HTLF - Heartland Financial: Prospects Of Sizable Earnings Growth Appear Priced-In

Summary

- Loan growth will likely slow down due to various economic factors.

- A lagged effect of last year's rate hikes will lift earnings this year. However, an increase in the deposit beta will restrict margin growth.

- Operating efficiency is likely to improve due to branch optimization efforts.

- The December 2023 target price suggests a small upside from the current market price. Further, HTLF is offering a low dividend yield.

Earnings of Heartland Financial USA, Inc. ( HTLF ) will most probably surge this year on the back of higher loan balances. Further, the lagged effect of last year's interest rate hikes will boost the margin this year, which will, in turn, support the bottom line. Further, an improvement in operating efficiency following recent branch closures will help earnings. Overall, I’m expecting Heartland Financial to report earnings of $5.44 per share for 2023, up 14% year-over-year. The December 2023 target price suggests a small upside from the current market price. Therefore, I'm adopting a hold rating on Heartland Financial USA, Inc.

Significant Loan Growth Slowdown is Likely

Heartland Financial’s loan growth remained remarkably strong during the fourth quarter of 2022, rising by 4.6%, which took the full-year loan growth to 15.0%. The management mentioned in the conference call that it expects loan growth of $150 million to $200 million for the first quarter of 2022, which translates to a growth of around 1.3% to 1.8%. This is a significant slowdown from the fourth quarter's growth of 4.6%, and quite low compared to previous years. Further, the management expects loan growth of just 6% to 8% for 2023, which is much below the last five-year compounded annual growth rate of 12%.

A slowdown is only natural given the ongoing steep up-rate cycle. Heartland Financial’s network is well diversified with a presence in several states across the West/Southwest and Midwest United States. Further, Heartland’s loan portfolio is concentrated on commercial real estate (“CRE”) and commercial industrial (“C&I”) loans. As a result, broad national economic metrics, like the unemployment rate, are good gauges of credit demand. As shown below, unemployment continues to remain near record lows and is showing no signs of relenting.

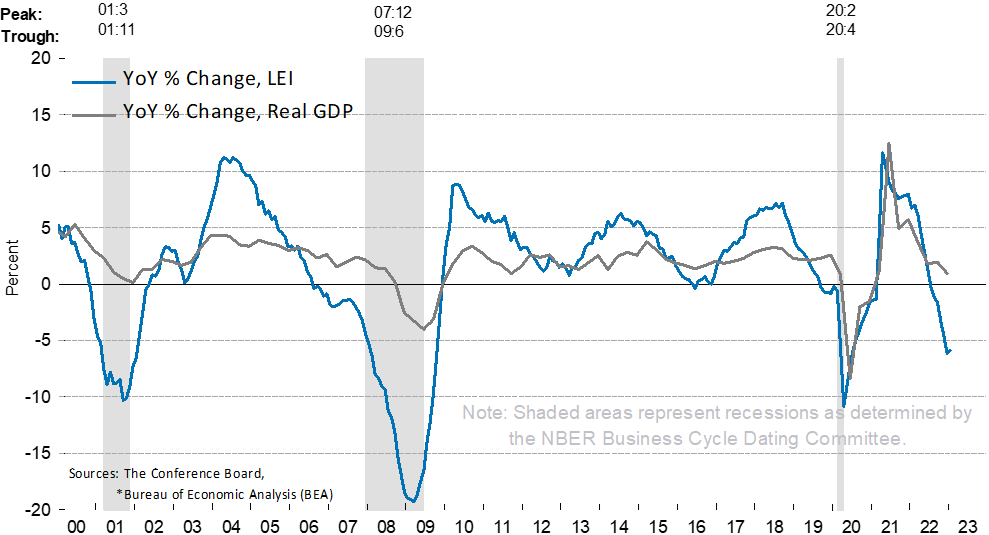

The U.S. leading economic indicator is another appropriate gauge of credit demand. The index’s decline has steepened in the last six months compared to the previous six-month period.

{kind=link}

Considering these factors, I'm expecting the loan growth to decline to 6% in 2023. Further, I'm expecting deposits to grow somewhat in line with loans. The following table shows my balance sheet estimates.

| Financial Position |

| FY18 |

| FY19 |

| FY20 |

| FY21 |

| FY22 |

| FY23E |

| Net interest income |

| 414 |

| 434 |

| 492 |

| 561 |

| 598 |

| 700 |

| Provision for loan losses |

| 24 |

| 17 |

| 67 |

| (18) |

| 15 |

| 24 |

| Non-interest income |

| 109 |

| 116 |

| 120 |

| 129 |

| 128 |

| 115 |

| Non-interest expense |

| 354 |

| 349 |

| 371 |

| 432 |

| 443 |

| 490 |

| Net income - Common Sh. |

| 117 |

| 149 |

| 133 |

| 212 |

| 204 |

| 232 |

| EPS - Diluted ($) |

| 3.52 |

| 4.14 |

| 3.57 |

| 5.00 |

| 4.79 |

| 5.44 |

| Source: SEC Filings, Earnings Releases, Author's Estimates(In USD million unless otherwise specified) |

My estimates are based on certain macroeconomic assumptions that may not come to fruition. Therefore, actual earnings can differ materially from my estimates.

Total Expected Return is Not High Enough for a Buy Rating

Heartland Financial is offering a dividend yield of 2.4% at the current quarterly dividend rate of $0.30 per share. The earnings and dividend estimates suggest a payout ratio of 22% for 2022, which is close to the five-year average of 19%. Therefore, I’m not expecting another increase in the dividend level this year.

I’m using the historical price-to-tangible book (“P/TB”) and price-to-earnings (“P/E”) multiples to value Heartland Financial. The stock has traded at an average P/TB ratio of 1.58 in the past, as shown below.

| FY18 |

| FY19 |

| FY20 |

| FY21 |

| FY22 |

| Average |

| TBVPS - Dec 2023 ($) |

| 28.2 |

| 28.2 |

| 28.2 |

| 28.2 |

| 28.2 |

| Target Price ($) |

| 39.1 |

| 41.9 |

| 44.8 |

| 47.6 |

| 50.4 |

| Market Price ($) |

| 49.7 |

| 49.7 |

| 49.7 |

| 49.7 |

| 49.7 |

| Upside/(Downside) |

| (21.3)% |

| (15.6)% |

| (9.9)% |

| (4.3)% |

| 1.4% |

| Source: Author's Estimates |

The stock has traded at an average P/E ratio of around 11.2x in the past, as shown below.

| FY18 |

| FY19 |

| FY20 |

| FY21 |

| FY22 |

| Average |

| EPS 2023 ($) |

| 5.44 |

| 5.44 |

| 5.44 |

| 5.44 |

| 5.44 |

| Target Price ($) |

| 50.3 |

| 55.7 |

| 61.2 |

| 66.6 |

| 72.0 |

| Market Price ($) |

| 49.7 |

| 49.7 |

| 49.7 |

| 49.7 |

| 49.7 |

| Upside/(Downside) |

| 1.1% |

| 12.1% |

| 23.0% |

| 34.0% |

| 44.9% |

| Source: Author's Estimates |

Equally weighting the target prices from the two valuation methods gives a combined target price of $53.0 , which implies a 6.6% upside from the current market price. Adding the forward dividend yield gives a total expected return of 9.0%. Hence, I’m adopting a hold rating on Heartland Financial USA, Inc. While the earnings prospects are good, the stock price does not appear to be attractive. I would only consider investing in Heartland Financial if its price dipped by more than 5% from the current level.

For further details see:

Heartland Financial: Prospects Of Sizable Earnings Growth Appear Priced-In