HEI - HEICO Corporation: Attractive Business Model With Attractive Financial Profile

2023-10-19 10:43:24 ET

Summary

- HEI has a strong value proposition and business model, with potential for attractive growth and expanding margins.

- The company operates in the aerospace industry, serving a global client base and generating recurring revenue from commercial aerospace aftermarket and defense subcomponents.

- HEI's unique position in the market, pricing power, and flexible cost structure contribute to its ability to negotiate on price and maintain profitability.

Summary

T his post is to provide my thoughts on the HEICO Corporation ( HEI ) business and stock. I am recommending a buy rating for HEI as I believe the business has a strong value proposition and business model that enable it to continue growing attractively with expanding margins. The valuation has also tapered down to its historical average of 22x forward EBITDA (from 30+x), making the risk/reward much more appealing. Based on my long-term DCF model, I believe there is 22% upside potential.

Business

HEI operates by developing, producing, and marketing aerospace goods and services via its affiliated companies. The firm serves a global client base, comprising airlines, defense contractors, and military agencies. The HEI business model is attractive as the majority of revenue is generated in commercial aerospace AM (aftermarket) and in defense subcomponents, both of which generate recurring revenue that provides high visibility and also has high margins. Its differentiated commercial aerospace AM model gives it access to an underpenetrated large TAM. It owns the distributors and MRO (maintenance, repair, and operations) shops to sell parts through, while leveraging existing customer relationships to offer discounted AM products.

Investment thesis

There are few key reasons for my bullish view on HEI’s business.

Firstly, HEI’s Parts Manufacturer Approval [PMA] business model is a design and production approval issued by the FAA for the manufacture and sale of modification and replacement parts for aircraft. PMA approval is required for suppliers that manufacture the original equipment, but HEI for the most part targets third party PMA. This puts HEI in a unique position as it provides HEI access to a large TAM for AM revenue that isn't restricted by products that are developed by OEMs. The value proposition of HEI's PMA business comes from the large discount HEI offers on the products (as much as 50% relative to OEM). The HEI discount model circumvents the traditional razor and blade aftermarket business models by introducing low-priced competition to what is often a sole-sourced OE product. The fact is, researching, developing, certifying, and manufacturing the parts HEI sells is difficult and costly, which HEI is very efficient at doing. As such, it is not a business that new entrants can simply replicate. Consequently, airlines love HEI 3rd party PMA business as it provides a unique value proposition, giving airlines access to significant discounts on OE-made aftermarket parts. HEI has multiple growth levers to pull for its PMA business, a large part from cross-sell potential; usually, HEI PMAs is part of the commitment of an airline, which shows that someone is willing to adopt them. HEI can then cross-sell to its existing base of customers. As HEI owns the distribution and repair business (that it sells its PMA parts through), this gives it a diverse stream of revenue channels (other than just selling standalone replacement parts) and allows it to build a stronger relationship with airlines.

Secondly, HEI benefits from passenger air travel as a long-term structural grower ( growth 2x global GDP ), since more travels = more planes, which directly impacts the growth of aftermarket services. The majority of HEI's aftermarket exposure is non-discretionary, which means they are essential products that, as long as planes fly and parts eventually wear and tear, they will need HEI's product.

Thirdly, it’s the pricing power that HEI has. HEI's products are diversified around the globe, often with small niche components, as evident from the fact that less than 10% of sales volume is parts over $5,000 ( 2Q21 earnings call ). This suggests that even with price hikes, customers will still accept it as the parts are crucial. Viewed from another perspective, HEI's products are often found in landing gear, engines, wings, and larger components like the axis power unit. These parts are unsafe to work on even if one screw is missing; hence, HEI's product can be known as mission-critical, which further empowers its ability to negotiate on price.

Lastly, the HEI business model has an attractive financial profile, both in the P&L and balance sheet. HEI has consistently grown both its GM and EBTIDA margins historically, which, based on my calculation, demonstrated ~30% incremental margins historically. Given no major change in the business model, HEI should continue to expand margins as it scales. A major positive that I like about HEI is the high mix of flexible cost structures. For example, during COVID, HEI faced -44% organic growth, but its EBIT margin only dived to 11%. The nature of its cost structure prevents an asymmetrical impact on the bottom line. As for its balance sheet, HEI has ample dry powder sitting on its B/S that, if management decides to lever up (current <1x EBITDA net debt), it could easily generate >1bn of capital for M&As. If HEI were to lever its balance sheet up to TransDigm level (~5x EBITDA), HEI would have a net debt position of $3.5 billion and an additional $2.9 billion in cash. On the M&A front, the M&A pipeline seems to be healthy despite the weak macro environment. Since the start of last year, HEI has made 11 acquisitions. Given that the cost of capital is now higher, which means the valuations of targets are likely to be lower, I see HEI in a good negotiating position to continue its M&A strategy to drive topline and margin growth. Notably, the HEI M&A strategy to acquire a majority stake while retaining the original owner with meaningful equity ownership is a smart move as it aligns owner incentives and drives long-term quality (the owner knows the business the best).

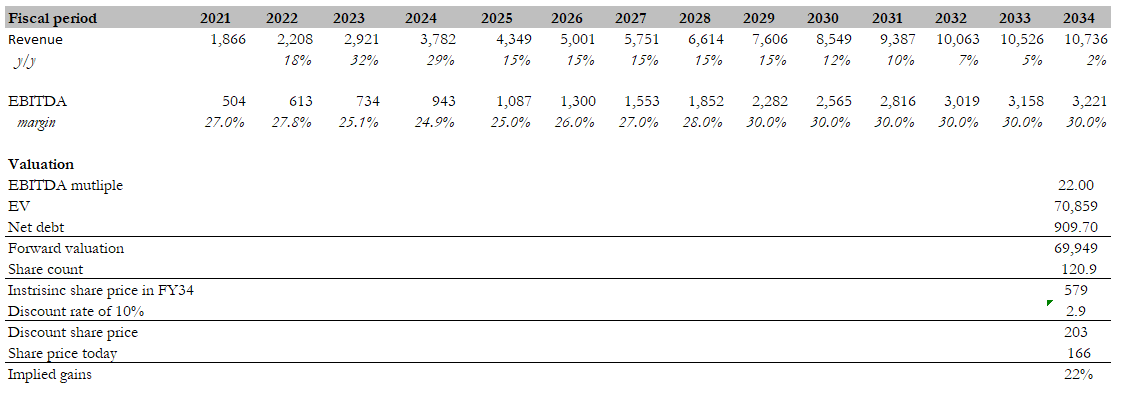

Valuation

{kind=link}

Own calculation

HEI's strong value proposition to customers and execution can be seen in its historical performance, where it has consistently generated positive revenue growth for the past 10 years (except for COVID, which was an outlier), growing revenue from $1 billion in FY13 to $2.2 billion in FY22. Even in the last 3 quarters, revenue has been very strong at more than 20%. More notably, margins across all 4 levels (gross, EBITDA, EBIT, and net) have improved significantly by ~300bps, 300bps, 400bps, and 400bps, respectively. Because of the nature of HEI’s business model, it has strong visibility into its cash flow movements; hence, the business has plenty of room to flex its balance sheet for growth. As of 3Q23, HEI had $500 million in net debt, or less than 1x EBITDA.

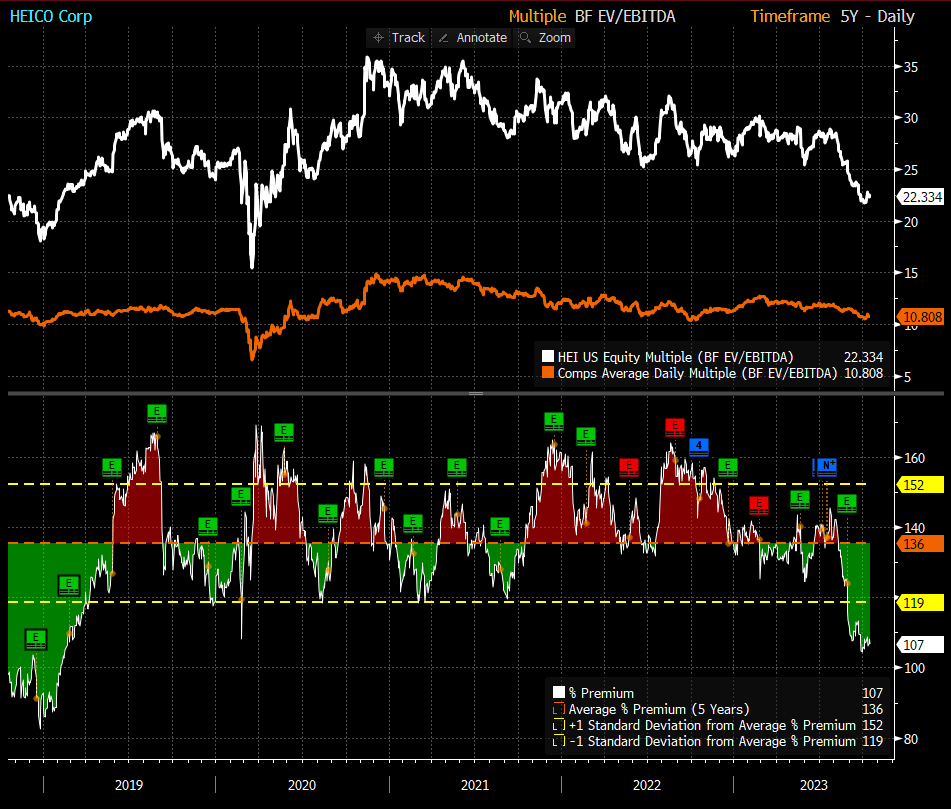

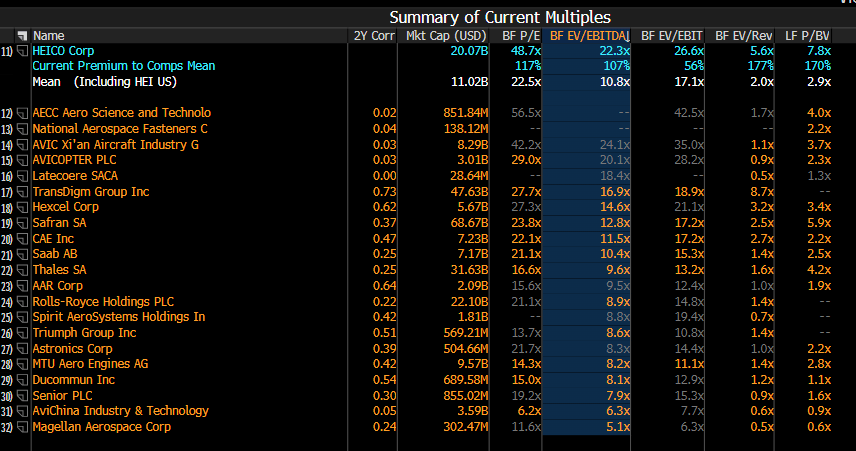

I believe the fair value for HEI based on my DCF model is $203. My model assumptions follow consensus estimates for FY23 and FY24, followed by my estimate that HEI should continue to compound growth at 15% a year, in line with its historical growth rates, followed by a decline in inflation rates in the terminal year (FY34). Based on HEI historical margin performance and its high incremental margins, I believe margin should continue to expand in the growth years (FY23 to FY29), followed by a matured EBITDA margin profile of 30% through FY34. HEI has consistently traded at a premium to peers over the years, which I believe is due to its consistent growth profile, expanding margins, and low debt nature (0.75x net debt to ebitda vs. peers’ average of 2x). I believe HEI will continue to trade at a premium, given my expectations.

{kind=link}

Bloomberg

{kind=link}

Bloomberg

Risk

In the event of any slowdown in the penetration rate of PMA adoption and penetration of the total aftermarket TAM, it would impact HEI's ability to grow revenue at attractive margins, as such, pressure valuation. M&A is a key piece of the puzzle for HEI to compound cash flow; if the M&A TAM shrinks or acquired businesses underperform, it would impact the HEI business model. One downside that investors may find is the valuation spread between TDG and HEI, where TDG may be more favored due to its pricing power and lower valuation.

Conclusion

HEI presents a compelling investment opportunity. Its business model, centered on PMA, positions it uniquely in the market, offering access to a sizable aftermarket revenue pool. This approach, marked by substantial discounts compared to OEMs, sets HEI apart and is challenging to replicate. Additionally, the company benefits from the long-term growth of passenger air travel, ensuring consistent demand for its products. HEI's pricing power is another strength, as its mission-critical components allow for negotiation on price, while its flexible cost structure insulates its profitability from external shocks. A robust financial profile and ample room for leveraging its balance sheet for growth make HEI an attractive proposition. With a healthy M&A pipeline and a history of acquisitions that align owner incentives, the company is well-positioned to drive further growth.

For further details see:

HEICO Corporation: Attractive Business Model With Attractive Financial Profile