HEI - HEICO Corporation: Great Performance But A Downgrade Might Be On The Horizon

2023-08-30 11:43:08 ET

Summary

- HEICO Corporation's financial results for Q3 of fiscal year 2023 exceeded expectations, with revenue increasing by 26.9%.

- The company's Flight Support Group and Electronic Technologies Group both saw significant revenue growth.

- Despite the positive results, the stock is considered expensive compared to similar firms, and a downgrade might not be far into the future.

On August 29th, shares of HEICO Corporation ( HEI ) dropped around 1.4%. This decline came in response to management announcing financial results covering the third quarter of the company's 2023 fiscal year. Interestingly, there wasn't much on this front that was disappointing. While the company did see some margin contraction, revenue and earnings exceeded expectations. If I were a shareholder in the business, I would have been thoroughly pleased with the results announced by management. But this does not mean that I am turning bullish on the firm. Even after factoring in the company's latest acquisition, shares do look still to be rather pricey. In fact, given how expensive the stock is relative to similar firms, I am very close to downgrading the company from the 'hold' I had it at previously to a 'sell'.

A solid quarter

{kind=link}

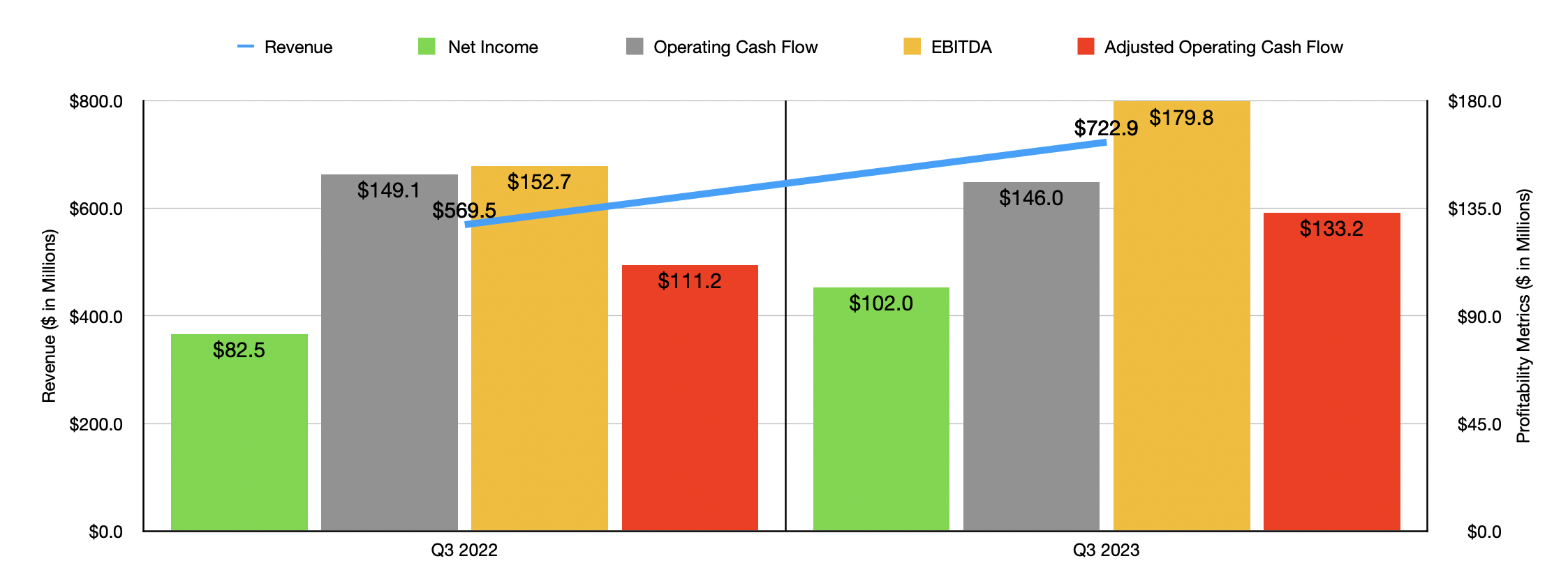

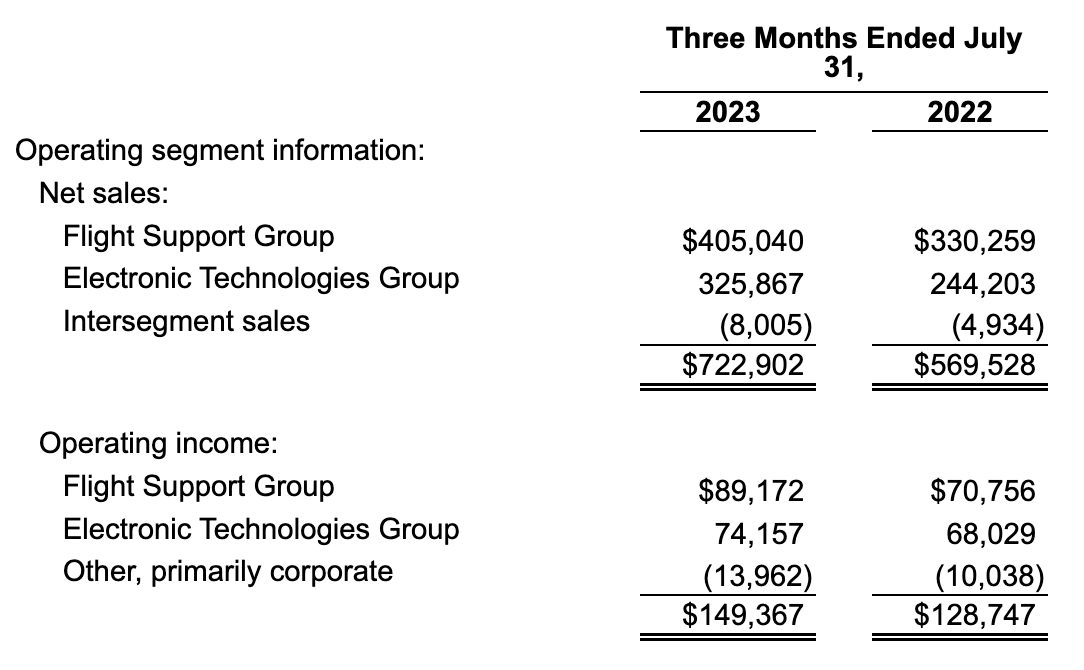

The management team at HEICO gave shareholders of the company a rather pleasant surprise after the market closed on August 28th. Financial results covering the third quarter of the company's 2023 fiscal year were rather solid. To start with, let's touch on revenue. During that time, sales came in at $722.9 million. That represents an increase of 26.9% compared to the $569.5 million in sales reported one year earlier. Both of the firm's operating segments performed quite well during this time. For instance, the Flight Support Group saw revenue shoot up 22.6% from $330.3 million to $405 million. It is important to note that the sales reported by management exceeded analysts' expectations by $15.9 million.

{kind=link}

This increase, according to management, was driven largely by robust organic revenue growth of 19%. This can be chalked up to higher demand in the commercial aerospace market, both for the products that the company sells and the services that it offers. As I have written about in prior articles , the aviation space has been showing impressive strength following years of pain caused by the COVID-19 pandemic. So it should not be a surprise to see sales pop like they did here. The rest of the growth, meanwhile, was driven by acquisitions that the company made in 2022.

Even more impressive was the Electronic Technologies Group. During the quarter, revenue came in at $325.9 million. That is 33.4% above the $244.3 million the company reported only one quarter earlier. The company did experience some organic growth under this segment. However, management made clear that the largest chunk of the increase, though they did not say how much, was driven by acquisitions, particularly the company's purchase of Exxelia.

{kind=link}

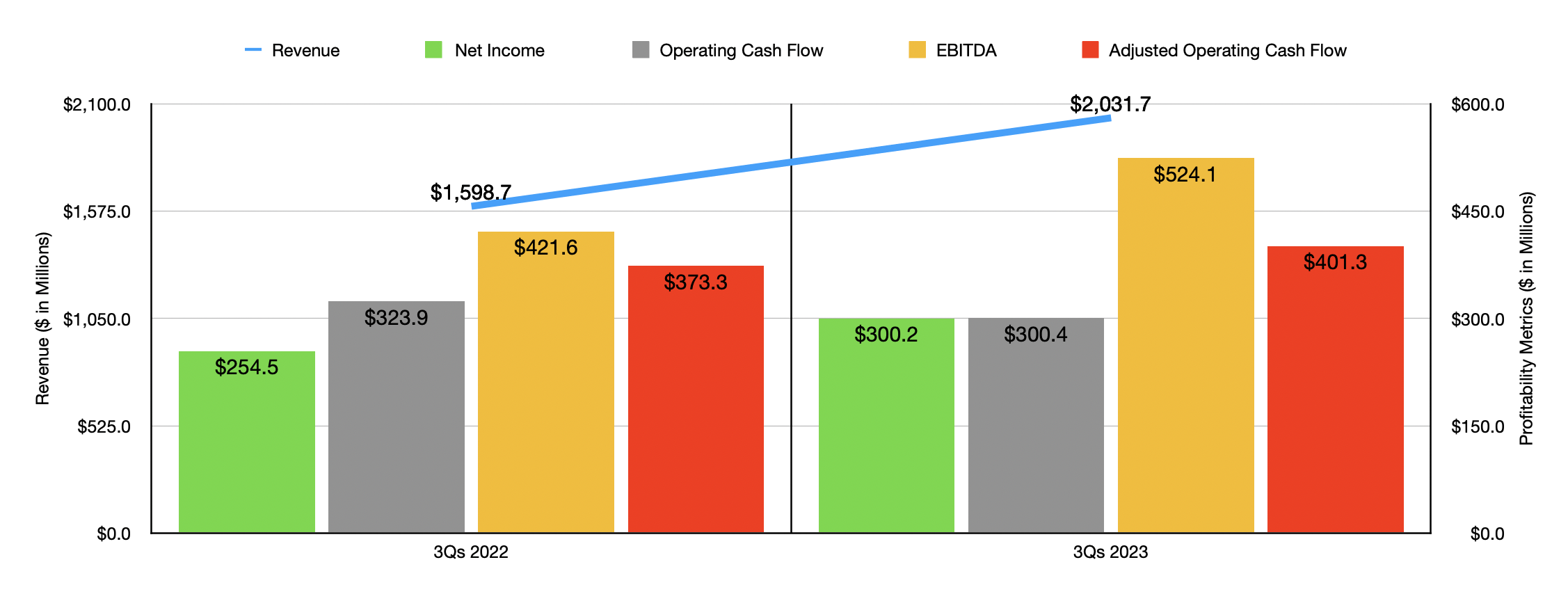

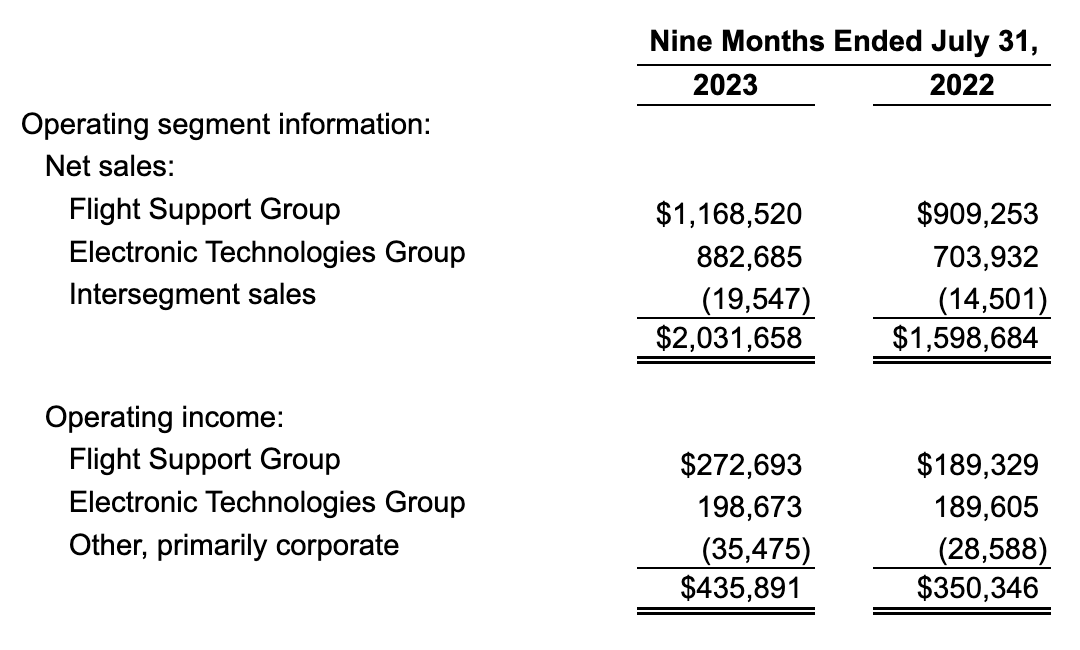

The growth in revenue brought with it higher profits. Net income of $102 million beat out the $82.5 million reported the same quarter last year. This translated to a net profit of $0.74 per share. By comparison, in the third quarter of 2022, profits per share totaled only $0.60. Once again, management exceeded expectations, with profits beating out forecasts by $0.02 per share. It is worth mentioning that the market seemed to be upset by the fact that the company's operating margin declined from 22.6% of sales last year to 20.7% this year. This was driven by a rise in selling, general, and administrative costs from 16.2% of sales to 17.9%. However, I saw nothing in the firm's financials that should convince us to prioritize operating margin over the fact that earnings exceeded forecasts. For the most part, other profitability metrics for the company came in stronger as well. It is true that operating cash flow dropped from $149.1 million to $146 million. But if we adjust for changes in working capital, we would get an increase from $111.2 million to $133.2 million. Meanwhile, EBITDA for the business shot up from $152.7 million to $179.8 million. For context, I also provided, in the chart above, financial results for the first three quarters of this year relative to last year, with the image below showing segment information for that same time period.

{kind=link}

Management has not really provided any detailed guidance for the current fiscal year, it would be fairly easy for us to value the company at this point. But we do have one problem. Subsequent to the end of the third quarter, management completed the largest acquisition in the company's history. This was of Wencor Group and it was completed in early August. This particular enterprise is a commercial and military aircraft aftermarket company that provides factory new aircraft replacement parts, as well as other goods and services, to its customers. The total purchase price came out to $2.05 billion, with $1.9 billion in the form of cash and $150 million in the form of common stock.

If we take the interest rate on the most recent debt that HEICO issued, and assume that all of the purchase price was covered with debt, we would get annual interest expense on that purchase of $100.7 million. For the 2023 fiscal year, Wencor Group is expected to generate $724 million in revenue and $153 million worth of EBITDA. Assuming there is no tax expense, the interest on this debt should translate to extra operating cash flow for the company of $52.3 million. If we add that on top of the annualized earnings and cash flow for the company based on the first three quarters of this year, we would get net profits on a pro forma basis of $467.2 million and adjusted operating cash flow of $603.8 million. EBITDA, meanwhile, would be around $891 million.

{kind=link}

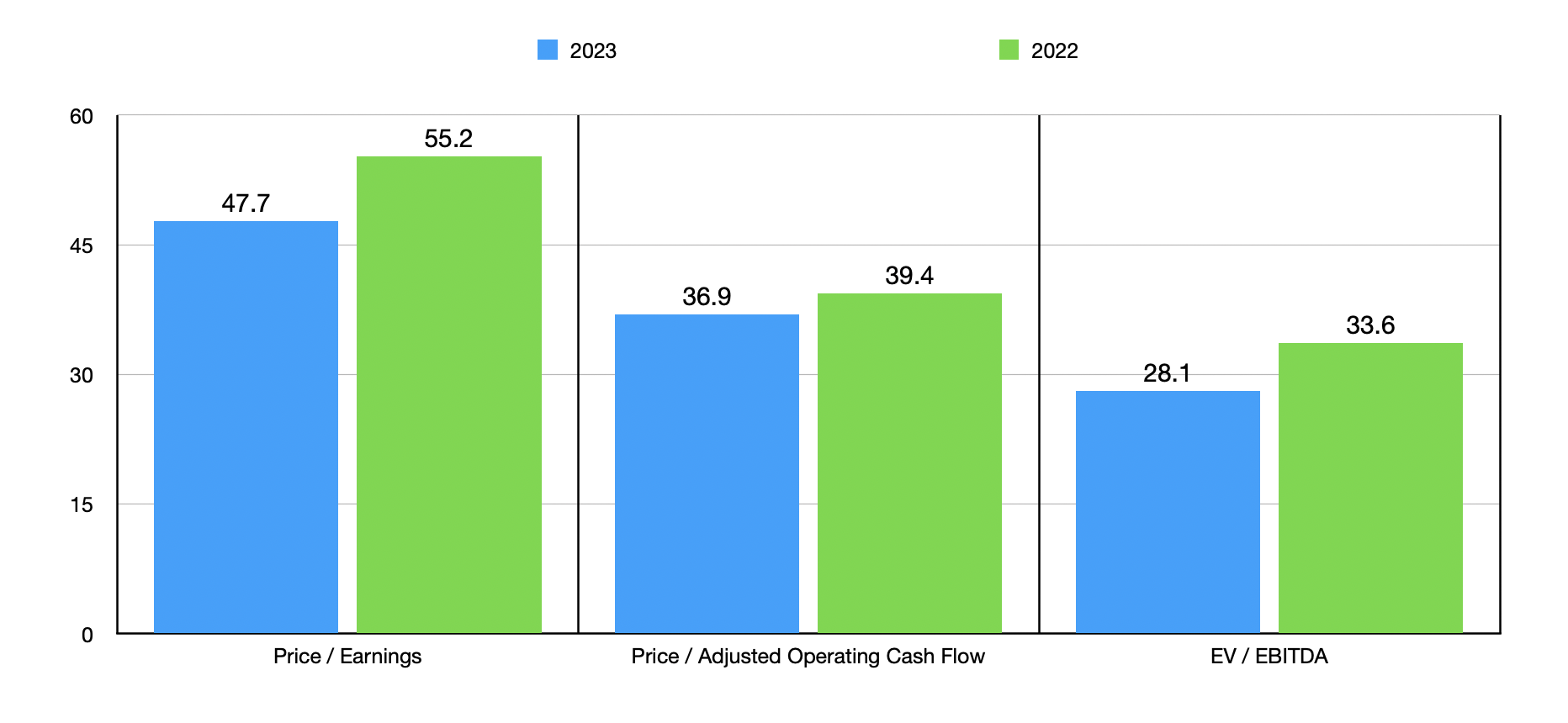

Taking these figures, I then was able to create the chart above. In it, you can see how shares are priced on a pro forma basis for 2023. I also applied the same profitability estimates for Wencor Group to results from 2022. Frankly, in either case, shares of HEICO look incredibly pricey on an absolute basis. Though it is positive that shares look cheaper on a forward basis. It means that financial performance looks set to continue to improve year after year. But of course, we should also see how shares are priced relative to similar firms. In the table below, I did precisely that. What I found was discouraging. On both a price to earnings basis and an EV to EBITDA basis, HEICO Ended up being the most expensive of the group. And when it comes to the price to operating cash flow approach, I found that four of the five companies were cheaper than it.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| HEICO Corporation |

| 47.7 |

| 36.9 |

| 28.1 |

| Howmet Aerospace ( HWM ) |

| 38.8 |

| 26.5 |

| 19.3 |

| Textron ( TXT ) |

| 17.5 |

| 11.9 |

| 10.7 |

| Elbit Systems ( ESLT ) |

| 33.3 |

| 54.5 |

| 18.5 |

| Rolls-Royce Holdings ( RYCEY ) |

| 11.5 |

| 7.5 |

| 6.2 |

| Huntington Ingalls Industries ( HII ) |

| 16.8 |

| 13.4 |

| 10.2 |

Takeaway

As much as I want to be bullish on HEICO because of the space in which it operates and because of the company's recent financial performance, I can't bring myself to take that leap. Yes, market participants were unhappy with financial results, even though the company exceeded expectations. The firm also continues to make interesting moves, such as the aforementioned acquisition. Long term, I have no doubt that the enterprise has excellent potential. But when you consider how pricey the stock is and you think about how many other prospects are out there that could appreciate more than it, I do believe that a more down to earth assessment is appropriate. I am still rating the company a 'hold' at this time, simply because it is a quality operation that continues to expand nicely. But if the stock does become any more expensive than it is right now, I do think a downgrade might not be too far off.

For further details see:

HEICO Corporation: Great Performance, But A Downgrade Might Be On The Horizon