HEI - HEICO: Optimistic Guidance Backlog Generation And Inexpensive

2023-03-18 06:49:57 ET

Summary

- HEICO is a North American company considered to be the world's largest manufacturer of engineering systems for aircraft as well as parts and replacement parts.

- I assumed that the recent increase in research and development expenditures, mainly in the FSG business segment, and new research will likely bring more product offerings, and more patents.

- HEICO reported an impressive backlog increase recently and expects sales growth in 2023 driven by product. We are talking about a backlog increase of 42% y/y, which appears quite impressive.

HEICO Corporation (HEI) continues to report backlog increases, and management was recently quite optimistic about the net sales growth in 2023 and the inorganic growth activities. In my view, further increases in research and development, more products, and cost reduction will likely lead to FCF growth. Like other analysts, in my opinion, sales growth could continue in 2023, 2024, and 2025, and the stock is not expensive.

Business Model, Established Relationships With Clients, And Recent Backlog Increase

HEICO is a North American company considered to be the world's largest manufacturer of engineering systems for aircraft as well as parts and replacement parts approved by the Federal Aviation Administration. Similarly, it is said to be the largest manufacturer of electronic devices for aircraft and other industries, such as medical, space, telecommunications, and defense.

HEICO divides its operations into two reportable segments: the flight support segment and the electronic technologies segment. The former consists of HEICO Aerospace Holdings Corp. and HEICO Flight Support Corp. in addition to their associated subsidiaries. In 2022 and the three months ended January 31, 2023 , the company reported sales growth in its both business segments, which I believe is a very good reason to have a look at HEICO today.

Source: 10-Q Source: Investor Presentation

With technologies developed under its intellectual property, HEICO Aerospace manufactures and designs aircraft components, mostly intended to replace original parts produced by aircraft manufacturers and approved by the Federal Aviation Administration. In addition to engineering systems and parts in this regard, the company also develops various equipment and devices for use in private aircrafts, commercial flights, and military activities. Finally, HEICO, through its aircraft manufacturing activity, is the main supplier of the United States Ministry of Defense as well as hydraulic parts for the U.S Navy.

HEICO Electronic Technologies Corp designs, develops, and produces various types of electronic systems as well as optical specialty products, among which we find lasers, electrical power generator supplements, emergency transmitters, capacitors, amplifiers, antennas, various components, panels, and indicators among others.

The company sells its products primarily through skilled employees and to a lesser extent through independent vendors. HEICO maintains business relationships of many years as well as a close relationship with the chamber of the aerospace industry in the United States, being a great value in the commercial and operational sense for the company. I do not think that we can talk about recurrent revenue, but I would expect less revenue volatility than new entrants in the market without established relationships.

Among its clients we find aviation operations companies, both local and foreign, repair facilities, and distributor and retail stores, especially in the electronic components segment. None of these clients currently accounts for more than 10% of the business, while net sales to the top five clients accounted for 23% or similar percentages in the last three years. Therefore, I do not really see risks from the concentration of clients.

Finally, another beneficial feature to remark is the recent increase in consolidated backlog reported in the last quarterly earnings release and backlog increase in 2022. We are talking about a backlog increase of 42% y/y, which appears quite impressive.

The increase in net working capital is inclusive of a $52.0 million increase in inventories to support an increase in consolidated backlog, a $7.3 million increase in contract assets and a $7.1 million increase in accounts receivable resulting from the timing of collections. Source: 10-q

Our total backlog increased by 42% to $1,383 million as of October 31, 2022, up from $977 million as of October 31, 2021. The majority of our backlog of orders as of October 31, 2022 is expected to be filled during fiscal 2023. Source: 10-k

The Company Expects Sales Growth For 2023 And Product Development, And Market Expectations Are Beneficial

I believe that the year 2023 will likely be beneficial for HEICO. Management noted sales growth expectations in 2023 in both business segments driven by demand from clients. It is also worth noting that management expects to acquire new companies, and launch new products, which will likely bring revenue growth.

As we look ahead to the remainder of fiscal 2023, we continue to anticipate net sales growth in both the FSG and ETG, principally driven by demand for the majority of our products. Source: 10-Q

During fiscal 2023, we plan to continue our commitments to developing new products and services, further market penetration, and an aggressive acquisition strategy while maintaining our financial strength and flexibility. Source: 10-Q

Market analysts are expecting 2025 net sales of $3.117 billion, a 2025 net sales growth of 6.60%, and 2023 sales growth of 23%-24%. In addition, 2025 EBITDA would stand at $855 million accompanied by an EBITDA margin of 27.43%. 2025 operating profit will likely be close to $728 million with an operating margin of 23.30%. Finally, net income would stand at $529 million with 2025 FCF of around $616 million and a FCF margin of 19.80%.

Source: Marketscreener.com

Balance Sheet

As of January 31, 2023, the company reported cash worth $142 million in addition to accounts receivable close to $325 million, contract assets worth $101 million, and inventories of $697 million. Prepaid expenses stood at $51 million, which implied total current assets of $1.31 billion.

Property, plant and equipment was equal to $274 million along with a goodwill of $1.994 billion, intangible assets of $873 million, and total assets of $4.804 billion. The asset/liability ratio stands at more than 2x, so I think that the balance sheet appears in great shape.

Source: 10-Q

Liabilities included current maturities of long term debt of $1 million, trade accounts payable worth $134 million, and accrued expenses of around $290 million. In addition, payable income taxes were $26 million, and total current liabilities were close to $453 million.

Long term debt, net of current maturities stood at $781 million together with a deferred income tax of $113 million and other long term liabilities of $372 million. In sum, total liabilities were equal to $1.720 billion.

Source: 10-Q

The Assumptions In My Financial Model Include Successful R&D Activities, Successful Acquisitions, And Integration Of Targets

Under my financial model, I assumed that the recent increase in research and development expenditures, mainly in the FSG business segment, and new research will likely bring more product offerings, more patents, and more recognition in the industry. As a result, I believe that HEICO may receive more attention from clients, and revenue will likely trend north.

As part of our growth strategy, we have continued to increase our research and development activities. Research and development expenditures by the FSG, which were approximately $.3 million in fiscal 1991, increased to approximately $22.2 million in fiscal 2022, $18.3 million in fiscal 2021 and $19.1 million in fiscal 2020. We believe that our FSG's research and development capabilities are a significant component of our historical success and an integral part of our growth strategy. In recent years, the FAA granted us PMAs for approximately 300 to 500 new parts and we develop numerous new proprietary repairs per year. Source: 10-k

I also expect improvements in quality and new products as well as cost reduction in the manufacturing activities. In particular, in the aircraft production segment, the company intends to manufacture new specialized parts and components, while in the development of its electronic technologies, HEICO is currently seeking to develop simple products that allow it to position itself in new retail markets.

Besides, I assumed that HEICO will successfully maintain its reputation, and pricing strategies will continue to successfully bring operating margin improvements. For starters, I believe that the following text about the current reputation of HEICO as a manufacturer and provider of niche products for commercial satellites is worth a look.

We believe that, based on our competitive pricing, reputation for high quality, short lead time requirements, strong relationships with domestic and foreign commercial air carriers and repair stations (companies that overhaul aircraft engines and/or components), and successful track record of receiving PMAs and repair approvals from the FAA and commercial air carriers, we are uniquely positioned to continue to increase the products and services offered and gain market share. Source: 10-k

We believe we are a leading supplier of the niche products which we design and manufacture for this market, a market that includes commercial satellites. Our customers for these products include satellite and spacecraft manufacturers. Source: 10-k

HEICO implemented successful acquisition strategies for years, which allowed it to access new markets and expand its activities both commercially and geographically. Since 1995, there have been 90 acquisitions to date. I assumed that new acquisitions will occur, and the integration of targets like Exxelia will be successful. As a result, inorganic growth will most likely enhance the fair valuation of HEICO.

We typically target acquisition opportunities that allow us to broaden our product offerings, services and technologies while expanding our customer base and geographic presence. Even though we have historically pursued an active acquisition policy, our disciplined acquisition strategy involves limiting acquisition candidates to businesses that we believe will continue to grow, offer strong cash flow and earnings potential, and are available at fair prices. Source: 10-k

Source: 10-k

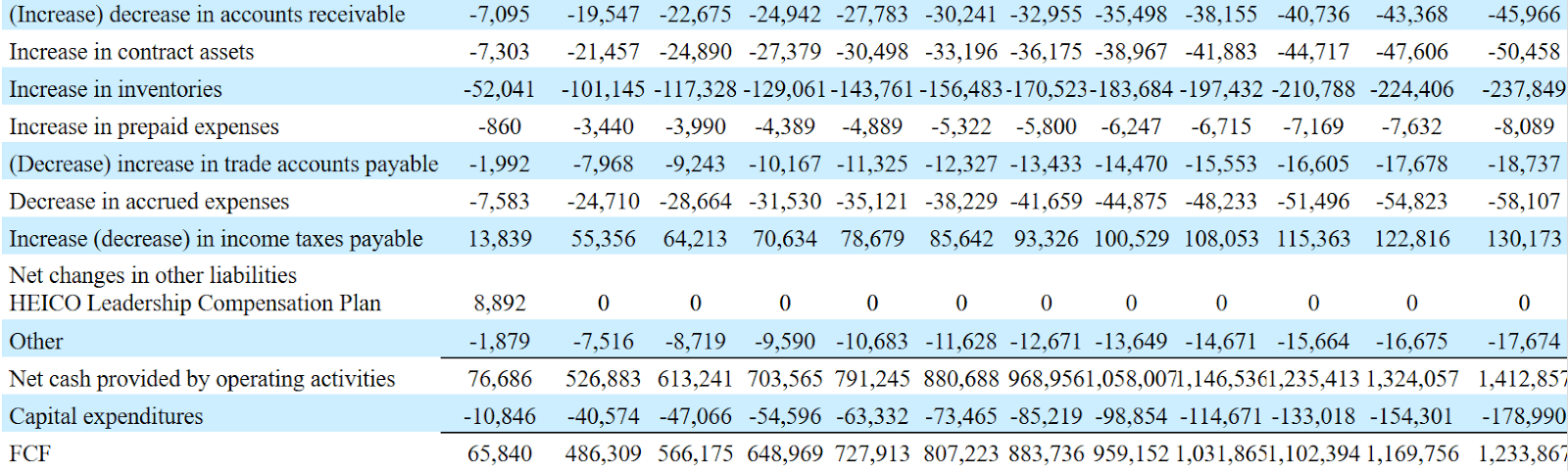

My Financial Model

My projections include 2033 net income of $1.142 billion, depreciation and amortization of $509 million, and a share based compensation expense of $45 million. Besides, I anticipate a deferred income tax provision of $9 million.

{kind=link}

I also included a 2033 decrease in accounts receivables of -$45 million, an increase in contract assets of -$50 million, an increase in inventories of -$237.5 million, and an increase in prepaid expenses of $8.5 million.

Changes in accounts payable would be -$18.5 million along with changes in accrued expenses of around -$58.5 million. Additionally, with an increase in income taxes payable of $130.5 million, I obtained 2033 net cash provided by operating activities of $1.4125 billion, capex of -$178.5 million, and 2033 FCF of $1.2335 billion.

{kind=link}

If we also assume an exit multiple of 41x FCF, the residual value would stand at $50.5 billion, and with a WACC of 8.655%, the implied enterprise value would be $26.05 billion. Besides, with cash close to $142.5 million and a debt of around $783.5 million, the implied equity would be $25 billion, and the fair price would be $186.55.

Source: Internal Estimates

Competitors And Risks

The competition in the market in which the company operates is very high due to a large number of companies that may have more recognition, access to resources, and investment capabilities than HEICO. With regard to aircraft manufacturing, the company competes with original manufacturers as well as some companies that have their own facilities for aircraft repairs and maintenance services. In the electronic technology segment, the market is populated by small producers, national and foreign, where larger producers and resources also appear.

HEICO depends directly on aviation activity, which, for example, was completely paralyzed during the restrictions due to the COVID pandemic. Similar events could seriously affect the company's operations. In other words, in addition to competition and possible complications in the supply of raw materials for manufacturing, HEICO faces its own volatilities and critical situations in the global economy.

A reduction in the expenses destined by the government agencies to the areas of development in defense, space, or national security in the United States would also affect the majority sales channel that the company has to date.

More generally, the inability to integrate its future acquisitions into the existing business model or the loss of employees who hold substantial positions in its subsidiaries and potential acquisitions could complicate the growth and development strategy for the company. Besides, goodwill impairments would most likely not be appreciated by investors, which would sell equity leading to stock price decreases.

Conclusion

HEICO reported an impressive backlog increase recently, and expects sales growth in 2023 driven by product demand, mergers, and acquisitions. I also assumed that the increase in research and development will likely lead to product offering enhancement and new patents. With many other financial analysts expecting great results from HEICO, I believe that stock price is still not expensive. Even taking into consideration risks from failed mergers and acquisitions or lower governmental expenditures, I believe that HEICO is a must-follow stock.

For further details see:

HEICO: Optimistic Guidance, Backlog Generation, And Inexpensive