HEI - HEICO: Wait For A Better Buying Opportunity

2023-03-20 03:45:25 ET

Summary

- The strong results for the first quarter of fiscal 2023 show that HEICO is growing rapidly.

- HEICO is operating in a growing market as the need for defense spending increases due to increased global threats.

- The profit margin is high at 15%, but it pays out only a small portion of its profits to shareholders in the form of dividends.

- Looking at the stock valuation, HEICO is expensively valued based on its PE ratio and enterprise value to free cash flow.

- I would wait for a better buying opportunity when the share price has corrected from this high price level.

Introduction

HEICO (HEI) (HEI.A) operates in the aerospace and defense industry and derives its revenues from two business segments: Flight Support Group ((FSG)) and Electronic Technologies Group ((ETG)). The first business group designs, manufactures and repairs FAA-approved parts for MRO companies. The second business group develops electronic products for aerospace, defense, medical and other industries.

The stock has risen sharply over the past 10 years, much more than the return of the S&P500. Investors who invested 10 years ago saw their position increase 9 times.

Now that the stock has risen so much, so has its valuation. That's why the stock is on hold.

Strong Results, Good Outlook, And Strong Performance

HEICO posted strong results for the first quarter of fiscal 2023 , with net sales up 27% year-on-year thanks to the impact of its Exellia and other recent acquisitions. Organic growth in net sales was also strong at 25%, and operating income also grew 27%.

Looking to the future, HEICO expects demand for commercial aviation to remain strong this year and beyond and defense sales to grow strongly late this year and beyond as higher defense budgets are materialized. The DoD budget ( FY '23 Omnibus spending bill ) was increased 10% to $858 billion. And the increased risks from the war between Russia and Ukraine should also be a catalyst for further increases in defense spending, which would benefit HEICO to enable long-term growth.

The global aerospace and defense market grew from $796 billion to $856 billion year-on-year, at a CAGR of 7.5%, mainly due to the war between Russia and Ukraine. The total addressable market is expected to grow at a CAGR of 5.9% through 2017. The research paper describes that North America was the largest region in the aerospace and defense market in 2022 and is expected to be the fastest growing region in the near future. HEICO operates in a growing market and the increased defense budget will be a growth catalyst. This sounds good, so how did the company perform in the past?

HEICO's revenue has increased 6% annually over the past 4 years, while non-GAAP EPS has increased 7.6%. 11 analysts are positive on the earnings outlook as they expect strong earnings and revenue growth; earnings are expected to rise 19% this year and 15% next year.

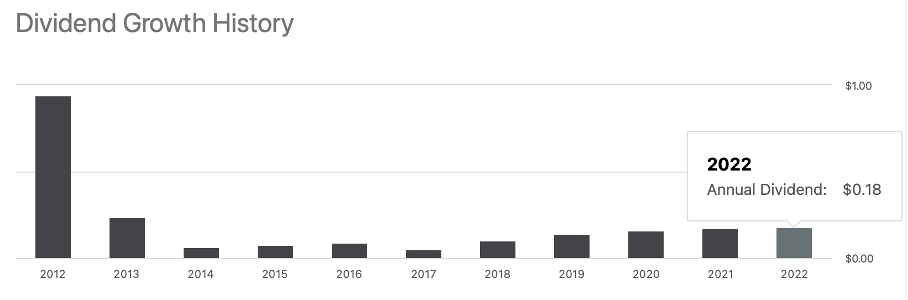

The profit margin is high at 15%. However, HEICO pays only a small dividend per share of $0.20, representing a dividend yield of only 0.12%. The dividend has grown steadily over the past 5 years, averaging 29% growth per year. Next year, the dividend is expected to double to $0.24 per share.

Dividend Growth History (HEI.A ticker page on Seeking Alpha)

{kind=link}

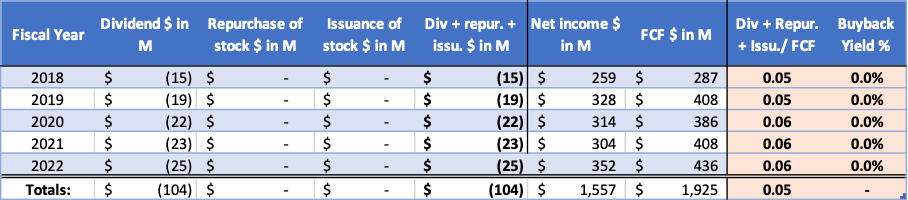

HEICO distributes only 6% of the free cash flow generated to shareholders. So the distribution is easily manageable for the long term. The balance sheet shows that the company has $143 million cash and $781 million long-term debt (and only $2 million short-term debt). So net debt is $640 million. With free cash flow of $436 million, the company can easily manage its debt. Now we look at the valuation of the stock, an important part of the purchase decision.

HEICO's cash flow highlights (SEC and author's own calculation)

{kind=link}

Valuation Is Too Expensive

The valuation at which HEICO stock is currently trading seems expensive if we look at many well-known valuation metrics. A PE ratio of 50 is extremely high. From the chart we can see that the average PE ratio has risen sharply over the past decade. The valuation was favorable in 2020. Then, the stock price has skyrocketed, making the valuation no longer attractive. During this high interest environment, the high valuation could not be justified.

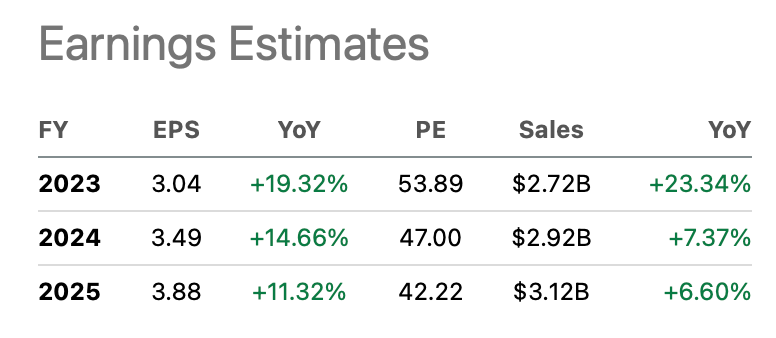

The near-term future looks bright, as 11 analysts expect strong revenue growth of high single-digits and non-GAAP EPS growth of mid-teens over the next few years. This growth is quite expensive, as the forward PE ratio is 42 in 2025. So currently the stock price seems expensive, but also for the foreseeable future. But we have not included cash and debt in the stock's valuation.

HEICO's earnings estimates (HEI.A ticker page on Seeking Alpha)

{kind=link}

A common measure for including cash and debt in the valuation of a stock is the enterprise value to free cash flow ratio. This ratio calculates market value plus debt minus cash and compares it to the company's free cash flow. With a ratio of 43, this also seems like an expensive buy.

In short, HEICO is growing rapidly, but its stock valuation is not realistic compared to today's market. With rising interest rates and a looming recession, I don't think HEICO is a good buy right now. I prefer to wait until the valuation is at market levels.

Conclusion

The strong results for the first quarter of fiscal 2023 show that HEICO is growing rapidly. Organic growth in net sales was strong at 25% and operating income was up 27%. HEICO is operating in a growing market as the need for defense spending increases due to increased global threats. The overall aerospace and defense market is expected to grow at a CAGR of 5.9% through 2027.

Many analysts expect strong profit and revenue growth averaging about 10% to 15% growth a year for the next few years. HEICO's profit margin is high at 15%, but it pays out only a small portion of its profits to shareholders in the form of dividends. The dividend yield is currently 0.12%, and the dividend is expected to double next year. Looking at stock valuation, HEICO is expensively valued based on its PE ratio and enterprise value to free cash flow. Since many analysts expect strong earnings growth, the PE ratio will fall from 54 today to 42 in fiscal 2025 at the current price level. The inverse of the PE ratio of 54 is the company's earnings yield, which is currently 1.9%. This ratio is still far too low, given that the yield on 10-year government bonds is currently 3.4%. Therefore, I would wait for a better buying opportunity when the share price has corrected from this high price level.

For further details see:

HEICO: Wait For A Better Buying Opportunity