TDG - HEICO: Flying Too Close To The Sun

2023-03-17 10:00:00 ET

Summary

- HEICO has compounded at a 22% CAGR over the last 32 years.

- The company has a robust business with sticky products.

- HEICO's entrepreneurial culture and 20% of insider ownership help its continued growth.

- Multiples expanded dramatically over the last decade and HEICO has been very richly valued for quite some time.

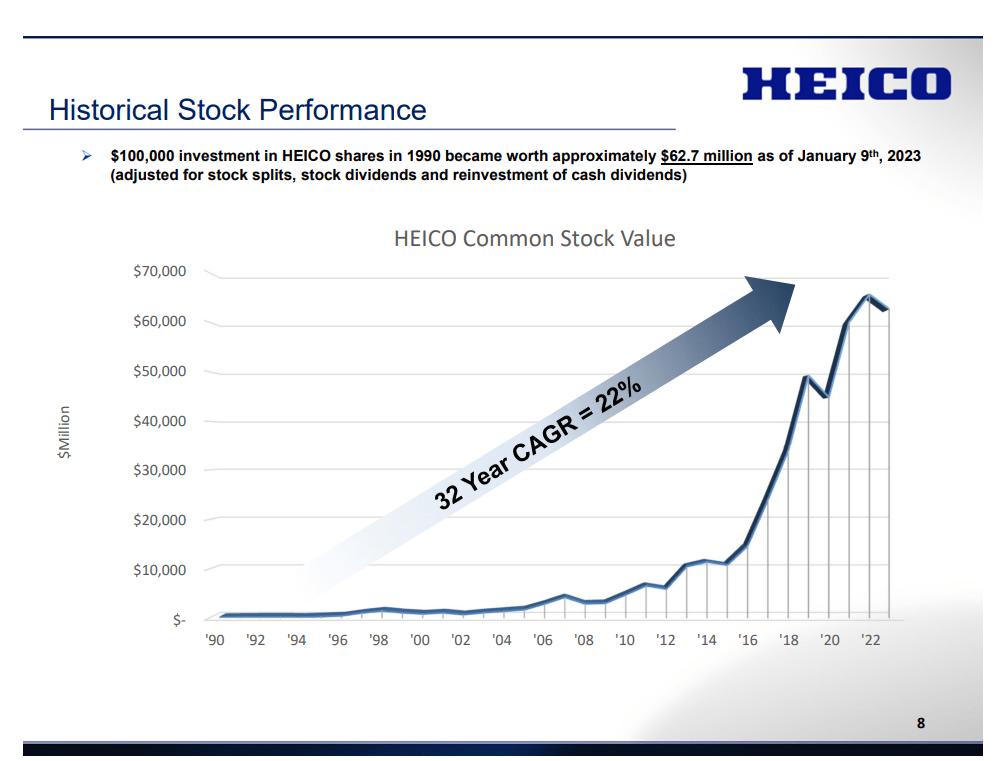

HEICO Corporation (HEI) has been one of the high fliers of the last 30 years, generating a 32-year share price CAGR of 22%. This mind-blowing performance would have turned $100 in 1990 into $62,700 in 2023. Let's see if the stock is likely to continue its outperformance.

Historical Stock Performance (Heico Investor Presentation)

{kind=link}

An industry with high barriers of entry

HEICO is split into two operating groups:

- Flight Support Group (60% of revenues, 50% of operating income) designs, manufactures and sells jet engine parts and aircraft component replacement parts, typically at lower prices than original equipment manufacturers (OMEs).

- Electronic Technologies Group (40% of revenues, 50% of operating income) manufactures and sells various types of electronic, electro-optical, microwave and infrared equipment, amongst others.

The company generates most of its revenues from Commercial Aviation (43%) and Defense (34%), with the remaining revenue coming from Space (5%) and Other industries (18%).

Aircraft components and electronic components are two exciting end markets. Aircrafts, especially, are large ticket items selling for millions of dollars and in small quantities. Each machine has thousands of parts and once a part is inside the plane, it has to be replaced with a fitting part eventually. Due to the relatively small cost of replacement parts compared to the airplane, it's unlikely that a customer will choose a different manufacturer once it's used in the machine's blueprints. This means low customer churn and sticky business relationships. Heico adds between 300-500 parts with Part Manufacturer Approvals ('PMA') to its portfolio each year, totaling 12,200 PMAs. This results in excellent unit economics and diversification through the number of different parts. It reminds me a lot of the analog semiconductor industry , which also has small ticket items. For example, Texas Instruments (TXN) has over 100,000 products and 80,000 customers, with the average selling price for its chips around $0.5.

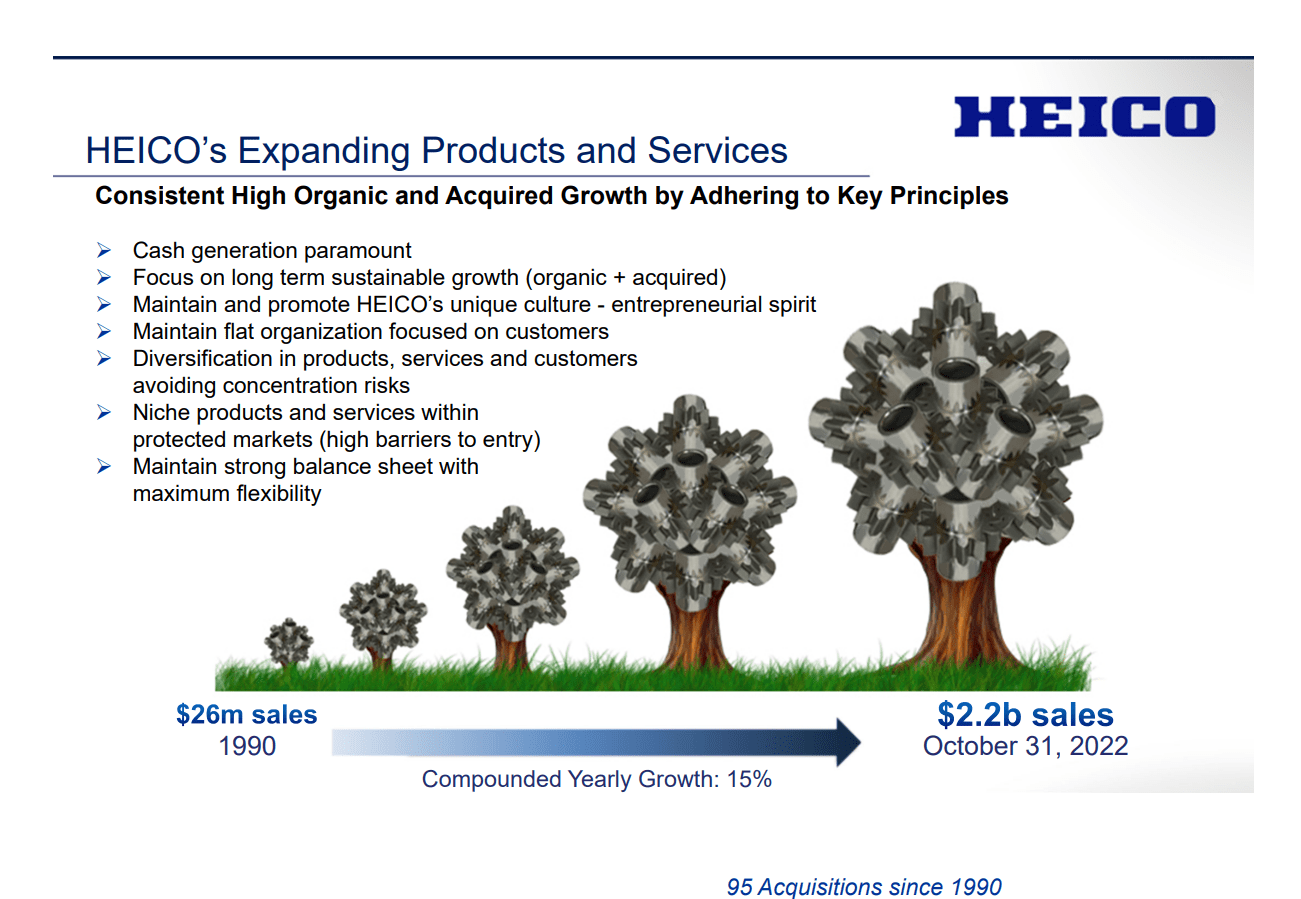

HEICO's strategy

HEICO focuses on a strong, entrepreneurial culture with sustainable cash generation as the primary goal. Over the last 30 years, the company acquired 95 companies and integrated them into its product portfolio. Acquisition targets need to broaden the product offering and expand the customer base and geographic presence of HEICO. Furthermore, they need to continue growing with strong cash flows. Unlike its competitor TransDigm (TDG), HEICO has a conservative balance sheet with the flexibility to lever up for bigger deals at just 1.0 times Net debt/EBITDA. TransDigm, on the other hand, runs a very levered balance sheet with a 6.3 times Net debt/EBITDA ratio and 5.7 times on average. While both strategies have merits, I prefer a conservative approach like HEICO's.

HEICO's expanding products and services (HEICO Investor Presentation)

{kind=link}

Skin in the game

I prefer to invest in companies where the management team has aligned incentives with shareholders. This can be achieved through various means, but the most important ones are equity ownership in the company (skin in the game) and executive compensation plans. Let's look at the latest proxy statement .

Heico prides itself on its ownership culture and insider ownership so much that it is written on the first page of its Investor Presentation. The board of directors, management and team members own around 20% of Heico, a significant amount of skin in the game. Most of this is with the Mendelson family, who owns 16.8% of the company.

If we look at executive compensation, we can see that it is pretty simple. The base salary is based on Sales, Net Income and Cash Flow growth. The bonus is based on Net Income, EBITDA and Operating Cash Flow growth with a 10% threshold. Both of these compensation packages are in cash. Sadly there isn't much light shed on the long-term incentives in the proxy.

Overall this simple compensation structure focuses on the company's fundamental performance, which is a positive.

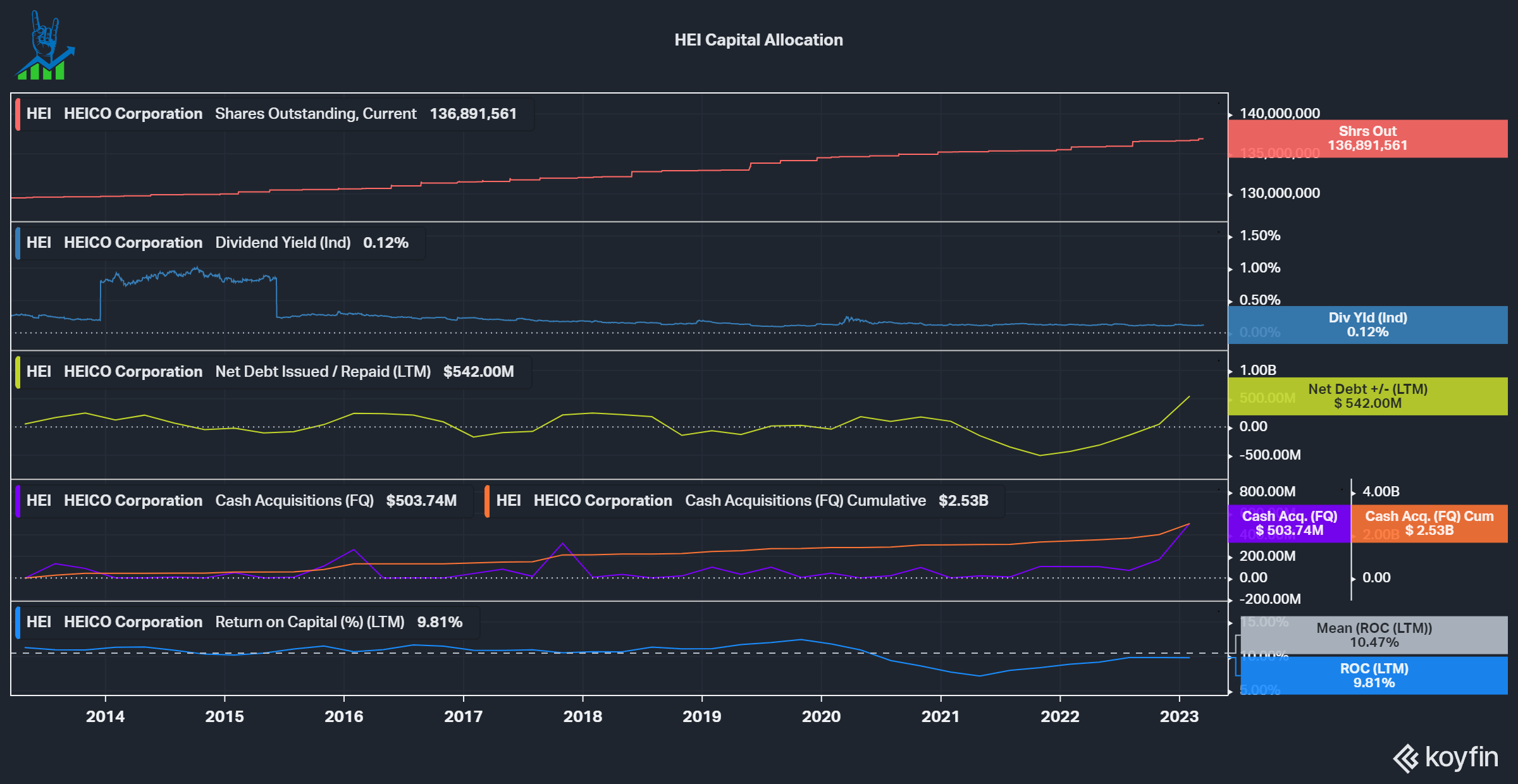

Capital Allocation

In the chart below, we can see HEICO's capital allocation. HEICO generated $2.91 billion in Free Cash Flow over the last decade, so they had plenty of Capital to allocate. We can see that the company continues to dilute its shareholders, raising outstanding shares by 5% over the last decade. The company pays a growing dividend but at a median yield of 0.28%, and this is distorted upwards from the special dividend in 2014; it's not much of a talking point. Most of the capital allocation goes toward acquisitions, where the company spent $2.53 billion over the last decade, nearly its entire $2.91 billion in FCF. Return on Invested Capital is a proxy for the effectiveness of a company's capital allocation. The chart below shows that HEICO only generated a median ROIC of 10.5%. As a rule of thumb, we want a company that produces ROIC at least 2% above its cost of Capital. HEICO's Cost of Capital comes in at 11.2%, below its ROIC. This should raise warning signs, but it looks much better if we adjust for Goodwill. The $2 billion of Goodwill is around half of the $3.87 billion in Total Capital invested into HEICO. If we adjust for it, we get around a 20% ROIC. I believe that for acquisitive companies, investors should adjust Goodwill because it is a price paid in the past and not an actual value the company could sell.

HEICO Capital Allocation (Koyfin)

{kind=link}

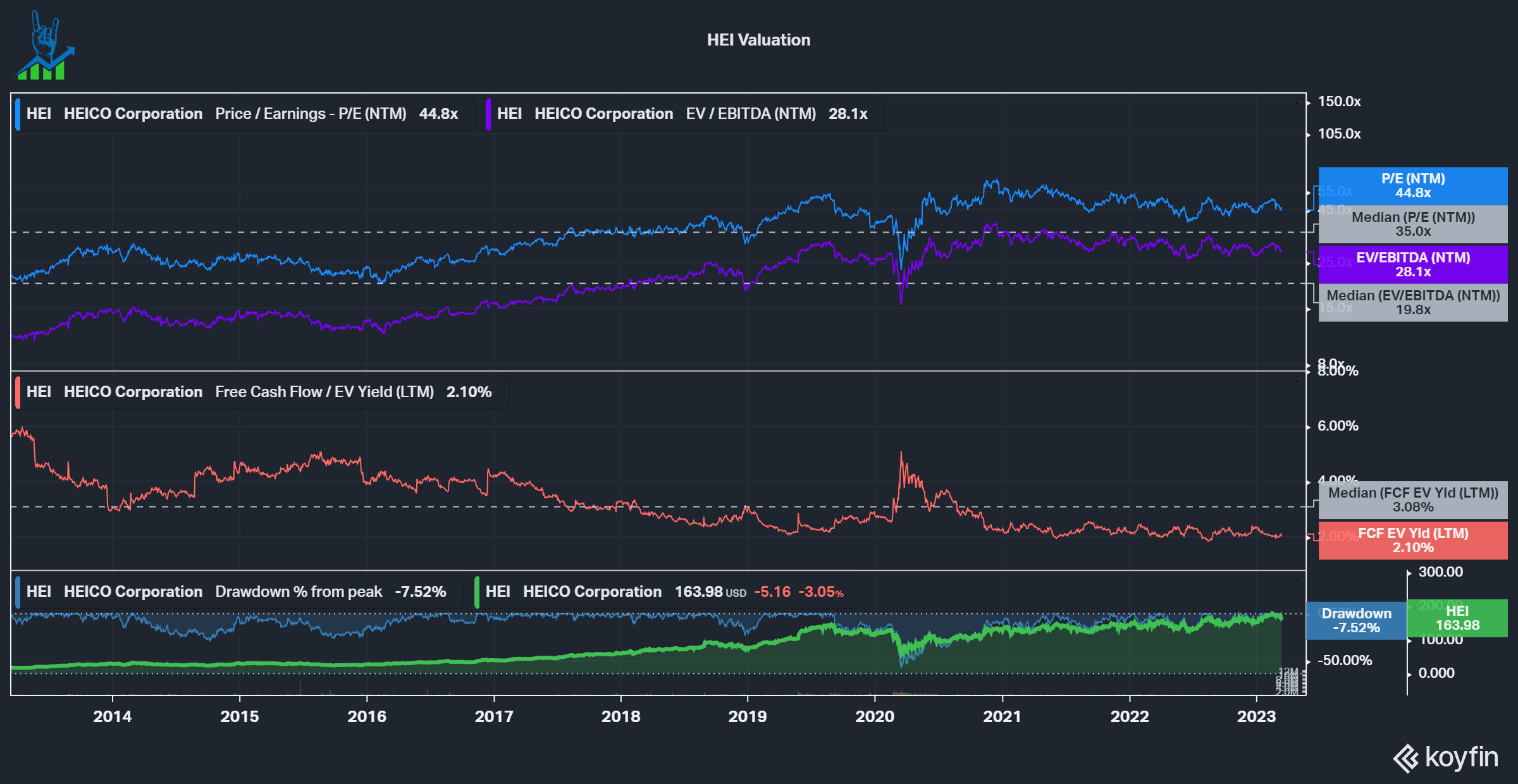

Valuation

HEICO is a high-quality company, but at the end of the day, even a great business can be a lousy investment if one pays too much for it. If we look at the last decade of valuation multiples for HEICO, we can see that multiples kept rising from 20 PE to 44 and from 10 EV/EBITDA to 28 times in 2023. This is a massive part of the reason HEICO generated total returns of 780% while EBITDA only grew 207%.

{kind=link}

If we look at the valuation from an Inverse DCF point of view, we see that at a 10% discount rate, assuming a 0.5% annual dilution in line with the past decade and a 3% perpetual growth rate, HEICO would need to grow FCF at a 20% CAGR to justify a 10% CAGR in its share price. I do not see how the multiple could expand further from this level and 20% is a high bar to achieve, even for a high-quality business like HEICO. To conclude, HEICO is a classic example of a great business that's simply too expensive. Shares would need to come down significantly to consider adding the company to my portfolio. There are many companies of equally high-quality trading at much more sensible valuations. Maybe HEICO will pull off this kind of growth, but I do not like the risk-reward here.

HEICO Inverse DCF (Authors Model)

For further details see:

HEICO: Flying Too Close To The Sun