HLBZF - Heidelberg Materials: European Value Play In The Building Materials Sector

Summary

- Heidelberg Materials is one of the world's largest producers of building materials, including cement, aggregates, and concrete.

- Pricing power enabled the company to offset rising energy prices.

- Price hikes might stay while energy prices fall back to levels of the past.

- Even with zero growth, my DCF valuation indicates that Heidelberg Materials is clearly undervalued at the current price.

Introduction

This will be an article that is pretty different from my past articles. While I normally try to focus on high-quality, compounding companies with high Returns on Capital Employed (ROCE) and a wide moat, Heidelberg Materials ( OTCPK:HDELY / OTCPK:HLBZF ) is a value play that doesn't meet all of these criteria and not a company I would just buy and hold forever.

However, as an investor and contributor based in Germany, I feel I have the duty to write an article about the only German company I am currently holding.

Regarding the structure of this article, I won't go over the quality of the business. I don't think this will add any value because as I already said Heidelberg Materials is not a quality compounder that I want to hold forever. I will rather start by giving a short introduction to the company followed by my investment case which focuses on pricing power, energy prices, undervaluation and the possibility of high shareholder returns through dividends and share repurchases.

So let's get started.

Company Overview

First of all, the Seeking Alpha tickers still state the company's name as HeidelbergCement AG. In September 2022 , the company changed its name to Heidelberg Materials to detach its name from the cement business because of the link to carbon emissions. Heidelberg Materials wants to link the company name to a more sustainable image.

Heidelberg Materials is one of the world's largest producers of building materials including cement, aggregates and concrete. Core activities include producing and marketing these products. The company operates in over 50 countries and 5 continents. It operates 600 quarries, 140 cement plants and 1,475 cement production facilities.

Investment Case

I want to start off with the moat Heidelberg Materials has. I normally argue that the main indicator for a wide moat is a high ROCE. As the chart below shows this is not the case here:

The ROCE didn't even surpass 10% over the past decade, which indicates that this is a low-quality business.

Pricing Power

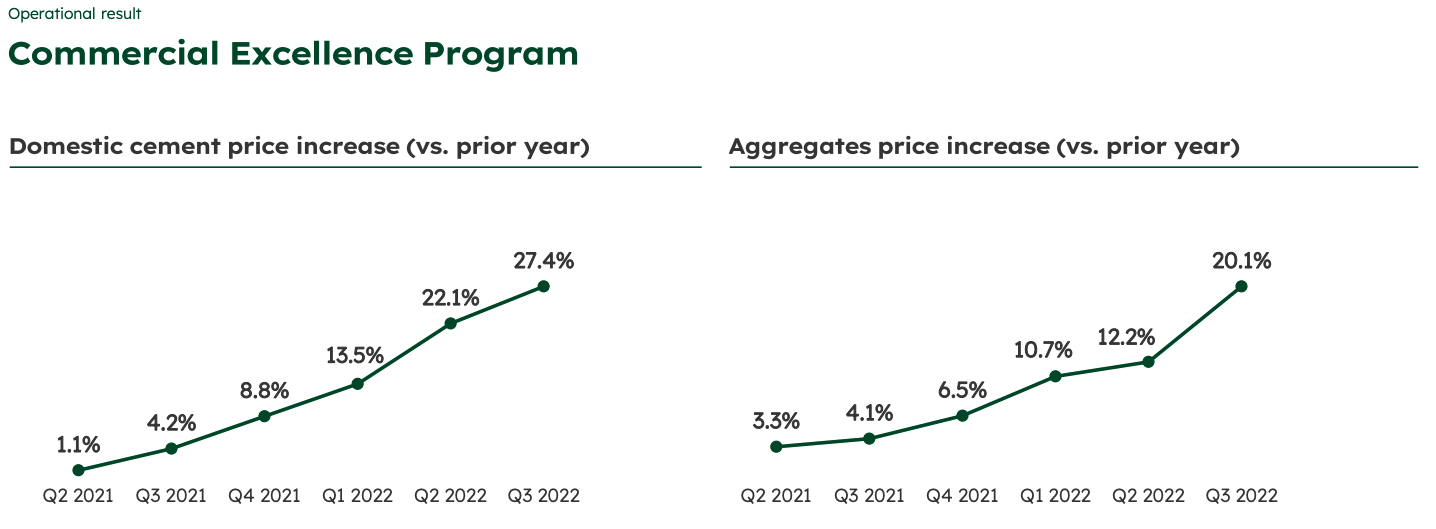

In my opinion, the case for Heidelberg Materials is different because in this case, we need to look at the real-life business. This business is very asset-heavy and capital-intensive, rightfully leading to poor ROCE numbers. The moat lies in the high switching costs between suppliers. The transportation of cement and aggregates is pretty expensive so customers will always focus on the plants that are the closest to the project being built at that moment. Paying a higher price for the materials more than offsets the saving in transportation costs. This leaves Heidelberg Materials with high pricing power, as can be seen in the chart below, showing the price increases over the past few quarters:

{kind=link}

Cement and aggregate prices have been raised by up to 27% and 20% respectively, more than keeping up with inflation.

Declining interest expenses

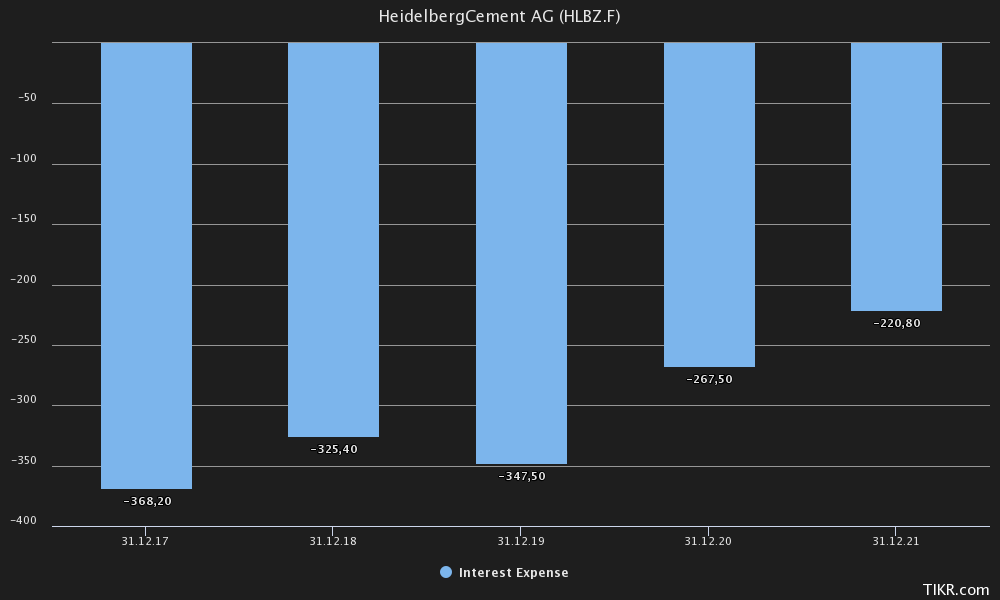

Another part of my investment case is the fact that the company managed to reduce debt and interest expenses by a lot over the past few years, as can be seen in the chart below:

{kind=link}

Interest expenses declined from €368.2 million in FY2017 to €220.8 million in FY2021, a 40% decline. For the trailing twelve months ((TTM)), interest expense stands at €196.5 million, another 10% drop from FY2021 levels. According to the investor relations website, there are only €229 million in debt maturities for FY2023 . While interest rates on new debt may rise in the future because the European Central Bank is raising rates, this leaves some more time to deal with this problem. Maybe rates will already start going down by the time the company is in need of refinancing. Only time will tell.

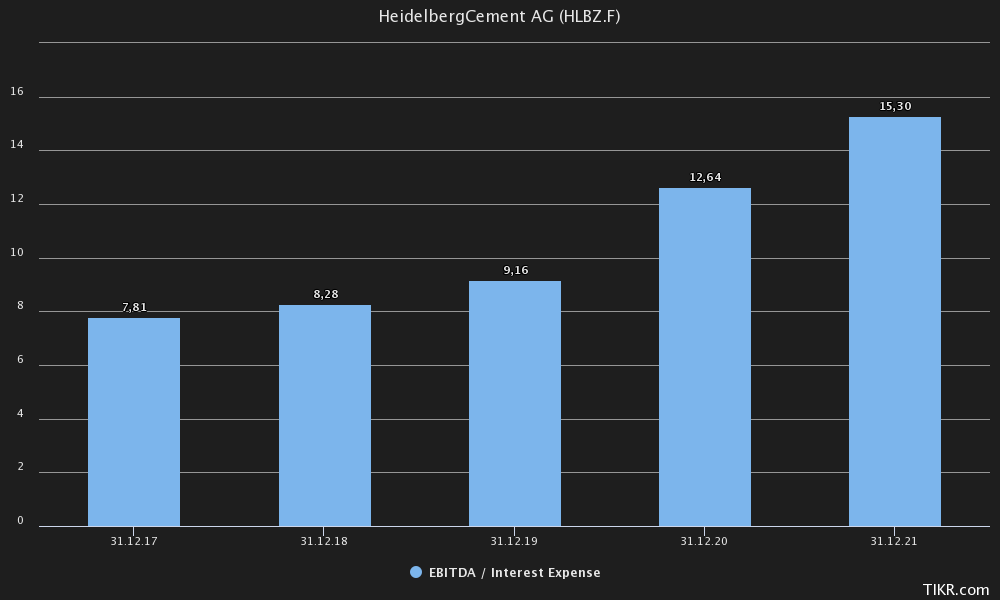

The decline in interest expense also shows in the interest cover ratio (EBITDA divided by interest expense), as is shown in the chart below:

{kind=link}

Interest cover nearly doubled over the past few years, a very good sign for the financial stability of the company.

Heightened Energy Prices

The production of cement, concrete and aggregates is energy-intensive. This has been a headwind for the company over the past few quarters, as can be seen in the chart below:

Price over cost past few quarters (Company Q3 2022 Trading Update - slide 6)

{kind=link}

This chart has to be looked at in combination with the price increases chart above. Rising energy prices have been a major headwind to the bottom line in Q4 2021 and Q1 2022 where price increases weren't able to offset cost increases from higher energy costs. This reversed from Q2 2022. Here is a chart showing electricity prices for some European countries since the beginning of 2020:

{kind=link}

Prices peaked in the third quarter of FY2022 and declined massively until October only to start rising again towards the end of the year. Now I have to say that Heidelberg Materials doesn't solely rely on energy costs in Europe because they have operations worldwide. However, this paints a picture of the situation in the energy markets. In my opinion, price increases are here to stay while the heightened energy costs are not. This should enable Heidelberg Materials to improve margins once energy prices start to normalize over a longer period of time.

Putting it together

To sum up my Investment Case, I think that the price increases in light of rising energy prices will be permanent while the energy prices won't. Additionally, the declining interest expenses leave more room for the company to pay out cash to shareholders through dividends and share repurchases (I will go over this in the next section).

Valuation

(Author Note: One share on the Frankfurt Stock Exchange equals 5 ADR - OTCPK:HDELY )

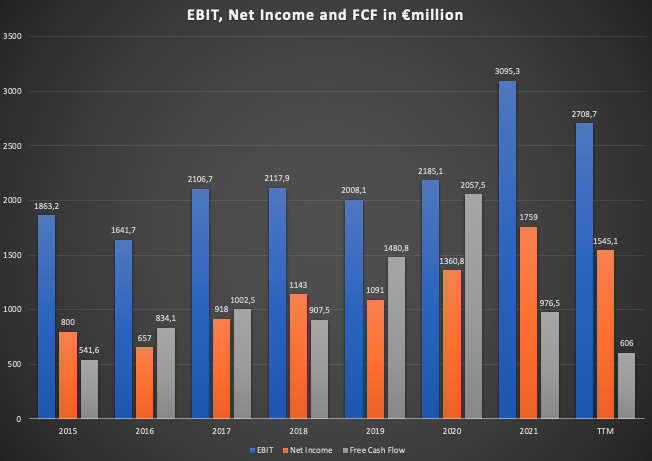

I want to start by giving a quick overview of the main financial metrics over the past few years:

EBIT, Net Income and FCF (Company Reports - compiled by Author)

{kind=link}

There has been an upward trend since FY2015. For the TTM we can see the aforementioned impacts of the cost inflation outpacing price increases. As I outlined above I think this will reverse over the upcoming months when energy prices start to stabilize again.

As I am writing this, the stock price on the Frankfurt stock exchange stands at €62.76 (ADR: $13.41). According to the first half FY2022 report, there are 186,185,619 shares outstanding, resulting in a market capitalization of €11.685 billion ($12.480 billion). With the TTM net income coming in at €1,545 million ($1,650 million), the stock is trading at a P/E of 7.56. By dividing the sum of all the Free Cash Flow [FCF] from the chart above by the sum of the Net Income I get an average cash conversion of close to 90%, so the normalized FCF should be around €1,390 million ($1,485 million), resulting in an FCF-Yield of 11.90%.

Management stated again and again over the past two years that it reached the targeted leverage-ratio of 1.5 to 2 times net debt/EBITDA. This leaves plenty of room to pay dividends and repurchase shares over the upcoming years. The company announced its first share repurchase program ever in July 2021. The program had a volume of €1 billion and was to be executed in three tranches. Two tranches have been finished at this time with a total of 12,230,381 repurchased and canceled shares. The first two tranches already bought back 6% of the market capitalization in the past 1.5 years. The third tranche should be announced after the dust regarding the rising energy prices settles. Additionally, the company paid a dividend of €2.40 in 2022. If the payout remains the same (after considering the 6% reduction in share count) the dividend should rise by at least 6%, resulting in a current dividend yield of around 4%.

The total returns from a company should be the sum of the FCF-Yield and any potential growth. The FCF-Yield alone should be able to provide close to 12% returns, even if the company doesn't grow at all.

DCF-Valuation

By assuming the aforementioned numbers, the normalized FCF per share should be €7.47 (€62.76 share price x 11.9% normalized FCF-Yield). I will just assume zero growth into perpetuity and a 10% discount rate. Here are the numbers:

DCF with zero growth (moneychimp.com)

The current value per share in the no-growth scenario would be €74.70 per share ($15.96 per ADR), representing 19% upside potential.

Now let's assume the company manages to grow in line with the targeted inflation of 2% per year, everything else equal:

DCF with 2% growth (moneychimp.com)

In this scenario, the stock should be worth around € 95 per share ($20.30 per ADR), representing around 50% upside potential.

In conclusion, Heidelberg Materials seems to be undervalued at the current price.

Risks

In my opinion, there are two major risks to my thesis:

(1) I think that price increases will stay while the rising energy prices will fall back to levels of the past. Energy prices have fallen dramatically in the 3rd quarter of FY2022 but started to rise again towards the end of the year. It remains to be seen if energy prices will stay at higher levels as a "new normal", limiting further margin potential from the cost side in the future.

As for the price increases, the high amount of increases in such a short period might limit Heidelberg Materials' ability to raise prices much further over the next few years. This could also be a headwind to the bottom line because labor costs might outpace possible further price increases in the near future.

(2) While I think the company will remain on track and achieve at least zero growth, the possibility of declining earnings can't be ruled out. According to Investor Relations, Consensus for FY2023 predicts a net income of €1,348 million and FCF of €1,434. This would be a 10% decline in net income from FY2022 estimate levels. This compression in net profits might also be a result of higher refinancing costs in the future as I stated earlier.

Conclusion

Heidelberg Materials is the only stock of a German company I am holding at the moment. Contrary to my usual investment strategy this is a value play and I don't plan on holding the stock forever. My DCF valuation shows that even in a scenario of zero growth, there is around a 20% upside from current prices. I think that zero growth is quite pessimistic. In my opinion, the stock should be worth somewhere between €80-90 per share ($17-19 per ADR). While waiting for my thesis to play out, I am getting a dividend yield of around 4% (paid once per year in May). I would probably start thinking about selling once the stock reaches €80 per share ($17 per ADR).

I rate Heidelberg Materials a buy at the current price. Investors should keep in mind though that this is not a buy-and-hold forever stock. Once the thesis plays out and the company is fairly valued, investors should consider selling because this is not a quality compounder you can hold forever and expect exceptional returns.

For further details see:

Heidelberg Materials: European Value Play In The Building Materials Sector