HSTM - HealthStream: Valuations Have Stretched Too Far (Rating Downgrade)

2023-06-14 02:56:32 ET

Summary

- HealthStream's Q1 results show declining operating profit and a lack of earnings growth despite ongoing investment.

- The company's restructuring and focus on its hStream platform present are two factors to keep a close eye on.

- The current valuation of 56x P/E and 48x EBIT is considered too high, leading to a revised hold rating for the stock.

Investment Summary

Following a disappointing set of FY'22 and Q1 FY'23 numbers from HealthStream, Inc (HSTM) I am paring back my rating on the company from buy to hold. I was hoping for more from HSTM, after buying the company at c.7% trailing FCF yield and a series of revenue upsides across 2022. This didn't materialize, and the market, in all its wisdom, has responded accordingly, with a negligent reappraisal to the company's market price.

Here I will discuss my latest findings and run through the reasons behind the revised rating. Net-net, it boils down to factors of profitability and valuation, two factors that simply cannot be ignored by any sophisticated investment cortex. Notably, the company's cost restructuring and pivot to focus on its hStream platform are key points for investors to stay vigilant on moving forward. Revise from buy to hold.

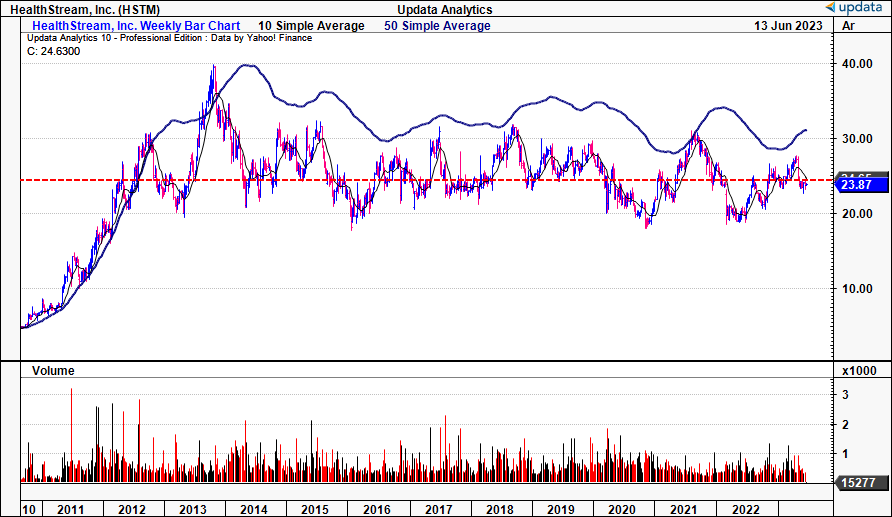

Figure 1. HSTM nil value-add 2012–date

{kind=link}

Q1 breakdown and headwinds

HSTM's Q1 numbers were mixed, with positive and negative aspects to consider. It pulled in c.500bps revenue growth to $45.1mm on core EBITDA of $12.8mm. I was looking for $43-$45mm so this came bang on internal targets. I'll break down the more relevant points for investors below. On face value, d espite achieving a record amount of top-line revenue, several key metrics have declined in Q1 and need further discussion.

The major take outs from the quarter in my eyes were the three following points. For investors, my recommendation is to pay close attention to these factors going ahead:

(1). Concerns over profitability and efficiency

- Revenue is only valuable in my eyes if it is profitable. Investors have deeper issues to consider here. Q1 operating income came in at $2.9mm, a remarkable 28% YoY decline. Earnings were also down 9% to $2.6mm for the quarter. It is looking at $10.4mm earnings at this run-rate, behind last year's $12.1mm. This is a concern as the revenue growth hasn't pulled down to earnings growth for investors in several years now.

- Moreover, the announcement of a $1mm severance expense related to the company's restructuring further underscores challenges in driving earnings growth looking ahead. This is reflected in the fact operating income remained flat since 2013 at c.$12–$15mm annualized. There is all reason to suspect this will continue going forward, based on management's language on the earnings call, and a more thoughtful analysis of the company's fundamentals.

(2). Impacts of acquisitions and product development

- Q1 revenue growth of 5% can be partly attributed to the contributions from two acquisitions made last year: 1) CloudCME, and 2) Eeds. These acquisitions accounted for approximately 1/3rd of the YoY revenue clip.

- However, the increase in product development costs by 12% is noteworthy and again removes any hope of obtaining operating leverage off the revenue growth (for some reason, the company decides to record this net of capitalized labour costs as well, so the 12% runs high). While investments in product development and a single-platform strategy can drive innovation and competitive advantage, there are inherent risks to earnings growth given the concentration risks and potential drags on operating margin in my opinion.

Despite positive talk on growth and the track record from management on the call, the numbers are at odds with this sentiment, as noted in the below record:

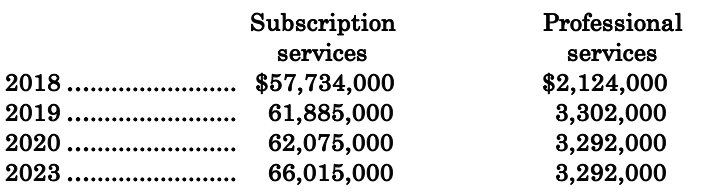

- Table 1. HSTM Q1 divisional revenue growth, 2018–'23

Note: All figures shown in quarterly, Q1 for each period respectively (Data: Author, HSTM SEC Filings)

{kind=link}

Notably, quarterly turnover in both subscription services and professional services has increased by $8.28mm and $1.168mm, respectively. Whilst not tremendous compounding rates, they are growth rates, nonetheless.

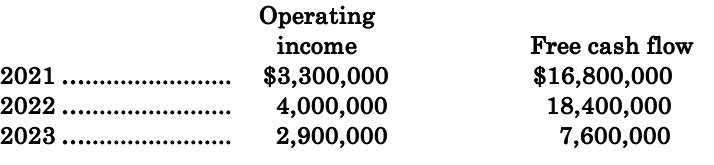

Similar results are missed further down the P&L, however. You'll note the discrepancies in Q1 operating income and free cash flow to the firm from 2021–'23 below, $400,000 and $9.2mm decrease respectively:

- Table 2. HSTM operating income, FCF downsides 2021–2023

Note: All figures shown in quarterly, Q1 for each period respectively (Data: Author, HSTM SEC Filings)

{kind=link}

Restructuring

As a reminder, HSTM is embarking on a cost restructuring announced on its February call . It reports having started this process and a $1mm severance expense booked during the quarter. The restructuring aims to point HSTM toward a single-platform company. To do this, it has embraced its hStream technology platform as the core of its operations. As mentioned earlier, previously, the company operated solely with two distinct business segments:

- Workforce solutions and

- Provider solutions.

However, through the unification of these segments under the "umbrella", let's call it, of the hStream platform, the company has diversified its interests across the healthcare spectrum. I have referred to this holistic approach as the 'one HealthStream' approach, so keep a close eye out for this in the company's updates going forward because it will be critical in my view.

Looking at the positives of the move:

- The strategic shift allows HSTM to leverage the hStream via interoperability among its expanding array of SaaS solutions.

- By doing so, HSTM aims to broaden its offering within healthcare delivery– in other words, penetrate more professional markets.

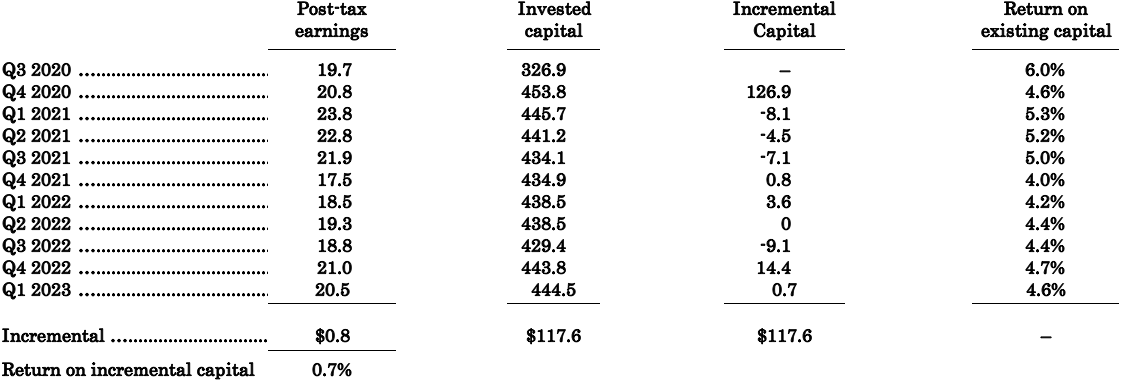

However, there are execution risks involved with the moves, given the company's performance on previous growth investments. This includes HSTM's subscription-based business model, involving contracts averaging 3-5 years, and therefore provides the company with recurring and predictable revenue streams. Looking back to 2020 using rolling TTM periods each quarter, the company has grown post-tax earnings by $0.8mm on a $117mm incremental investment, just 0.7% return on incremental capital. Further, you'll note the return on existing capital has never hovered above 6% at any point in this testing period.

Neither of these is good in my view. I want my companies to put capital to work and generate obscene profits on these investments– more than what I can achieve elsewhere. The long-term market averages are 10–12%, so I'd expect a company to be doing this at minimum to attract investment, let alone rate higher from the market. Without this on the table for HSTM, there is a lack of value creation in my view. Moreover, there is an indication to believe this will continue going ahead.

Management expects $57–60mm in adj. EBITDA for FY'23 and I am in-line with this view, calling for $58mm at the upper end of my assumptions. This would be another $4–$6mm on the FY'22 adj. EBITDA, and thus not much of an indication of growth, and in-line with my neutral view.

Table 3. Return on incremental capital

Data: Author, HSTM SEC Filings

{kind=link}

Valuation and conclusion

If the above points weren't enough of a challenge, investors are trying to sell their HSTM shares at 56x forward earnings. That is far too much of an ask in my view, with the sector at 19x as well. That's also 48x forward EBIT, and there is no justification to pay these multiples in my opinion. Breaking this viewpoint down further, the data so far has shown:

- Declining operating profit on an annualized basis dating back to 2018 at least;

- Lack of earnings growth despite $117mm in incremental investment since FY'20 (TTM basis);

- Sub-standard returns on invested capital that suggest it could be an inefficient use of investors' capital to place their money against HSTM's market value.

These points command a discount to peers if anything in my view, not the opposite. As mentioned, I've uncovered nothing to suggest a 182% premium is worth paying for HSTM at this point, and those tired hands holding the stock will have to accept a far lower bid than 56x P/E to get me interested to nibble.

In that vein, there are several points to suggest HSTM warrants a hold. One, the company's fundamentals are weakening below the top-line. Two, it isn't recycling its profits at rates I could earn elsewhere just riding the benchmark indices. Three, the valuations of 56x P/E and 48x EBIT are borderline offensive considering points one and two. There is consequently more than enough data to support my revised hold rating. Net-net, revise to hold. I look forward to providing further coverage.

For further details see:

HealthStream: Valuations Have Stretched Too Far (Rating Downgrade)