HTLF - Heartland Financial USA: Erratic Heartbeat In Q2 Earnings

2023-08-02 12:00:00 ET

Summary

- Heartland Financial USA, Inc. reported Q2 earnings that missed expectations, but maintains a strong financial position.

- The company is focused on expanding its loan and deposit bases to strengthen its financial position.

- The stock's medium-term performance has lagged behind the broader market but it offers a strong dividend yield.

Thesis

This article delves into Heartland Financial USA, Inc.'s (HTLF) recent Q2 earnings that showcased a GAAP EPS of $1.11 that missed by $0.02, and revenue of $179.6M that missed by $2.55M. Despite some headwinds such as rising credit losses and operational expenses, HTLF maintains a relatively strong financial position, supported by a high liquidity profile, a healthy loan-to-deposit ratio, and a low debt structure. However, the medium-term stock performance of HTLF has lagged behind the broader market, which, coupled with certain risk factors, tempers its appeal.

Company Overview

Heartland Financial USA, Inc., a Denver-based, diversified multi-bank holding company, has a broad service spectrum that spans commercial, small business, and consumer banking. The firm presents a broad suite of deposit products and loans tailored to varied sectors, alongside a venture into credit cards. Their footprint extends into the digital realm with a host of services including online banking, fraud prevention measures, and wealth management. Heartland Financial further diversifies with an offering in the investment world, and has branched into consumer finance, insurance, and property management. Founded in 1981, the company extends its presence beyond its Colorado base, reaching from the Midwest to the West Coast.

Heartland Financial USA's Q2 Earnings Highlights

Heartland Financial USA unveiled its earnings per share ((EPS)) that came in at $1.11 and reported an expansion of its loan portfolio, which experienced a noteworthy increase of over $220 million.

An examination of HTLF's balance sheet reveals a concerted effort to reduce debt, as seen by the contraction of total borrowings by $48 million. As long as it's maintained, this proactive reduction in indebtedness will contribute to the overall health of HTLF's financial position moving forward. Notably, the firm's liquidity profile appears strong, projecting a sizeable cash flow of $1.3 billion over the coming 12 months, expected from its securities portfolio.

In addition, HTLF is backed by low outstanding borrowings and is buttressed by an impressive $3.3 billion of available capacity at the Federal Reserve and Federal Home Loan Bank. This balance of lower debt and highly accessible funds should add a solid buffer to HTLF's financial stability.

Heartland Financial's customer deposit base presents a picture of relative strength and diversity, with over two-thirds of balances either secured or collateralized. The relatively low loan-to-deposit ratio signals a fairly sound liquidity position. A comforting note is HTLF's holding company's cash reserve of $268 million, amply covering any impending annual interest and dividend payments.

HTLF is underpinned by a capital structure boasting a common equity Tier-1 ratio of slightly over 11.3% and a total risk-based capital approaching 15%. Notably, even after adjusting for unrealized investment losses, these ratios remain commendably above the level considered as well-capitalized, bolstering the company's fiscal health. The rise in non-interest income, a component of the bank's revenue stream, is another positive indicator this quarter.

Looking ahead, HTLF has set its sights on further expanding its loan and deposit bases. This growth strategy, if successfully implemented, could potentially reduce reliance on wholesale deposits, further strengthening its financial position.

Performance

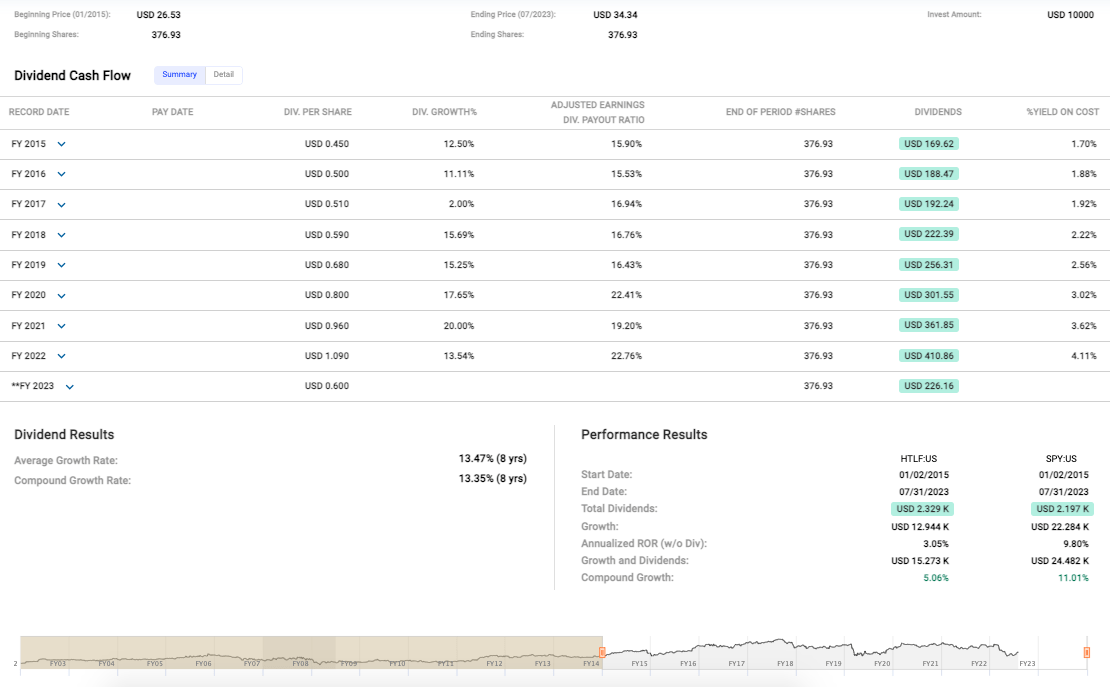

Drawing attention to the stock's medium-term price growth (see data below) from 2015 to 2023, we're looking at an increase from $26.53 to $34.34, representing a growth of around 29% over 8.5 years. That's an annualized rate of return of 3.05% without taking dividends into account. Not spectacular, in my view, especially when you consider the S&P 500 Index (SP500), which has returned 9.80% annually in the same period. This comparison paints a less than rosy picture for HTLF in terms of price appreciation.

{kind=link}

However, don't discount the dividends. When you factor in dividends, the picture improves a bit for HTLF. The total dividends received (on an initial $10k investment) amounted to $2.329K and, when combined with growth, led to a total of $15.273K. This bumps up the annualized rate of return to 5.06%.

Nevertheless, the broader market still outpaced HTLF, even when we consider both growth and dividends, with an 11.01% compound growth. Therefore, if you're an income-focused investor, HTLF might appeal to you due to its strong dividend history.

Valuation

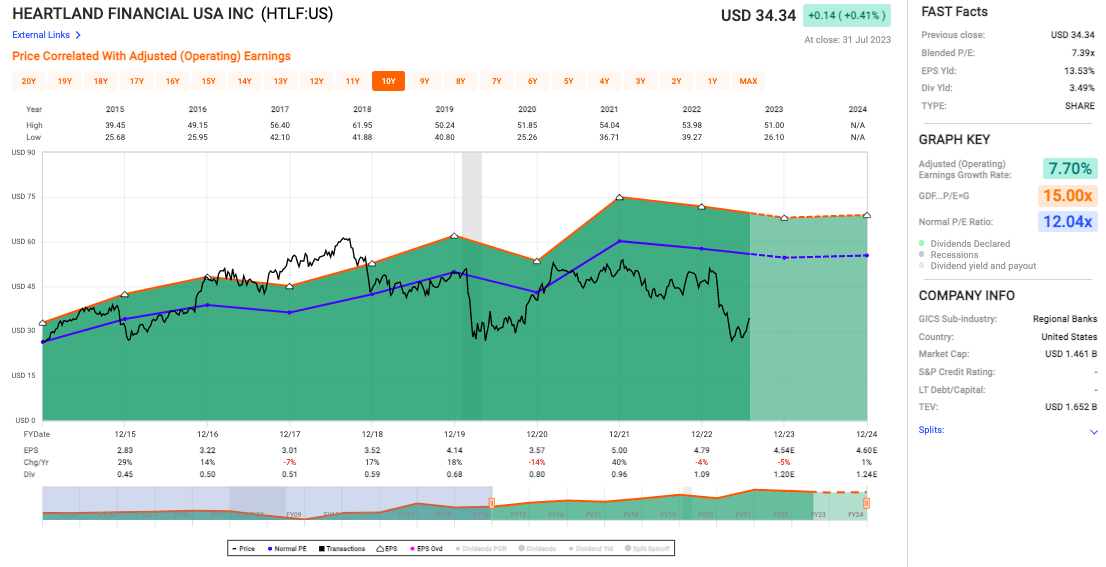

The blended P/E ratio of 7.39x is also of particular interest (see chart below). This is well below the industry standard P/E ratio of 15.00x, and it's even below Heartland Financial's own historical normal P/E of 12.04x. In my book, that potentially marks the stock as undervalued. It indicates that the market might not be fully appreciating the company's earnings potential.

{kind=link}

The EPS yield of 13.53% is not to be taken lightly either. It's impressive, underscoring Heartland's profitability. The high EPS yield signals that the company is generating a significant amount of profit relative to its stock price, another sign that the stock could be undervalued.

A dividend yield of 3.49% rounds out the picture of a company that is rewarding its shareholders - an aspect of Heartland Financial that should particularly appeal to income-focused investors.

Lastly, let's talk about the adjusted operating earnings growth rate of 7.7%. This is a modest growth rate but it is growth nonetheless.

Risks & Headwinds

Heartland's difficulties are underscored by an augmented provision for credit losses by $2.3 million over the last quarter, a development that tends to forecast probable default hazards. In addition, the bank has seen an upswing in net charge-offs, a metric that implies an increase in debts that are unlikely to be recovered.

The complications extend to Heartland's investment portfolio as well, which has experienced a contraction of close to $300 million. This contraction is noteworthy as it could potentially impede the bank's prospective earnings generated from these assets. A deeper dive reveals an exacerbation of the unrealized loss on the available-for-sale ((AFS)) portfolio within this quarter, which might signal unfavorable market conditions or perhaps, a subpar performance of the underlying assets.

An essential gauge for banks, net interest income, unfortunately, did not escape the downward trend. It experienced a decline to the tune of $5.1 million in comparison with the preceding quarter. This downturn can be traced back to two primary causes: premium write-offs associated with payoffs from purchased Small Business Administration ((SBA)) loans and a strategic shift in deposit balances, from the less expensive non-maturity deposits to the costlier time deposits.

Lastly, the operational expenditure of the company exceeded its anticipated projection, fueled by a surge in advertising costs linked to deposits, and a significant rise in professional fees. As Heartland Financial plans its trajectory for the future, it has factored in restructuring costs within the range of $2.5 million to $3 million for each of the next two quarters. Such an estimate points towards an unavoidable impact on future profitability, even as the bank strives to remain agile in the face of these challenges.

Final Takeaway

Based on the data, I'd rate Heartland Financial USA a "hold." Although it has a solid balance sheet, promising earnings potential, and an undervalued status, the stock's medium-term growth rate has underperformed the broader market. Furthermore, the company faces various headwinds including increased credit losses, a shrinking investment portfolio, and operational expenses, which could potentially undermine future profitability and is most likely the reasons behind the market taking down its share price by -4.63% at the time of this analysis. Despite this, the strong dividend yield might still be appealing to income-focused investors, warranting a hold rating for Heartland Financial USA, Inc.

For further details see:

Heartland Financial USA: Erratic Heartbeat In Q2 Earnings