HDELY - Heidelberg Materials: Solid Q1 But Headwinds In Real Estate

2023-05-11 18:35:22 ET

Summary

- Portfolio reshaping continues with an ongoing upside on the circular economy.

- The company announced new acquisitions as well as a DPS increase.

- 2023 outlook upgraded with a higher RCO.

Here at the Lab, in conjunction with the latest Q1 update, we decided to follow up on HeidelbergCement (now called Heidelberg Materials, HLBZF , HDELY ). Last time, we provided a comps analysis with Holcim and since early March, Heidelberg is up by almost 8%. In detail, after years of holding, here at the Lab, we are now more favorable on a Holcim investment and this was based on: 1) better portfolio improvements thanks to the roofing division and our Multiple Arbitrage Opportunity analysis; 2) a lower net debt; and 3) a new buyback announcement with a higher DPS increase. Even if we were more cautious about Heidelberg's estimate, our buy case was supported by 2023's positive guidance and despite a higher debt, we reiterated our €70 stock price buy rating ($14.5 in ADR).

Mare Evidence Lab's previous publication

{kind=link}

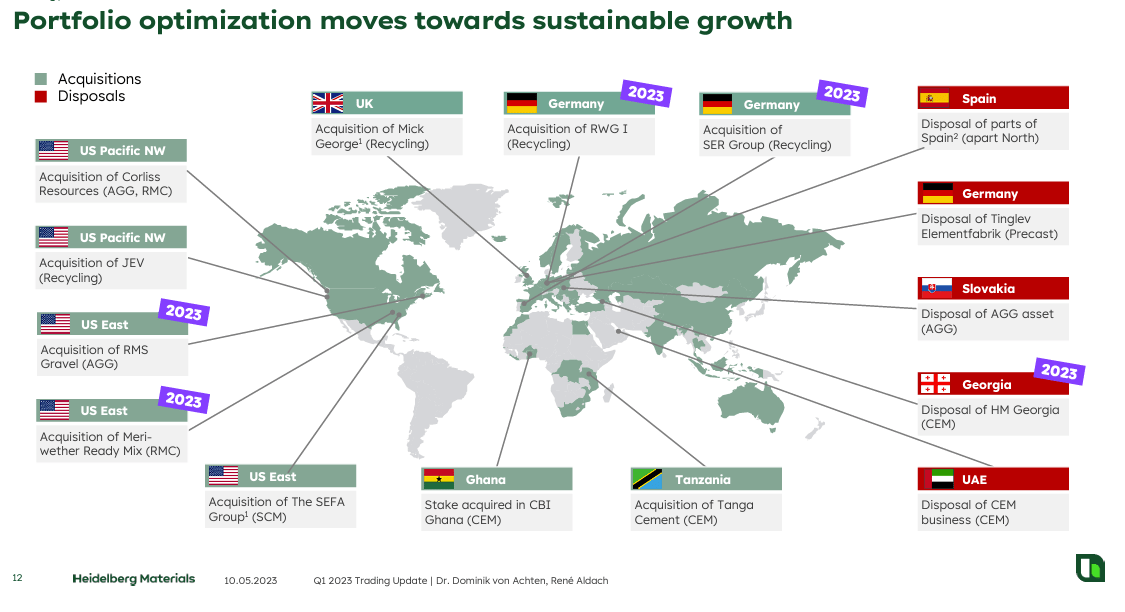

Looking at the latest developments, it felt like our thoughts were executed. Starting with Heidelberg Materials' portfolio reshaping, the company announced:

- The acquisition of the largest fly ash recycling company in the USA. The company entered into SEFA Group , a business that reuses fly ash from energy production in alternative outputs such as composite cement. This aims to strengthen Heidelberg Materials' circular value chain. In the Q1 update, the RMS Gravel Inc. deal was announced . This is part of Heidelberg's strategic plan to optimize the current portfolio. As a reminder, in April 2022, the company acquired Meriwether Ready Mix, a ready-mixed producer in the commercial and residential Metropolitan Atlanta area. In October 2022, JEV Recycling was also finalized, this company is a recycler in the Greater Seattle area that supports our point 1). These latest deals contribute to the main company's goal to provide circular alternatives for 1/2 of concrete production capacity by 2030. In Fig 1, it is evident how the company is becoming a material business solution and is exiting its traditional business and disposing of CEM business. In addition, Linde ( buy target by Mare Evidence Lab ) and Heidelberg will build the world's first large-scale CCU plan in a cement facility in Germany;

- Regarding the dividend payment, in the FY 2022 results, the company's dividend was left unchanged on a year-to-year basis. However, in March-end, the company announced a DPS increase of 8% to €2.60 from €2.40;

- Concerning the net debt evolution, Heidelberg left its 2023 guidance unchanged, confirming a leverage between 1.5x and 2.0x. There was no disclosure on the cash flow generation, but we are estimating a net debt/EBITDA in line with Q4 2022 at 1.5x.

Heidelberg Materials portfolio optimisation

{kind=link}

Q1 update

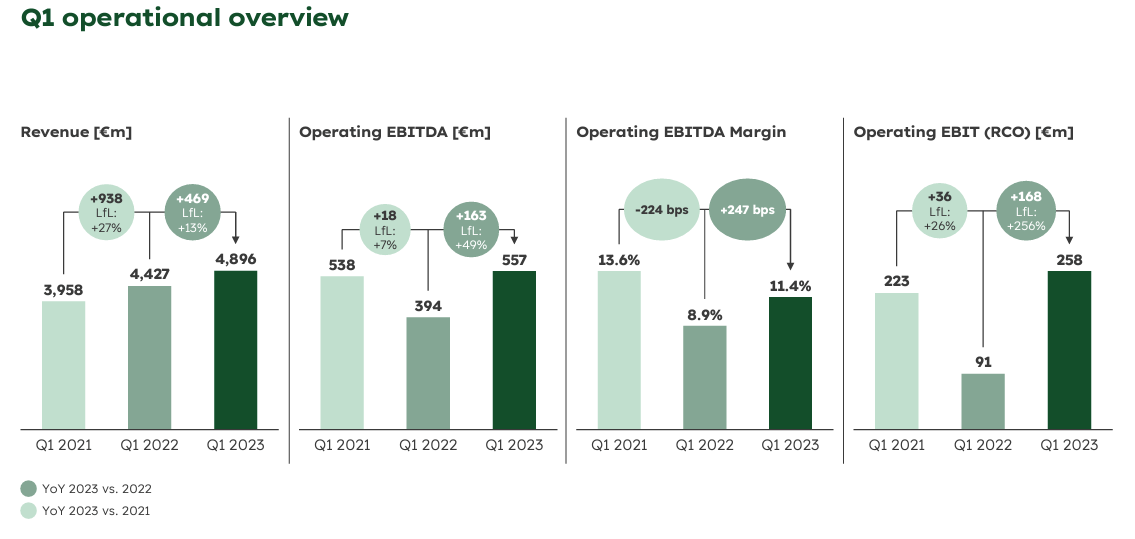

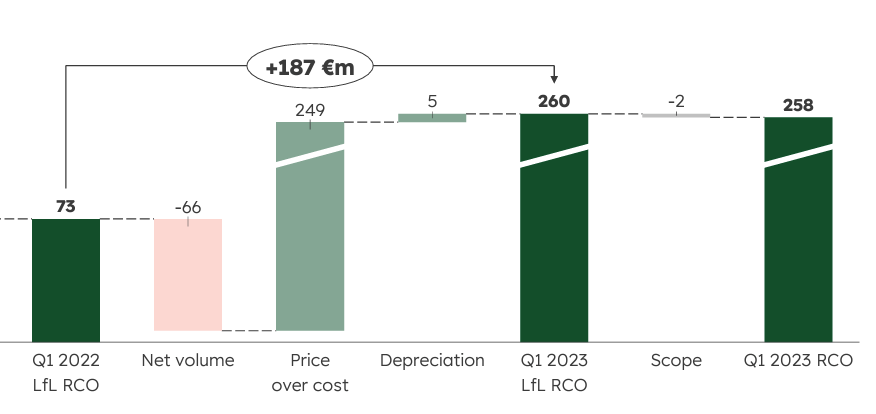

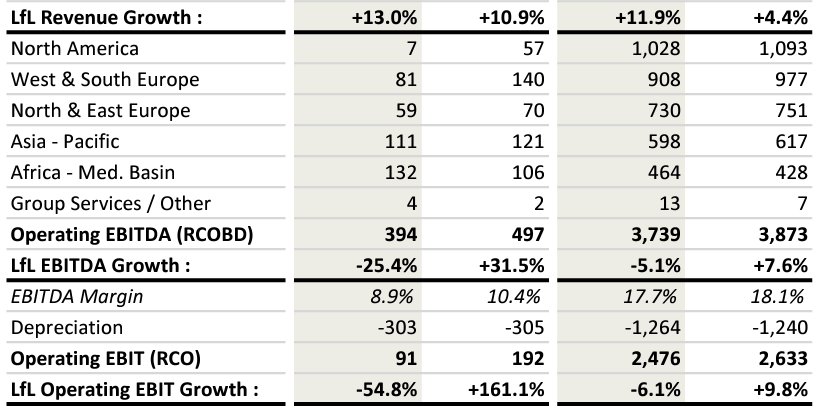

In Q1, as expected, volumes declined and this was the result of the economic downturn. The US and the EU construction sector recorded lower volumes growth in residential demand. This was due to higher interest rates and raw material inflationary pressure. We pointed out that geopolitical events in Ukraine and sticky inflation are weighing on the sector's construction demand. In detail, the company delivered top-line sales of plus 13% to almost €4.9 billion (Fig 2). Despite a negative FX evolution, Heidelberg was able to increase the price, confirming the positive trajectory recorded already in Q4 2022. With lower volumes, the company increased price over cost, with a supportive effect quantified in €187 million (Fig 3). Going down to the P&L analysis, there was a strong improvement in profitability results. Despite energy costs remaining elevated, all geographical areas positively contribute to the group's net results. EBITDA increased by €163 million and was up by 41.3% to €557 million. Cross-checking the Wall Street analyst expectation, the company managed to beat all the main ratios (Fig 4).

Fig 2

Heidelberg Q1 Financials in a Snap

{kind=link}

Fig 3

Heidelberg price/cost vs volume

{kind=link}

{kind=link}

Conclusion and Valuation

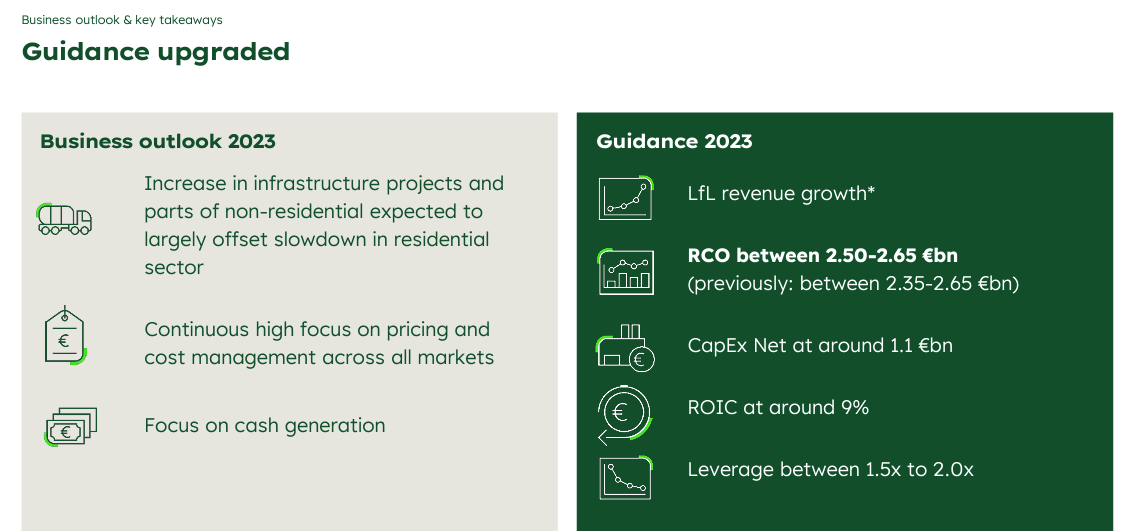

Thanks to a good start to the year, Heidelberg Materials decided to increase its 2023 guidance. In detail, RCO is now expected to be in a range between €2.50 billion and €2.65 billion (it was previously set between €2.35 billion and €2.65 billion). Looking at the consensus, we do not believe that Heidelberg will deleverage by €700 million on a yearly basis, and despite a better outlook, here at the Lab, we believe that the construction sector is going to be beaten down . In addition, the company reached our target price of €70 per share ($14.5 in ADR). Therefore, continuing to value Heidelberg with a 5.5x rolling forward EBITDA, we moved our rating to an equal weight.

Heidelberg Materials 2023 guidance

{kind=link}

For further details see:

Heidelberg Materials: Solid Q1, But Headwinds In Real Estate