HEI - HEICO Corporation: I Am Buying The Share Price Dip

2024-01-13 05:30:24 ET

Summary

- HEI's total revenue grew 34.4% and EBITDA reached $760 million, exceeding expectations.

- The FSG segment, driven by aftermarket replacement and specialty products, grew 21% organically and is expected to continue strong growth.

- HEI's PMA business is gaining market share and the acquisition of Wencor enhances their capacity to target more parts opportunities.

Summary

Following my coverage of HEICO Corporation (HEI), I recommended a buy rating as I believed the business had a very strong value proposition and business model. I expected the business to continue demonstrating attractive growth and expand its margins. The stock's valuation back then has also come down to a more attractive level, making the risk/reward better. This post is to provide an update on my thoughts on the business and stock. I remain buy-rated for HEI as the share price has taken a dip recently. I believe there is still plenty of room for HEI to penetrate the PMA space and its FSG segment to outperform due to the aging fleet of aircraft.

Investment thesis

HEI performance did better than my expectations for FY23 . Total revenue grew 34.4% (vs. my 32%) to $2.97 billion, and EBITDA came in at $760 million (vs. my $734 million). As for the quarter, revenue came in at $936 million, with FSG (Flight Support Group) revenue growing 20% organically, while ETG (Electronic Technologies Group) segment revenue was up 6% organically. 4Q23 exit segment EBIT margin also saw strong performance, coming in at 21.5%, and EBITDA margin coming in at 24.9% (which is close to my FY23 25.1% assumption).

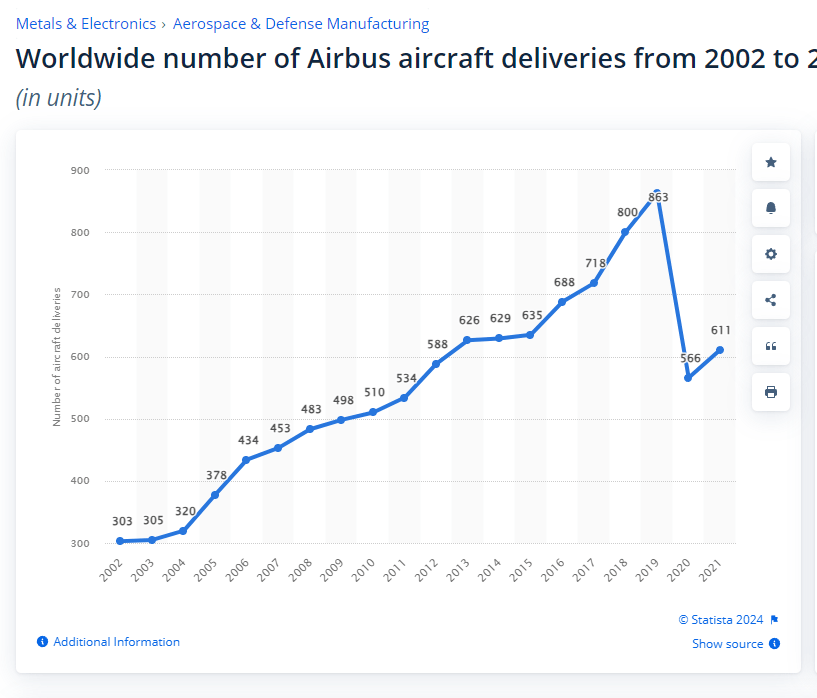

To start things off, I will touch on the HEI FSG segment, which I believe will continue to be a strong growth driver in the near term. As I noted earlier, FSG grew 21% organically, and if we include the Wencor contribution, reported y/y growth touched 41%, reaching a total revenue of $1.77 billion. The strong growth was driven by all business units within the segment (aftermarket replacement, repair and overhaul, and specialty products). Especially for the aftermarket sub-segment, I expect it to be the fastest-growing sub-segment among all due to the existing aging fleet of aircraft as well as revenue synergies from Wencor. With Wencor in HEI's portfolio, HEI's offerings of generic parts have expanded, giving it more opportunities to cross-sell across its entire customer base. On the point of the aging fleet, this is a big opportunity for upside in the next couple of years due to an expanding fleet of aircraft over 6 years old and out of warranty, given the large number of aircraft delivered in 2017-18.

{kind=link}

{kind=link}

In addition to volumes, I think HEI will continue to expand margins as well. Over the past few years, HEI has been increasing prices to maintain margins, as there have been cost increases over the past four years that have been significant in some cases. While it is HEI's philosophy to take care of its existing base of customers-hence, price increases are just to maintain margins-this is not the case for new customers. New customers will need to pay the new list price, which means the HEI margin will only continue to expand from here unless there is a massive deflation in parts prices across the board.

Cycling back to one of my favorite aspects of HEI, its PMA [Parts Manufacturer Approval] business, management believes it has continued to gain share in this business. My view is that HEI will continue to gain share in this space because the cost savings benefit is too much to ignore and that HEI is a trustworthy partner.

As you know, HEICO exists because its pricing is below the OEM, and that's the reason that they buy our products. We're 30%, 40% below, and this will give us the capacity to give even more value. 2Q23 earnings results call

Along with the substantial savings, HEI's ongoing investment in new product development-with 300 to 500 new products introduced annually-allows them to consistently capture a larger share of the market, strengthening their competitive position. With the addition of 150 new parts per year, Wencor's acquisition further enhances HEI's capacity to target more parts opportunities.

Yeah. I think -- you know HEICO has been running in that 300 to 500 area, roughly 400 parts a year. And Wencor has been running in about 150 area. So I would anticipate those numbers continuing that way. 4Q23 earnings results call

For those who think that there are not many parts left for HEI to penetrate an aircraft, I beg to differ. In an aircraft, millions of parts are required in order to make it work. Based on management comments, HEI only had a 2% market share of aircraft parts pre-Wencor, where it only had 12,500 PMA SKUs. With Wencor, HEI will have an addition of 6,000 SKUs, which I expect will help HEI capture more market share.

So, if you had to pin me down and guess what our market share -- the combined market share against OE aftermarket parts, I guess it's in the 2% area. I mean, it's very, very small. And that's why we think that there's a lot of opportunity to really grow, and frankly, look, it's 2%. We're never going to be -- we're never going to have the sales of some of these very large companies. 2Q23 earnings results call

Valuation

{kind=link}

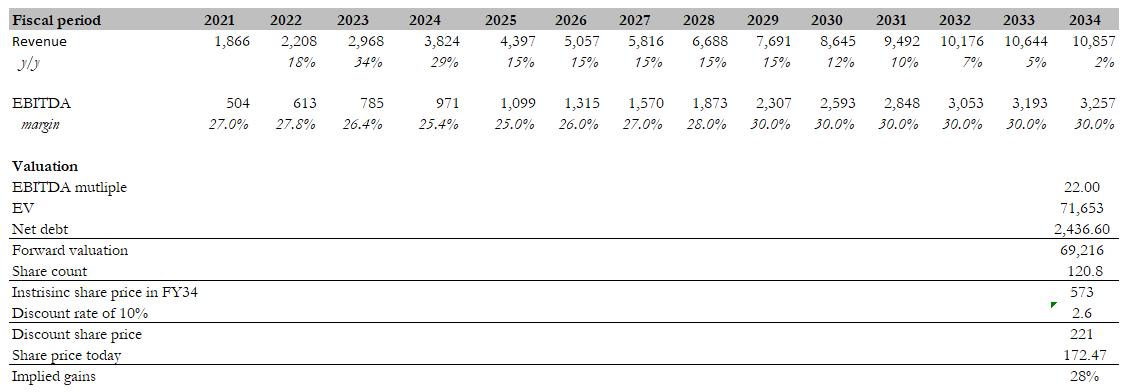

The market has been nice enough to offer long-term investors another opportunity to buy HEI at an attractive price. My DCF model this time around has been adjusted for consensus using the latest FY23 numbers and using consensus FY24 assumptions. My long-term growth assumptions remain the same in that I expect HEI to grow mid-teens, just as it did historically, with margins expanding. Previously, I used peer analysis to derive HEI's exit EBITDA multiple assumption. This time around, I compare HEI against its own valuation range. Over the past 10 years, HEI has traded within the range of 15x to 28x and at an average of 21.8x. I think a safe assumption to make here is that HEI should at least be trading at its historical average, given the fact that it is a much better business today than in the past. Attaching 22x forward EBITDA gets me my future target price of $572. Discounting the future share price using a 10% discount rate, I got a similar target price as I did previously, $221, representing 28% upside from the current share price.

Risk

The number of aircraft flying in the air impacts the revenue potential and growth of HEI. Any incidents or pandemic that would cause a significant decline in the number of airplanes operating worldwide will be detrimental to HEI performance (i.e., COVID).

Conclusion

I remain buy rated for HEI and consider the recent share price dip as a buying opportunity. The company's robust FY23 performance exceeded expectations, with total revenue growing by 34.4% and EBITDA reaching $760 million. I expect the aftermarket sub-segment to see strong growth ahead due to an aging aircraft fleet and expanded offerings from the Wencor acquisition. HEI's continued gains in the PMA business also support my bullish outlook.

For further details see:

HEICO Corporation: I Am Buying The Share Price Dip