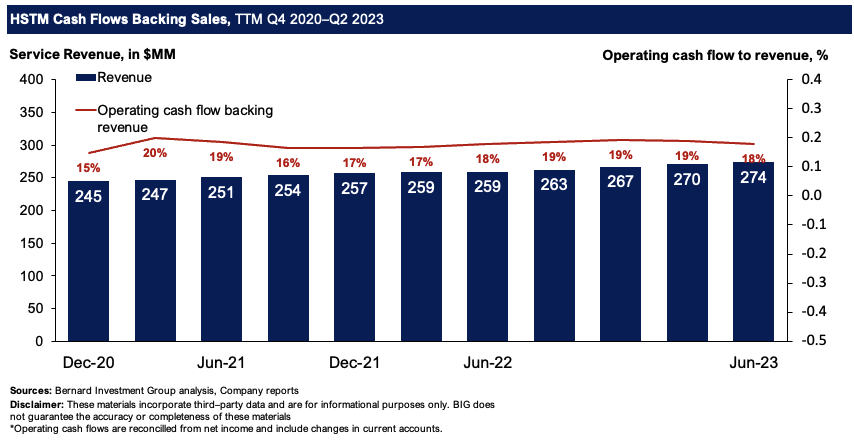

As it stands, HSTM is printing OCF at a historical rate relative to service revenues. Figure 3 tracks the degree of cash flows backing HSTM's turnover on a rolling TTM basis. It remains flat at ~18-20% over the testing period back to 2020. As such, more than 80% of turnover is "non-cash revenues", not abnormal, but not terribly exciting either in terms of conversions from the receivables account.

Figure 4

{kind=link}

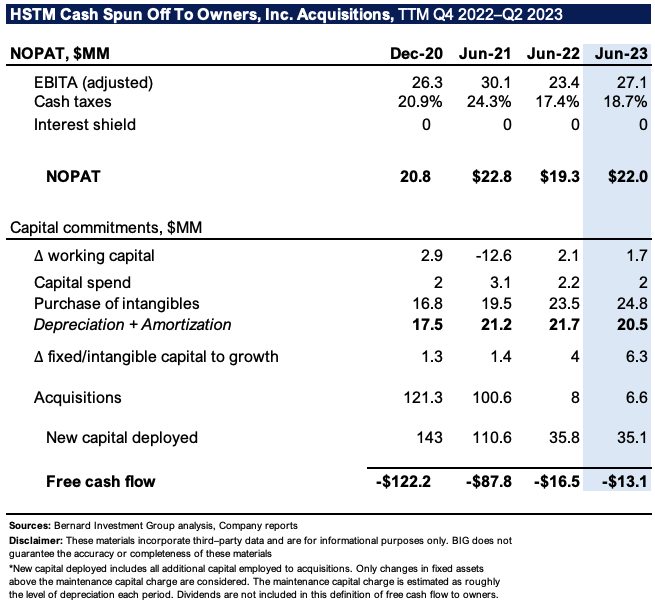

Meanwhile, Figure 4 reconciles the firm's pre-tax earnings to free cash flow attributable to shareholders, and includes all respective uses of capital reinvested back into the business. HSTM is light on fixed assets - instead, it's the reinvestment to intangible capital that is most relevant to the firm. That's why the 'back of the envelope' calculation of FCF less CapEx is less relevant here.

What shows is the firm recognized a free cash outflow when factoring in all acquisitions and purchases of intangibles. Only spending above the maintenance capital charge is considered. This is considered to be roughly equivalent to the depreciation, and particularly amortization expense. These new capital commitments equate to $35mm in the TTM, whereas post-tax earnings grew just $2.7mm. The resulting return on new capital is thus 7.6%. As such, around $340mm produces just $22mm in post-tax earnings, just 6.5% return on the capital at risk. The FCF outflows are therefore being reinvested at sub-par rates of return, and investors can expect to compound capital more efficiently than HSTM can.

Figure 5

{kind=link}

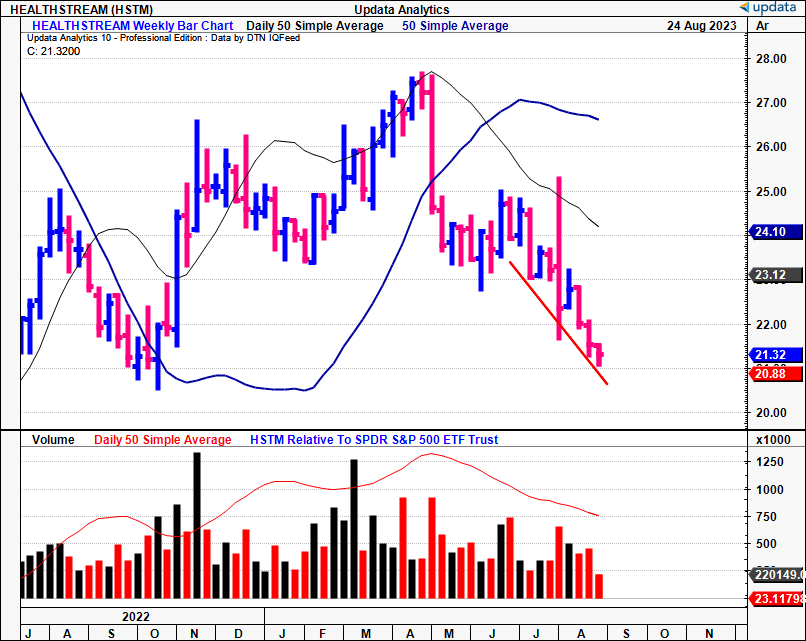

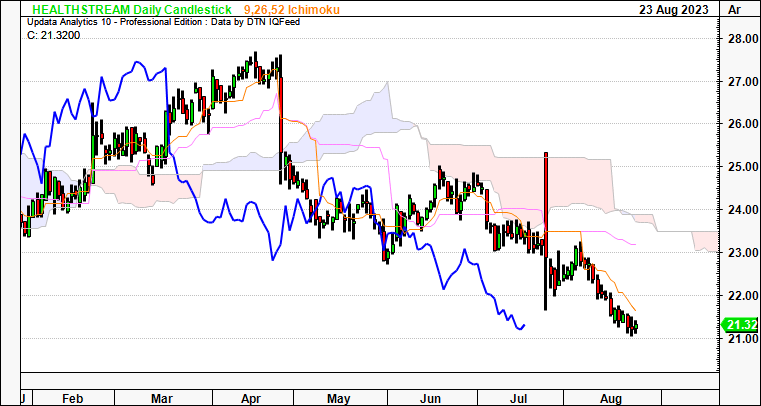

3. Technical take

The stock is weakly supported on technicals as well. The downtrend across 2023 is still well in situ, clearly shown in Figure 5 and Figure 6. On the daily chart below, both the price and lagging lines (in blue) are positioned well below the cloud. This gap has widened in recent months, and you'd need a move to $23.00 by mid-September to suggest a complete reversal in the trend. This corroborates a neutral view.

Figure 6

{kind=link}

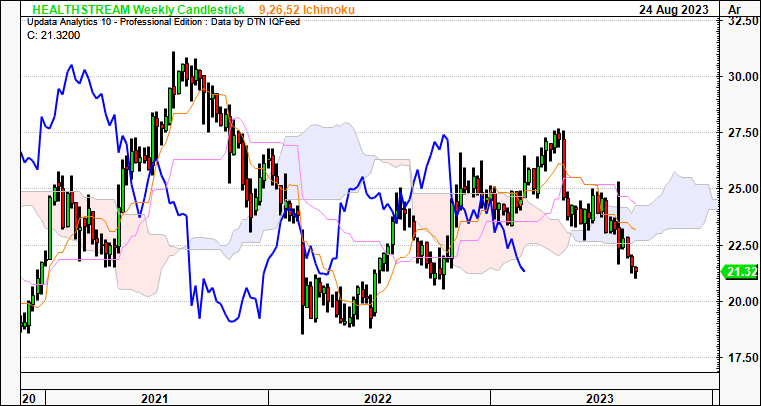

What's most concerning in my eyes is what's seen on the weekly chart. The lagging line has just broken the cloud base in August, after trading through the cloud most of 2023. This is a critical juncture, not a good one either. You'd need a move to $25 on the weekly chart to get back into bullish territory on this setup. Given the weekly chart looks out to the coming months, this implies a neutral view on a long-term time frame.

Figure 7

{kind=link}

Valuation and Conclusion

The talk on valuations also supports a neutral stance in my view. The stock sells at 51x forward earnings but 10x forward EBITDA, with just $1.90 in market value priced for every $1 in net asset value. Given the firm's intangible intensity, I'd expect the market to place a higher premium on its net assets to suggest these are actually valued in high esteem.

Stripping the depreciation + amortization charge out of the mix - which is necessary to understand profitability beyond maintenance spending - HSTM sells at 45x forward EBIT. Not attractive in my eyes. It points to 1) thin profits and 2) poorly valued asset values. The question is, would you pay $45 for every $1 in future earnings, where $340mm in capital invested produces just 6.5% return? In my estimation, this does not constitute an investment-grade company. These findings are supported objectively by the quant system, that also rates HSTM a hold.

Figure 8

{kind=link}

In short, the neutral stance on HSTM remains after rigorously analyzing the latest investment updates. The company's latest numbers do little to sway the debate in my opinion. The consolidation of multiple segments hasn't resulted in additional profitability this year, and you've got a fairly asset-heavy business in HSTM tied up mainly to intangibles, where $11.33/share in capital produces just $0.73/share in earnings after-tax in the last TTM. By all measures, it looks difficult for HSTM to reverse these economic headwinds. Net-net, reiterate hold.

For further details see:

HealthStream: Asset Intensity Not Translating To Profitability, Reiterate Hold