HEI - HEICO: Insanely Overpriced Or Extremely Underappreciated?

2023-11-26 23:41:39 ET

Summary

- HEICO's acquisition of Wencor Group is expected to positively impact earnings, with estimated revenues of $911.8 million for Q4 2023.

- The consensus is that HEICO will generate $0.66 in earnings per share, marking a 5% decline.

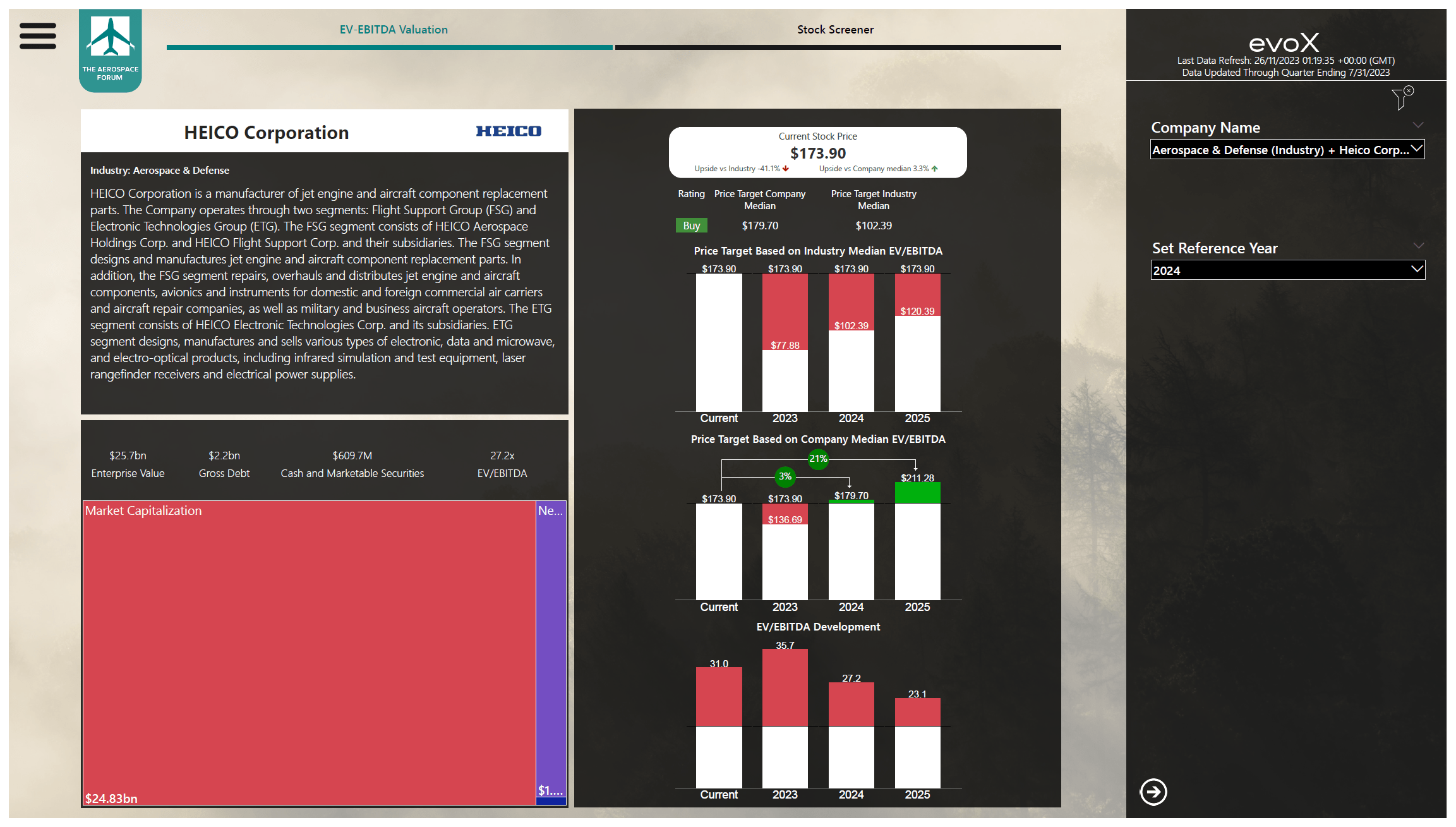

- The stock is trading at an elevated EV/EBITDA multiple, but there is still potential for a 21% upside to $211.28 per share.

In a previous report, I analyzed the Q3 2023 financial results and concluded that the 6% dip in stock prices provided a nice opportunity for investors. It seems to have been an easy call as the stock value rebounded more than 5%, outperforming the market. Indeed, you won’t get poor buying the dip, but the reality is also that the stock price has not fully recovered from the dip. In this report, I will be previewing Q4 2023 earnings and re-assessing my rating and price target for the stock.

Wencor Acquisition To Positively Impact Earning

In August, HEICO (HEI) completed the acquisition of Wencor Group for $1.9 billion in cash and 1.138 million shares of HEICO Class A Common stock. Wencor Group offers factory-new FAA-approved replacement parts as well as MRO capabilities. The company with $724 million in pro-forma sales for 2023 will be integrated into HEICO’s Flight Support Group and has an adjusted EBITDA of $153 million indicating a margin of 21.1%.

For the fourth quarter, the revenues are estimated to be $911.8 million, indicating 50% year-over-year growth. I don’t think that 50% growth comes as a major surprise. In the third quarter, we already saw the revenues grow 28% and the Wencor acquisition provides an additional $181 million in revenues. If we were to apply the nine-month total growth rate to HEICO’s Q4 2022 results and add the Wencor acquisition, we would get to $948.5 million for Q4 2023 net sales which is higher than the $911.8 million that analysts are expecting. Possibly there is some space to outperform or the recovery growth rate of the HEICO business without Wencor is going to taper a bit. Either way, when it comes to revenues, the company has quite a good track record. Over the past two years, it missed revenue estimates once in eight quarters and over the past 16 quarters it missed revenue estimates only twice.

The consensus is that HEICO will generate $0.66 in earnings per share which would mark a 5% decline in earnings per share. I would put the net income per share related to Wencor at $0.15 per quarter. For Q4, initially, the expectations were that HEICO would record earnings per share of $0.85 but that has since come down to $0.66 while the dilution of shareholders has only been 1.6% to finance part of the Wencor acquisition. So, there is likely some cost impact to be expected but during the third quarter, the company could not provide specifics other than the expenses related to the acquisition would be lower than 1% of the acquisition price and no huge inventory write-ups or write-downs that would be capture under purchase accounting.

What I find somewhat unfortunate is that the Wencor acquisition is HEICO’s biggest acquisition but the company has not been able to prepare a full overview and fair value assessment of the Wencor acquisition as noted in their 10-Q filing.

What Is The Price Target For HEICO Stock?

{kind=link}

If we consider the balance sheet data and forward projections for HEICO, there is one thing that becomes clear and that is that it's trading at an EV/EBITDA multiple significantly higher than that of peers, and the company is even trading ahead of its 10-year EV/EBITDA. The reason for this seems to be that the company has been significantly expanding its business via M&A with 23 businesses acquired in the past five years alone. Using the five-year average EV/EBITDA instead of the 10-year median gives and allowing the stock to trade against FY2025 earnings there is 21% upside to $211.28 per share and according to my stock screener, the stock has a buy rating.

Conclusion: HEICO Stock Might Not Be Everyone’s Cup Of Tea

HEICO’s merger and acquisition is a strong one which has resulted in strong share price appreciation over the longer term. I think the company will continue to expand its business with the same mindset riding the demand trends in its end markets. Whether HEICO Corporation stock is worth your investment really depends on whether you can stomach their elevated EV/EBITDA valuation in recent years which is driven by the increased M&A activity. Acquiring businesses at the rate seen with HEICO requires time to deleverage and become fully accretive, so the EV/EBITDA being elevated might be somewhat justified and would provide around 20% upside. What might also be something that is not fully appreciated about HEICO is that it provides over 4 million certified parts a year, giving it a market share of over half of the certified parts distribution excluding OEM-supplied parts. However, if you cannot accept the premium valuation, then this stock is at best a hold.

For further details see:

HEICO: Insanely Overpriced Or Extremely Underappreciated?