HLBZF - Heidelberg Materials: Might Be Expensive Despite The Upside

2023-10-26 06:44:01 ET

Summary

- Heidelberg Materials AG has experienced a decline in share price and performance since the last article review.

- The company has shown positive operational performance and sustainability progress, but faces challenges with contextual valuation and CO2 impacts.

- I suggest that Holcim is a better investment option compared to Heidelberg Materials AG.

Dear readers/followers,

I last reviewed Heidelberg Materials AG ( HDELY ) a few months back in April of 2023. This article is an update you can find here . This, as such, is an update on the company. While Heidelberg Materials, formerly Heidelberg Cement, is a solid company, it's also very cyclical, and in my last article, I made it clear that I was starting to rotate the shares I held. My final shares, beyond a watchlist position, were rotated when the company was close to €80/share, and it reached what I considered to be the apex of my thesis for the time being.

The price action following this decision to rotate shows that, as I see it, this was the "right decision" for the short-term, because Heidelberg Materials has started cycling "down" again. The company is now at a sub-€70 share price, with this RoR.

Seeking Alpha Heidelberg materials (Seeking Alpha)

So, as you can see, the company has done pretty sub-par since my last article. I recently updated on Holcim ( HCMLY ) - and now I'm going to show you why I consider Holcim the better choice compared to Heidelberg Materials AG.

Heidelberg Materials - Plenty to like fundamentally, but some issues with the contextual valuation

Heidelberg Materials remains a very solid company, despite me having sold all but a few of my shares in the business. We have a very strong overall operational performance in the last reported period as well, in this case, the 2Q23 with the 3Q23 looming fairly close here.

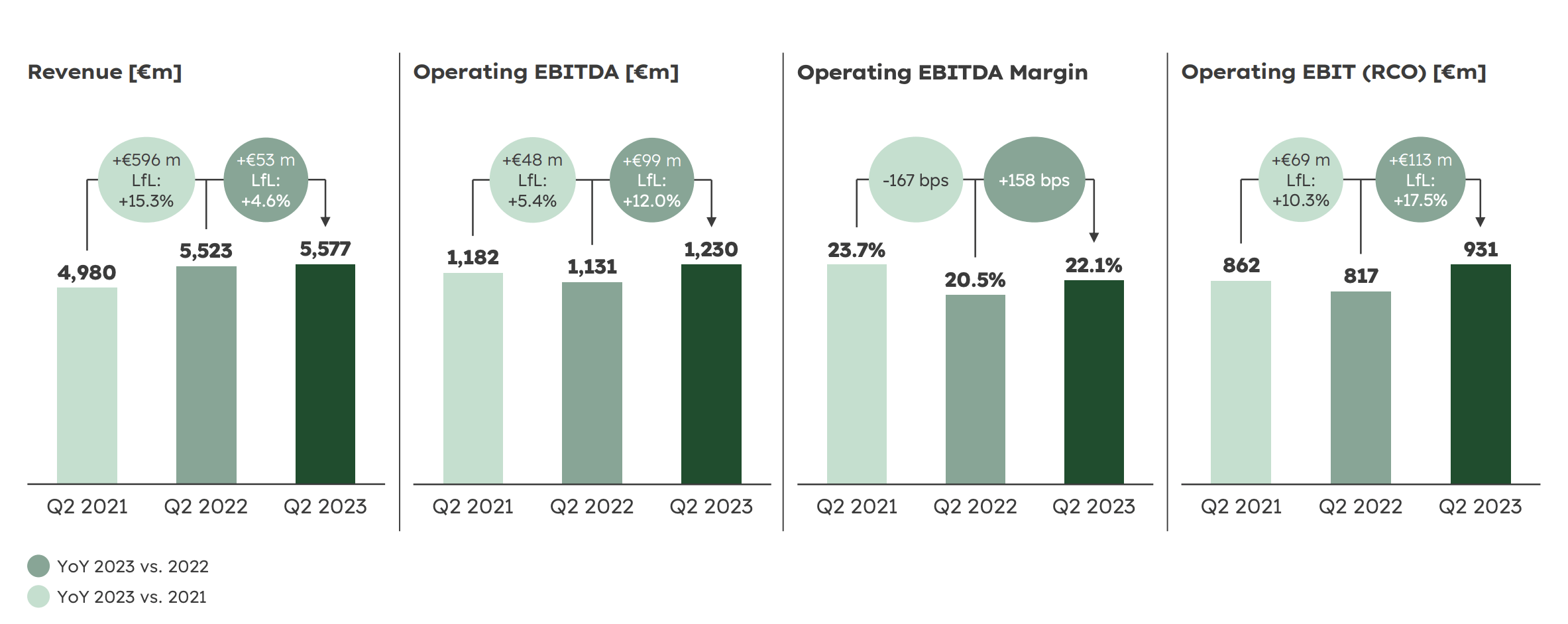

During 2Q23, Heidelberg Materials saw some of the similar trends as we saw in competitors, like Holcim, despite that some of their geographical foci are somewhat different. Revenue for Heidelberg materials was up 5% - but EBITDA was out 12%, with RCO up as much as 18%.

Why?

Positive price-over-cost movements continue to offset and compensate for the volume pressure the company is feeling, which led to significant margin improvement not just in one region, but in all of the company's operating regions. The company even, and I don't particularly like this given the valuation, began a share buyback from its €1B share program, buying back around €300M at what I consider being not that great value, unfortunately. I also expect that this has had to do with what has kept the company's valuation up overall. ( Source )

Much like with Holcim, the company's sustainability targets are actually progressing well. Every KPI in terms of ESG is actually on track, and the clinker input rate reduction is solid as well. Heidelberg is also putting more and more alternative fuels to work.

Aside from the positives from its share buyback program, if it can be called that, the company is also likely being supported by a further-upgraded outlook - much like with Holcim. Heidelberg Materials now expects an RCO of upwards of €2.9B, and this is an improvement of over €300M for the year on the top-end guidance range for the 2023E RCO.

Here is the operational overview, as it came in for the last quarter.

Heidelberg Materials iR (Heidelberg Materials iR)

{kind=link}

The improvement was purely a product of price-over-cost, given a net volume decline of around €139 during the quarter. Improvements echo the trends seen by Holcim, with NA-segment improvements and excellent margin development despite weakness in residential on the continent. The order books, again much like its competitors, remain very well-filled. Even Europe showed very positive trends, though this was not due to volume trends, but due to operational improvements in RCO. The company showed significant margin growth despite a challenging environment - though not because of volume. ( Source )

What this means, because it's not based on volume, is that if pricing pressure starts to really ramp up, there will be a "double" sort of decline, given that we can't guarantee or forecast a ramp-up in volume just because prices go down. The company's growth regions, meaning in this case Africa and the Middle East, are so-so, but this was mostly due to a very difficult comp due to outperformance in the YoY period.

Overall, it's fair to say that Heidelberg Materials showed significant improvement across all KPIs that matter.

Heidelberg Materials IR (Heidelberg Materials IR)

{kind=link}

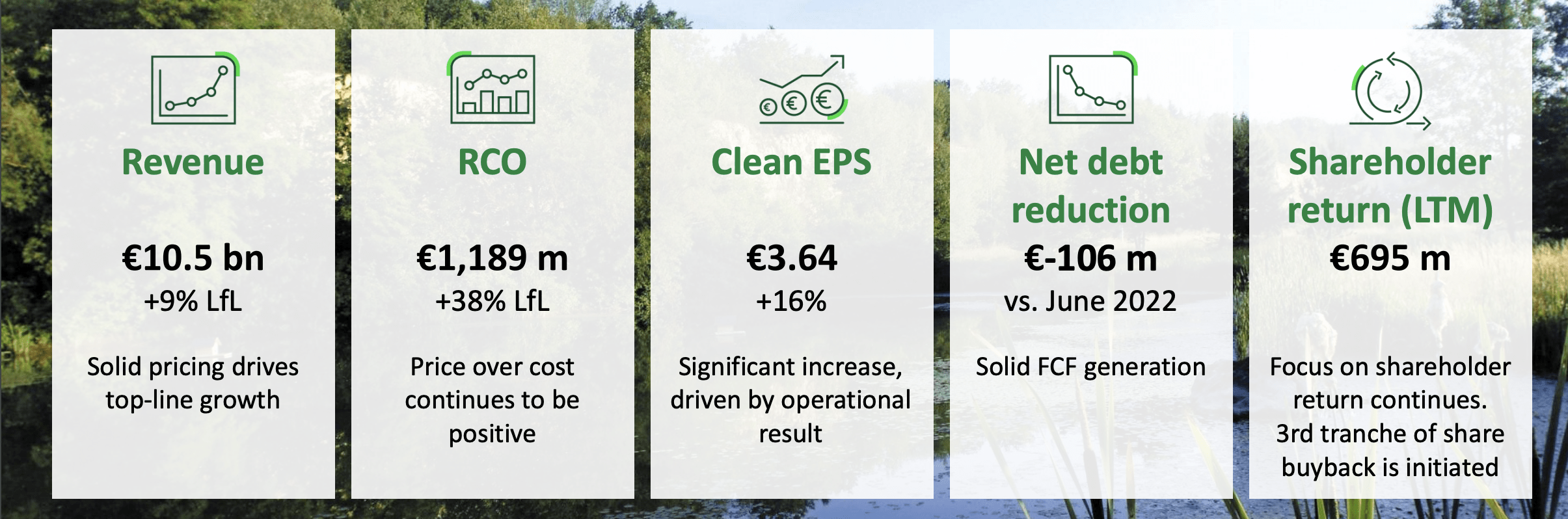

The adjusted EPS increase especially is something, as I see it, to note here, as is the company's increase in FCF with an FCF conversion of 37.2%, an improvement of 1,645 bps. This had to do with seasonal build-up, given construction activity trends, as well as WC improvements. ( Source )

Heidelberg Materials is also showcasing its first decarbonized cement plant in Germany, which has a carbon capture capacity of 700kt Co2 per annum starting in 2029 when the plant opens. This project works with fuel substitutes and other measures, which enables the company to offer fully decarbonized cement and clinker products.

Funding for this was enabled by the EU Innovation Fund, supporting flagship projects such as this one.

The current business outlook is a positive one. The company expects revenue growth, and good RCO improvements without seeing over-the-top increases in CapEx with an ROIC of about 9%, and a leverage that's likely to remain within the target corridor of 1.5x to 2x.

The problem with Heidelberg Materials isn't that it has bad debt, a bad balance sheet, bad earnings, or significant geographical exposures or risks. All of these things are solid. The dividend yield is good, and the stability here is good as well. Revenue is growing, operating margin is going up - on that front, all is "good". That has never been the problem, or why I consider Holcim to be the superior investment at this time.

The problem that I see here is that once we look at the actual producing assets for the company, inclusive especially of the legacy assets acquired in the last M&A, these are assets that are far more unfavorable than assets worked by Holcim or other players from an ESG/Co2 perspective. I've covered extensively before that Heidelberg Materials is more likely than any of its near-term competitors to see these impacts, and this means that the company is deserving of discounting to its peers - and this discount is something that I'll stick to in this article as well.

While the company can indeed manage an 8-9% ROIC, the cost of capital has also gone up since my last article, and definitely, since 2021, which means that the company is currently calculated to be at 0-0.5% on an ROIC - WACC. However, out of all the concrete/aggregate/materials companies in this sector that I offer coverage on, I would say that Heidelberg Materials is one of the most impacted businesses by these trends, and therefore the one deserving not to be bought at levels that we buy companies like, say, Holcim.

Heidelberg Materials Valuation - The upside is now contextually lower than I might like

In my last article, I actually called this company a "BUY" with undervaluation still, despite making it abundantly clear that I was rotating my stake at the time, and over the next few weeks and months. As I am updating my thesis for HeidelbergCement, I find it difficult to come up with concrete (pardon the pun) arguments for why the company is a "bad" investment. Because, frankly, it's not.

The company is sub-par on a few levels, which I consider to be enough for the argument. Holcim has a better yield, as well as a better credit rating. Heidelberg Materials is at BBB. It yields less than 4% despite the recent drop, and it typically trades at 11-12x P/E, with a current P/E of 7x. That alone should show you why I still maintain my "BUY" rating because, from a fundamental valuation perspective, this company still has an upside.

However, based on the Co2 impacts and the instability of the company's end markets, as proven by its history, as well as the failure to provide forecastable earnings based on a 60%+ forecast miss ratio even with only a 10% margin of error (Source: F.A.S.T Graphs), I will say the following.

I do not consider it completely unlike that until 2024-2026E, we'll see Heidelberg Materials Trade at a 6-8x P/E based on the headwinds that I mention here. And if we use let's say a 7x P/E for the forecast, consider a 5% EPS growth rate which I believe is a fair average based both on analysts and other forecasts (Source: S&P Global), then your eventual upside in this investment would be less than 10% per year, and that's inclusive of the company's dividend.

Sure, you can forecast at 10x-11x. That would give you over 20%+ annualized, but I also want to make it clear to you that this implies a share price of €104/share. The company has not traded that high for a very, very long time, and I don't necessarily believe this macro to be an environment where such an upside is likely, even if it doesn't necessarily denote a premium for the company.

S&P Global averages for Heidelberg Materials currently begin at €70/share, which is laughable - because when I bought the company, some believed it to be worth around €38/share. The high end now is €104 - so keep that in mind, with an average of €83/share. The stance from 18 analysts is 11 at either a "BUY" or an "outperform".

I don't necessarily disagree with the sentiment, but I believe that Holcim, on every level, offers you a more conservative and safer upside than Heidelberg Materials.

For that reason, the only reason to buy HDELY here is if you already have full positions in Holcim and for some reason "must" have more European concrete.

Then, this one is a "BUY".

Here is my thesis for the company.

Thesis

- Heidelberg Materials is still one of the better cement/aggregate plays on the planet from a fundamental basis, but a 40-50% move in the positive direction has taken much of the valuation-related shine from the business, coupled with the current macro.

- Due to worsening macro outlooks, rate increases, and the company's asset characteristics in this context, I am lowering the target to €75/share. Most analysts I follow have the company at €65-€80/share. In the context of the market, despite my positive rating for the business, you are buying Heidelberg materials at somewhat of a premium from a 12-month perspective - just be aware of this.

- I am no longer calling Heidelberg Materials a potential trim target below €70/share, but once it goes above that again, I'd be very careful. Only those really wanting the exposure and willing to ride through the lows (because lows will come again, I have no doubt), should consider the "BUY" here.

Remember, I'm all about:

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

Heidelberg stock is still a "BUY" but read my thesis to understand why I am no longer as interested in going further at this time.

For further details see:

Heidelberg Materials: Might Be Expensive Despite The Upside