HDELY - Heidelberg Materials: Time To Take Profits (Rating Downgrade)

2023-06-23 12:37:02 ET

Summary

- I initiated coverage on Heidelberg Materials with a buy rating in February 2023 due to its undervaluation, trading at €62.76 per share with a P/E of 7.56.

- The stock should have been worth around €75 per share at the low end and €95 at the high end.

- Heidelberg Materials is not a buy-and-hold forever stock due to poor returns on capital employed (ROCE) indicating that it is fundamentally a low-quality business.

- Since my initial thesis played out as expected, I decided to take profits a bit below my estimated low-end fair value and rate the stock a "sell".

Introduction

On February 12, 2023, I published my first article on Heidelberg Materials ( HDELY ) ( HLBZF ) and initiated coverage with a buy rating. My investment case was simple: While not a high-quality compounder, Heidelberg Materials was too cheap to ignore. The company was trading at €62.76 per share (on the Frankfurt stock exchange) for a P/E of 7.56. Even when assuming zero growth, the stock should have been worth around €75 per share. Assuming 2% growth in line with the targeted inflation, the stock should have been worth around €95.

I concluded that Heidelberg Materials was undervalued and gave it a buy rating while noting that this is not a buy-and-hold forever kind of company due to poor returns on capital employed (ROCE) indicating that this is a low-quality business. Here are my last words from my initial article:

I rate Heidelberg Materials a buy at the current price. Investors should keep in mind though that this is not a buy-and-hold forever stock. Once the thesis plays out and the company is fairly valued, investors should consider selling because this is not a quality compounder you can hold forever and expect exceptional returns.

Source: Initial article

In this article, I want to give an update on what has happened since I started coverage, valuation and what I have been doing with my shares.

Initial thesis review

Besides the fact that I thought Heidelberg Materials was undervalued, my fundamental thesis was based on two factors and I want to give an update on these first:

(1) The company had shown tremendous pricing power over the past few quarters. Here is what I wrote regarding pricing power in my initial article:

The transportation of cement and aggregates is pretty expensive so customers will always focus on the plants that are the closest to the project being built at that moment. Paying a higher price for the materials more than offsets the saving in transportation costs. This leaves Heidelberg Materials with high pricing power...

Source: Initial article

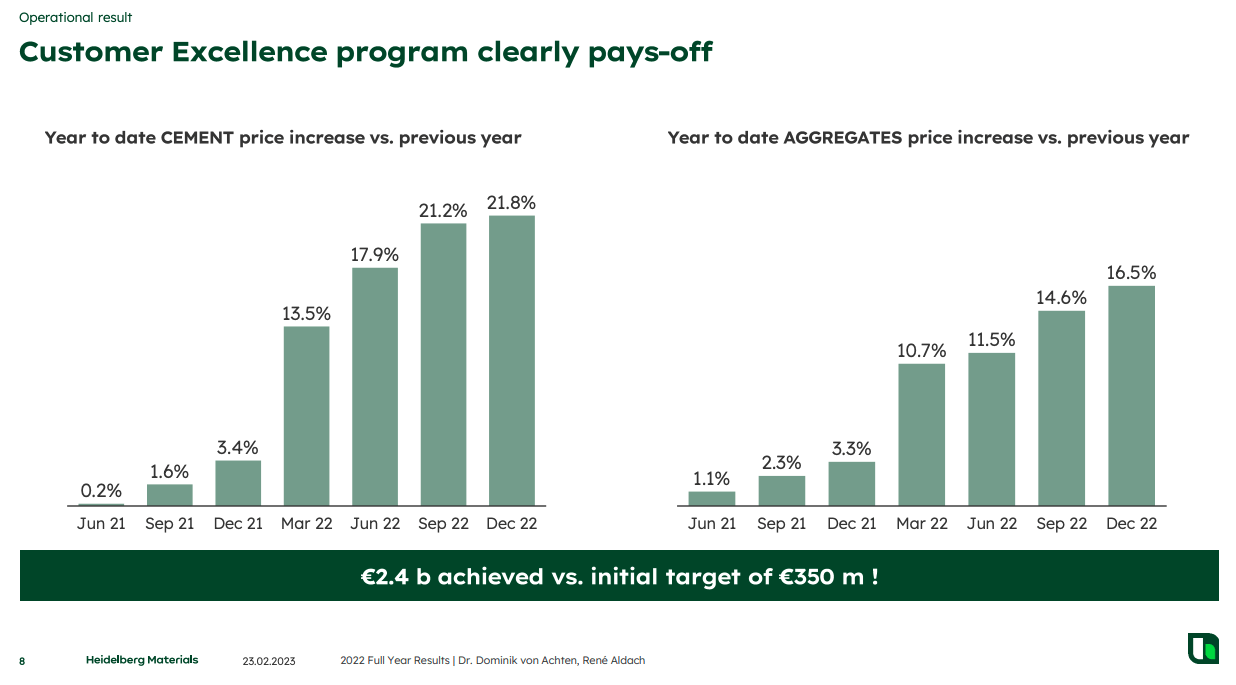

Here is the updated slide from the FY2022 results presentation :

{kind=link}

My guess was (and still is) that these price increases will be permanent and not just a temporary effect of higher energy prices. The company didn't update this slide in its last Q1 2023 trading update. This is a sign that price increases probably stopped due to the decline in energy prices. Declining energy prices probably took away the main argument for price increases. This leads me to the second factor: Energy prices.

(2) In Q4 2021 and Q1 2022, rising energy costs more than offset the aforementioned price increases. This turned around from Q2 2022, so price increases and rising energy costs were nearly breaking even. I argued that if price increases are permanent, the company's margins should improve by a lot once energy prices reverse to a more reasonable level because the input costs (energy) go down while revenue (pricing) stays the same.

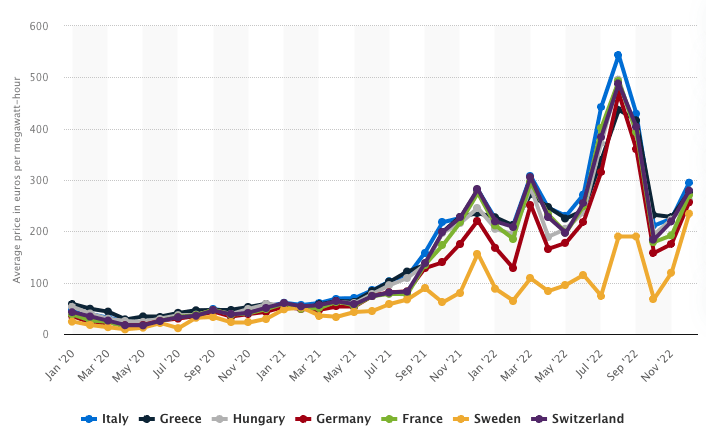

Here is the electricity price chart I used in my initial article (for reference):

{kind=link}

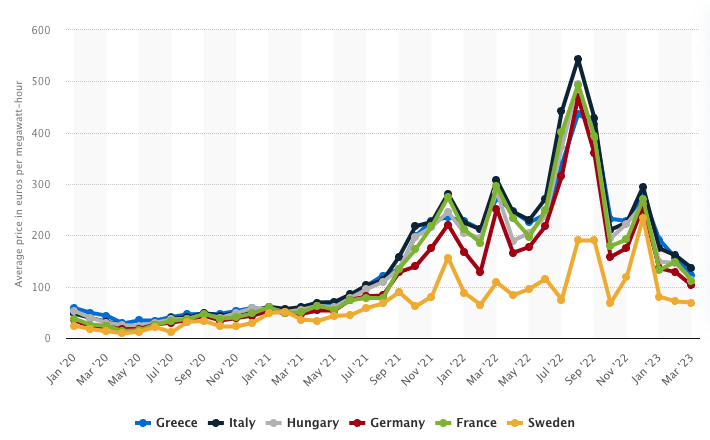

And here is the updated version :

{kind=link}

We can see that electricity prices declined sharply after the second peak in December 2022. With prices staying the same, this should result in margin improvement for FY2023 and ultimately be rewarded with a rising share price.

This is exactly what happened, as can be seen in the following snippet from my initial article:

Performance since last article (Seeking Alpha)

The share price only went up after a temporary low in October 2022 (just a few weeks after the electricity price peak in August 2022). The stock outperformed the S&P 500 by a wide margin since my first coverage (including a dividend of €2.60 paid in May).

This is where I have to come back to my statement from above. Once the thesis plays out and the company is fairly valued, investors should consider selling because this is not a quality compounder you can hold forever and expect exceptional returns. This leads me to the next part of this article: Valuation.

Valuation

(Author Note: One share on the Frankfurt Stock Exchange equals 5 ADR - OTCPK:HDELY )

There are 186,185,619 shares outstanding at the moment. The price on the Frankfurt stock exchange currently hovers around €72 per share (ADR: $15.65) so the market capitalization amounts to around €13.4 billion ($14.6 billion). With FY2022 net income of €1,597 million ($1,735 million), the P/E stands at 8.4. The cash conversion rate is quite cyclical (as is to be expected by a company like this) but averages around 90 to 100 percent over the past seven years. I will just assume an average cash conversion of 90% which would put the normalized free cash flow ((FCF)) at around €1,437 million ($1,561 million) or €7.72 per share (ADR: $1.68) so that the FCF yield (on a normalized basis) would stand at around 10.7% at the moment.

If we again assume zero growth into perpetuity with a 10% discount rate, the stock should be fairly valued at €77.20 (ADR: $16.77) or 10 times FCF per share, slightly higher than the current price.

If we assume 2% perpetual growth in line with the inflation target of 2%, the fair value should be around €98 per share (ADR: $21.29) as can be seen in the following screenshot from a simple DCF calculator:

DCF calculation (moneychimp.com)

Do I think that we will see prices like €98? No. Heidelberg Materials is a cyclical business and the low ROCE indicates that it is fundamentally a poor business. A valuation discount is warranted here.

In my last article, I stated that I would start to think about selling at around €80 per share (ADR: $17.38). However, I recently decided to sell my full position at a bit above €73 per share (ADR: $15.86). The stock might still be undervalued and there might still be around 10-15% upside left, but I don't know how long it will take to get there and most importantly (I need to repeat myself here) this is not a buy-and-hold forever stock for me. Hence, I decided to take the profits from the run-up since February.

Conclusion

In my initial article, I argued that Heidelberg Materials was undervalued. My main thesis was that once energy prices start to decline and the market realizes that the price increases over the past few quarters are staying, the stock price should reward this by approaching fair value which should have been €75 per share (ADR: $16.29) at the low end.

Furthermore, I stated that Heidelberg Materials is a temporary value play and that investors should start thinking about selling once the stock approaches fair value.

Energy prices declined since my last article and Heidelberg Materials outperformed the broader market by a wide margin. Since my thesis played out and Heidelberg Materials isn't a long-term buy-and-hold stock for me, I decided to sell my shares at around €73 (ADR: $15.86) and invest those funds into more promising opportunities which I plan to cover over the upcoming weeks.

So I have to rate Heidelberg Materials a "sell" at the current price and will stop covering the company for the foreseeable future. I might write about it again if it becomes clearly undervalued and offers another possibility for a temporary value play.

For further details see:

Heidelberg Materials: Time To Take Profits (Rating Downgrade)