HTLF - Heartland Financial USA Stock: An Interesting Prospect For Bargain Buyers

2023-10-18 12:23:20 ET

Summary

- Heartland Financial USA, Inc. is a value-oriented investment opportunity in the banking sector.

- Shares look cheap and the company is making progress in some important areas.

- Some issues still remain, but Heartland Financial USA shares do warrant a modest degree of optimism.

Although the banking sector has not been particularly popular this year, it does currently offer some of the more interesting prospects. This is especially true if you are a value-oriented investor like myself. One firm that I have come across that I believe investors should be paying attention to is Heartland Financial USA, Inc. ( HTLF ). While there are some negatives about the bank, such as a modest decline in deposits recently and uninsured deposit exposure that is higher than I would like to see, shares are cheap and the overall picture for the institution is far from bad.

All things considered, I would rate the company a soft "buy" at this time. But that view could become further cemented if, in the company's next earnings release, we see some improvements along key areas.

An interesting bank for bargain buyers

For those not familiar with Heartland Financial USA and its operations , it is set up as a bank holding company that engages in a wide variety of activities. Prior to this year, the company actually had multiple bank charters under its belt. But as of February of this year, they have all been consolidated under the HTLF Bank charter. Just like really any bank out there, Heartland Financial USA originates loans, not only for consumers, but also for businesses. Examples include commercial real estate loans, agricultural loans, small business loans, residential real estate mortgages, and more. The company also engages in traditional consumer banking activities like accepting deposits, issuing CDs, helping customers with IRAs, and more. The company even engages in brokerage services, including those centered around the issuance of fixed rate annuity products.

Although not a major part of what Heartland Financial USA does, it also helps customers with wealth management and retirement plan services. As of the end of its 2022 fiscal year, it had over $3.6 billion in trust assets under management, with different plans including 401(k)s and 403(b)s. The company has 117 different branches. But it wasn't always this large. At the end of 2020, the bank had 142 branches. But management has been focused on trying to cut costs, and it has even gone so far as to express an interest in decreasing branch count further. Of course, the company can only shrink so far without hurting itself from a geographic exposure perspective. All of its branches are currently split between the Southwest, the West, and the Midwest.

{kind=link}

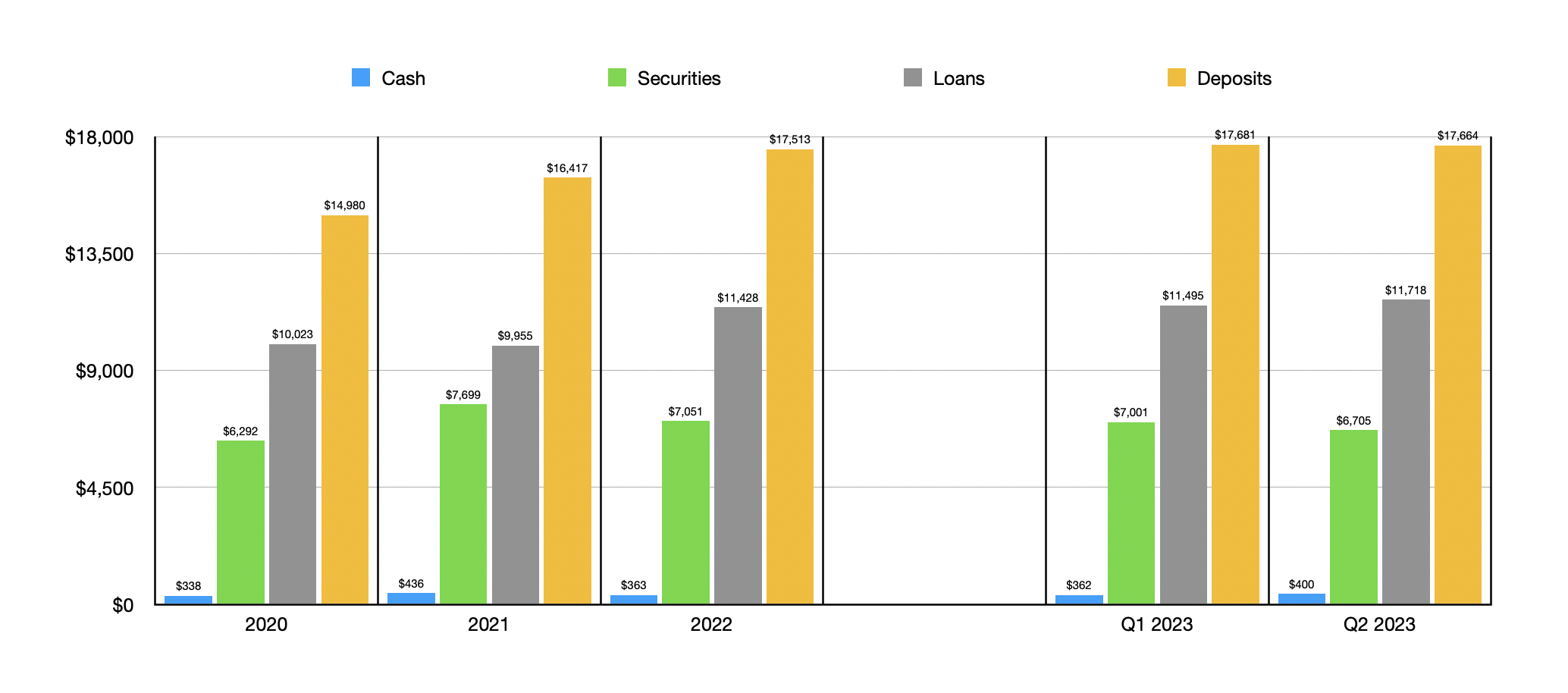

In recent years, even in spite of the decline in branch count, management has done well to grow the bank's assets. The value of loans grew from $10.02 billion in 2020 to $11.42 billion in 2022. The firm saw further growth in loans from that point to the end of the second quarter of this year, when they totaled $11.72 billion. I do know that investors are generally worried about exposure to office properties.

The good news here is that only 3.5% of all of its loans are dedicated to this space. As the value of loans has increased, so too has the value of securities on its books. Securities jumped from $6.29 billion in 2020 to $7.05 billion in 2022. We have seen a bit of a decrease since then, with security values declining to $6.71 billion at the end of the most recent quarter . Meanwhile, the value of cash on the company's books has remained fairly consistent, hovering between a low point of $337.9 million and a high point of $435.6 million. As of the end of the most recent quarter, the bank had $400.2 million in cash and cash equivalents.

{kind=link}

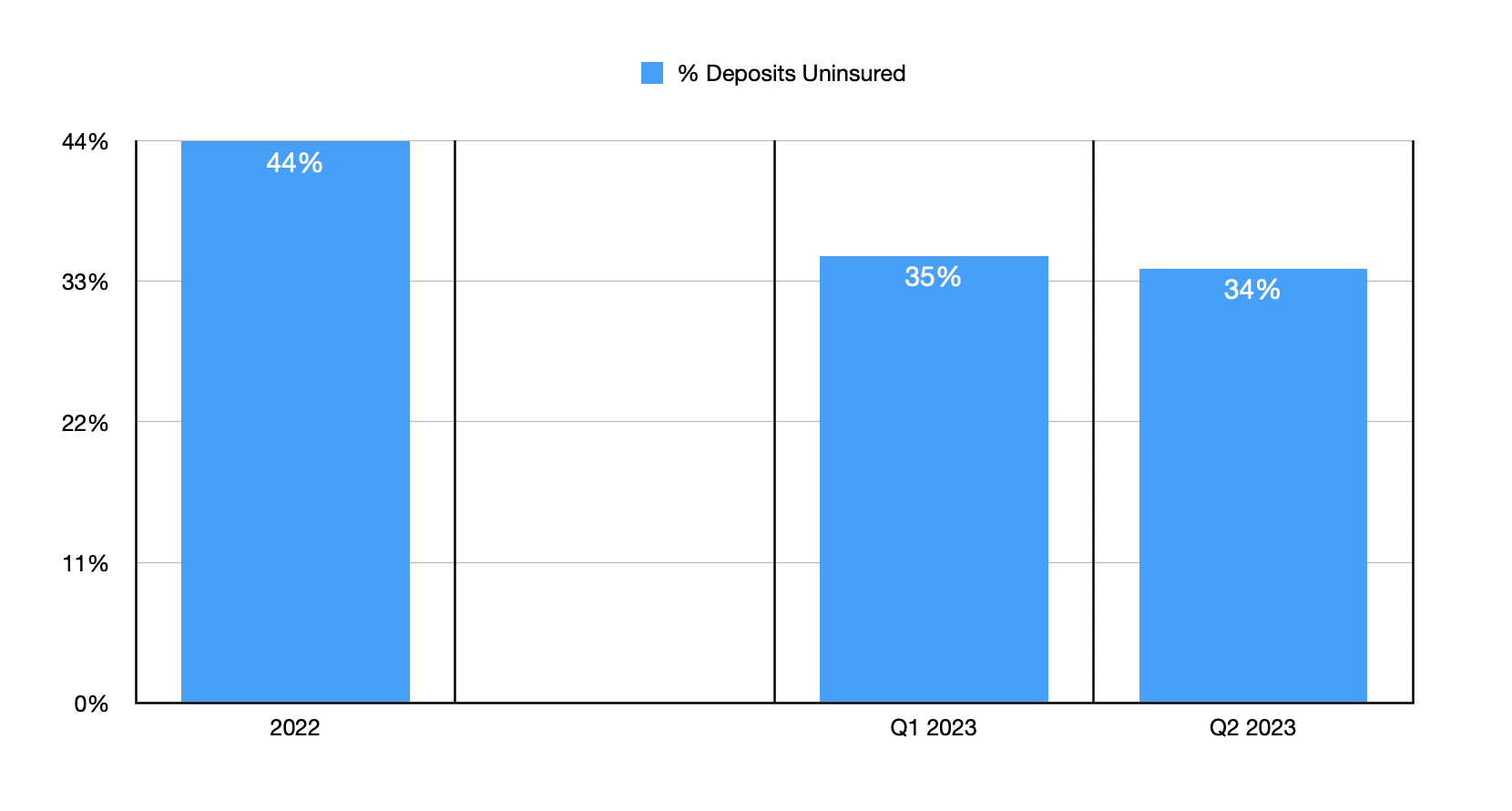

This increase in overall assets has only been made possible by growth in deposits. From 2020 through 2022, deposits at the bank expanded from $14.98 billion to $17.51 billion. We saw a continued increase to $17.68 billion during the first quarter of this year. But in the second quarter, likely in response to the banking crisis that occurred earlier in the year, deposits pulled back slightly to $17.66 billion. Although this is not great to see, it is a rounding error in the grand scheme of things. And more importantly, the company can at least say that it improved the exposure that it has to uninsured deposits . At the end of 2022, 44% of its deposits were uninsured. This number dropped to 35% in the first quarter before dipping further to 34% in the second quarter. I am quite adamant in targeting banks that have uninsured deposit exposure that is 30% or lower. But the overall trend here is positive.

{kind=link}

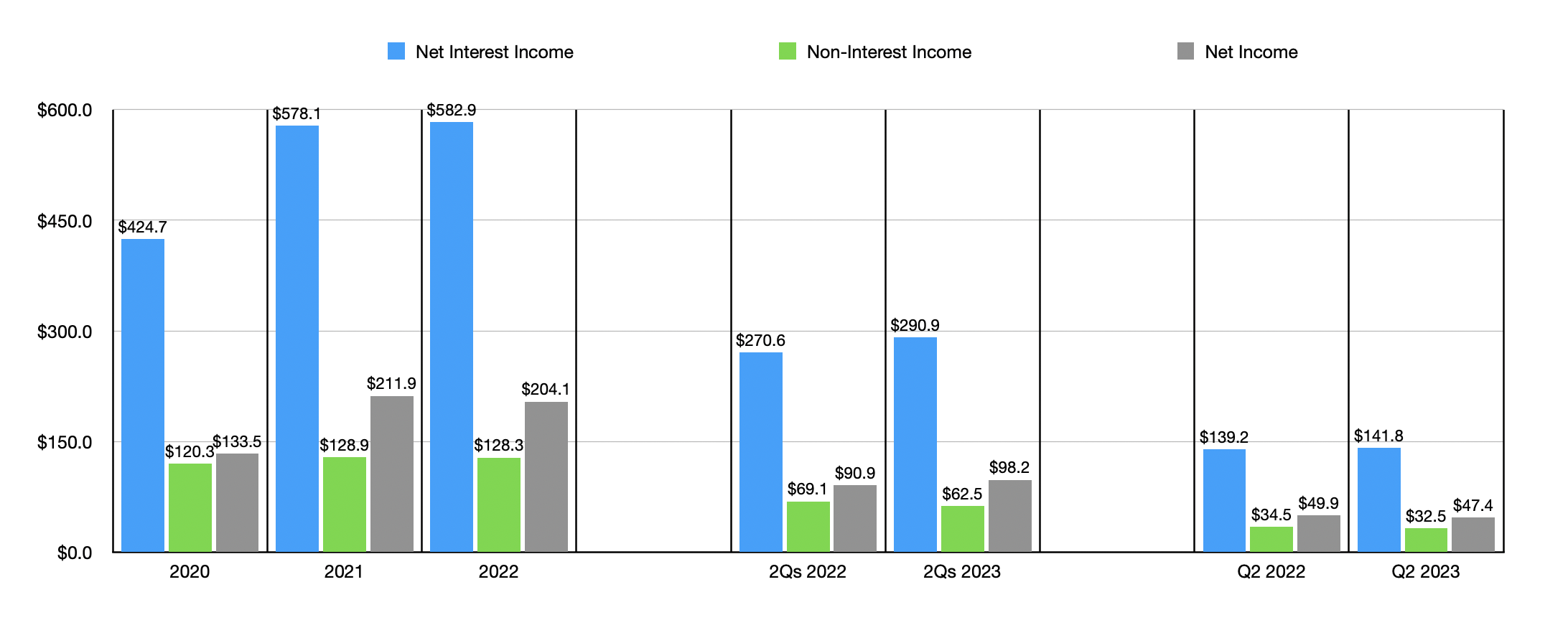

Despite the consistent increase in deposits and loans, financial performance of the bank has been somewhat mixed. Net interest income did grow from $424.7 million in 2020 to $582.9 million in 2022. We saw a modest increase in non-interest income, while net interest income popped from $133.5 million to $204.1 million. For the current fiscal year, the picture is generally positive. Net interest income in the first half of the year totaled $290.9 million. That's up nicely from the $270.6 million reported one year earlier. Even though non-interest income shrank from $69.1 million to $62.5 million, overall net income grew from $90.9 million to $98.2 million.

{kind=link}

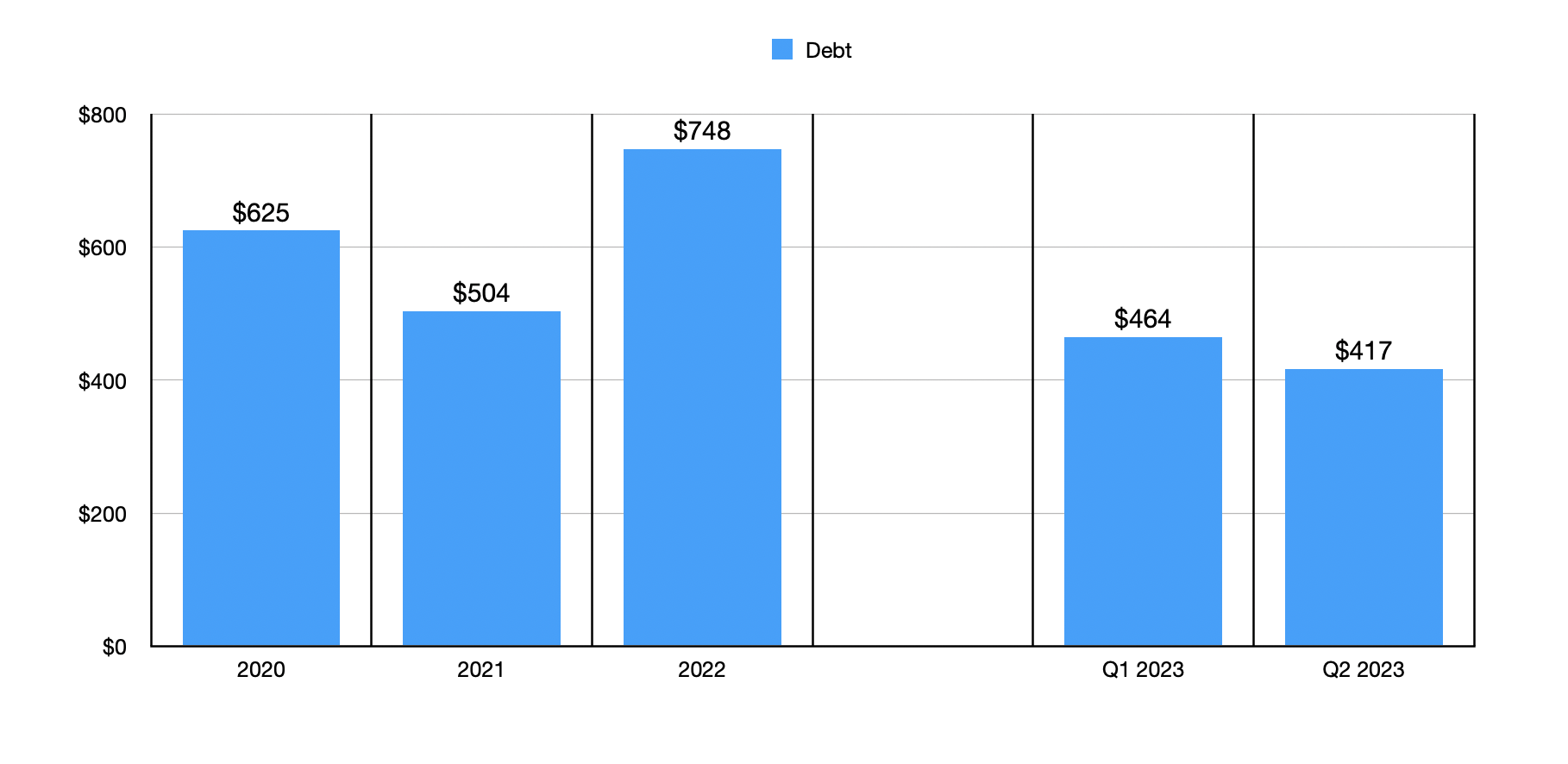

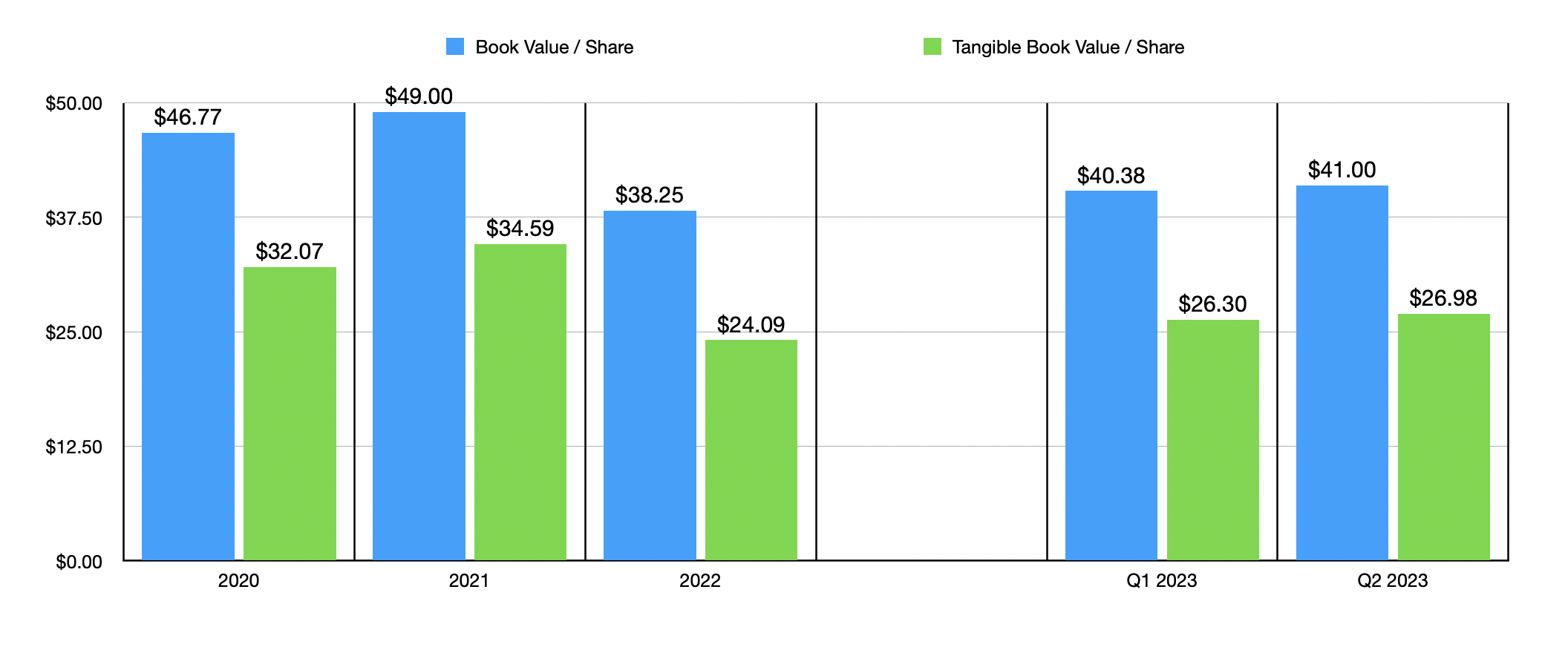

There are a couple of other good things that the bank has going for it. For instance, at the end of last year, the bank had $747.9 million in debt on its books. As of the end of the second quarter, that number had fallen to $416.8 million. Book value per share grew from $38.25 to $41, while tangible book value increased from $24.09 to $26.98. At present, this all translates to the company trading at a 28.3% discount to book value and at only a 9% premium to tangible book value. Meanwhile, using financial performance from 2022, the institution is trading at a price to earnings multiple of only 6.1. This is comfortably below the average that I have seen of about 10.4.

{kind=link}

Takeaway

As far as banks go, Heartland Financial USA, Inc. looks to be a really interesting prospect. I don't like the uninsured deposit exposure still, and I would have preferred for deposits to actually increase. But outside of that, I really like what I I'm looking at. Shares look cheap at this point in time, and the overall trajectory for the bank has been positive, not only in prior years, but also this year as well. Due to this combination of factors, I've decided to rate the bank a soft "buy" at this time, which is a rating reflective of my belief that shares should outperform the broader market, even if only marginally so, for the foreseeable future.

For further details see:

Heartland Financial USA Stock: An Interesting Prospect For Bargain Buyers