RHI - Heidrick & Struggles: Attractively Valued Cash Cow With Growth Prospects

2023-07-18 11:27:12 ET

Summary

- Heidrick & Struggles International, a leading executive search firm, is a cash cow that has potential to improve profitability and grow.

- The company's consulting business has been a drag on earnings, but its on-demand talent sector shows potential for growth, especially with the acquisition of German company Atreus.

- Despite potential headwinds, Heidrick's strong balance sheet, cash-generative business and attractive valuation could make the stock a profitable investment with a decent dividend yield.

Heidrick & Struggles International ( HSII ) is primarily an executive search company with growing temporary staffing and consulting businesses. Heidrick is focused on the upper end of the market in all of its businesses and is recognized as a leader in the executive search market.

As a capital light business Heidrick enjoys high returns on capital, good margins and excellent cash flows. The company has a strong balance sheet with plenty of cash to go through tougher times. Heidrick has one promising growth business and one to be turned around, which could boost the profitability further. Heidrick pays a modest well-covered dividend. I believe Heidrick is attractively valued historically, relatively and in relation to its earnings power.

Record year behind

Heidrick & Struggles is primarily an executive search firm. The company is hired to find and recruit new members of top management for its clients. Heidrick also has on-demand talent and consulting businesses. Heidrick revenues were approximately $1 billion last year and it employs less than 2200 people.

In 2022 the revenues were split between three segments: Executive search 84%, On-demand talent 8.5% and Consulting 7.5%. Executive search reports its figures also geographically and revenues are split between Americas (68%), Europe (20%) and Asia-Pacific (12%). Both On-demand talent and Consulting were loss-making measured by operating income.

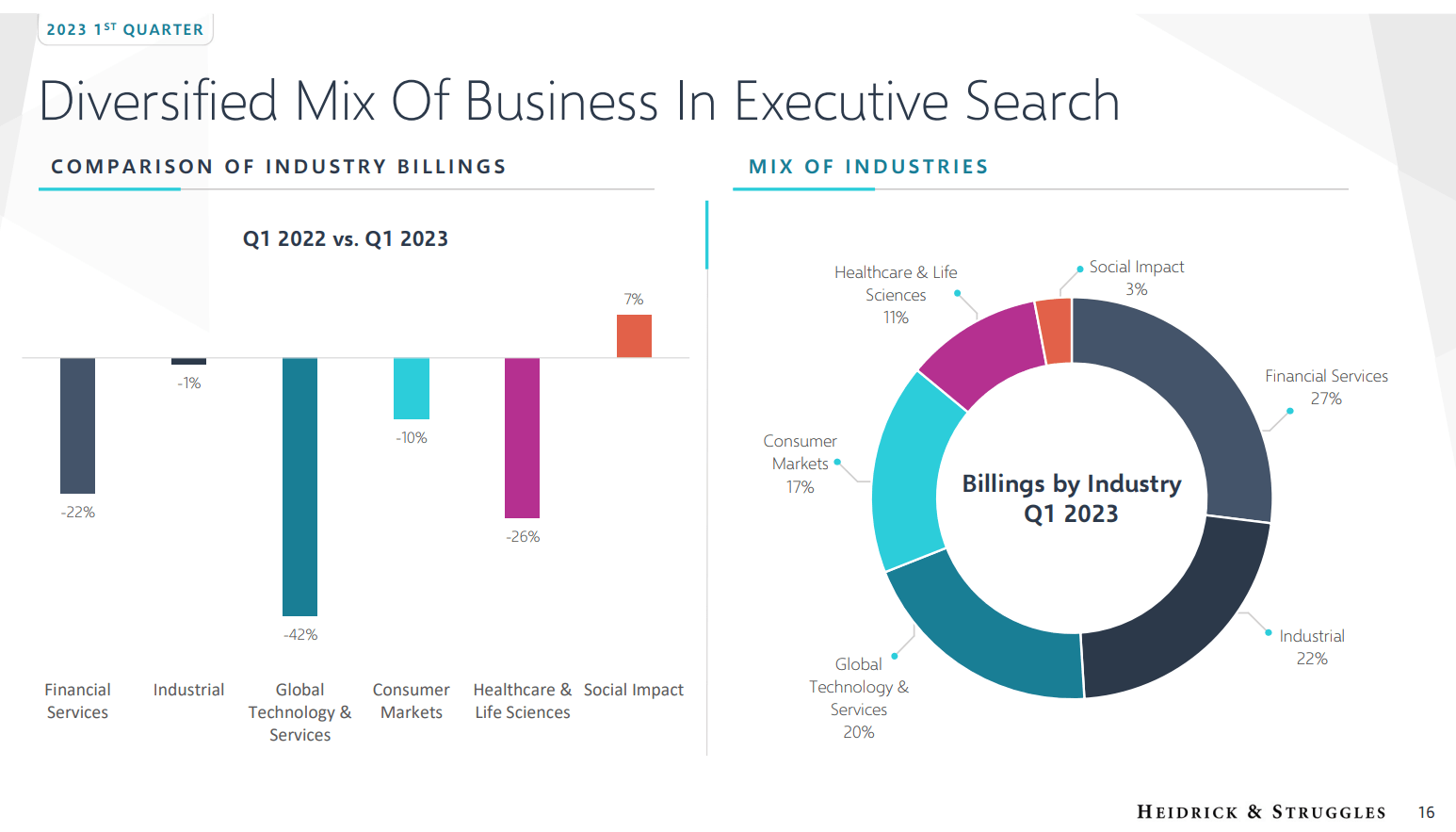

2022 was a record year for the company. After a strong 2021, its revenue increased 14% and net income nearly 10%. In Q1 the positive trend reversed. Both revenues and net income declined 16%. The outcome was mainly due to the negative development in executive search business. In a segment breakdown one can see that the slowdown in the technology sector has hurt Heidrick’s sales the most, which could be a result of over-hiring in the sector.

Q1 was hurt by recruitment slowdown in several sectors. (Q1 presentation)

{kind=link}

Heidrick also spent $20.4 million on R&D to catch up on the digital frontier. The company expects R&D to continue but moderate in the following years. Heidrick is definitely a beneficiary of the work from home trend and it has taken on extra costs to right size its real estate footprint.

Executive search and consulting are relationships and people businesses. Salaries and benefits represent approximately 70% of the company's revenue, which could hurt the company’s profitability if wage growth accelerates. On the other hand company’s revenues would increase as its fees are based on the salaries of the recruited people. One of the key metrics, revenue per employee, has grown favorably over the years.

Strong market position and the large pile of cash

According to Randstad the executive search is a $35 billion market globally. Overall, personnel services is a highly competitive industry where no incumbent can enjoy a true moat in my opinion. The giants such as Manpower, Adecco or Randstad might enjoy some scale advantages, but there are no barriers to entry and consultants can move from a company to the next and take a portion of customers with them.

Heidrick is specialized in the executive search services. According to Forbes and its survey among 5200 recruiters, HR, managers and job seekers, Heidrick is the fourth best executive search firm in the U.S. Two listed competitors made it ahead of Heidrick. Korn Ferry ( KFY ) and Robert Half ( RHI ) took the first and second position in the survey.

Heidrick’s business appears to be cyclical, even if one would think that executives tour around companies independent from cycles. In downturns companies freeze their hiring and people stay put in their old jobs. Both in 2017 and 2020 Heidrick delivered negative net income, but this was primarily a result of goodwill impairments and therefore its free cash flow was positive.

An anecdotal evidence of the excellent profitability of the business is the financials of the Heidrick's local subsidiary in my home country, Finland, where financials of companies are public. For the past four years the local company has delivered average revenues of €3.6 million with an average EBIT of 48%. The subsidiary has employed nine to ten people. Unfortunately the business has remained flat.

Heidrick has a strong balance sheet to weather through tougher times. It doesn’t have any long-term debt nor short-term borrowings. In the end of Q1 the company had $205 million of cash and equivalents on its balance sheet. The cash balance varies heavily quarter to quarter, since 2018 the quarterly cash balance and short term investments have averaged $283 million.

Consulting business needs to be turned around

Heidrick’s consulting business has been a big drag on earnings. Although selling HR-related consulting to the same customers and recruited people, has some logic, the performance leaves much to be desired.

In the Q1 2023 the operating income went into the wrong direction and declined from negative two million to three million. The aforementioned goodwill impairments in the past have resulted from previous acquisitions and poor development of the consulting business.

Revenue and operating income of consulting business. (10-Ks)

In Q1 2023 the company plowed more money into another business by acquiring a British company called Businessfourzero, which helps businesses in “purpose-driven transformations". The details of the acquisition were not disclosed. However, the company features rather high profile customers on its website, such as Tesco, Reckitt, Electronic Arts.

The table above implies several challenges. Business that is based in its entirety on people and relationships, is difficult to integrate and the performance is challenging to maintain. Consulting is ultimately different from Heidrick’s core business. The financial performance of Heidrick's consulting business also questions the capital allocation and execution skills of the management.

Turning around the profitability would be positive to the earnings and returns on capital. Unfortunately the current market environment won’t help the company in turning the consulting business to a profit contributing unit. Despite the negative operating income of the consulting business, Heidrick has delivered excellent returns on capital over the recent past.

On-demand talent potential growth area

In February 2023 Heidrick announced an acquisition of German on-demand talent company Atreus. The acquisition expanded Heidrick’s reach to Europe after it had acquired Business Talent Group in the U.S. in 2021. Atreus will add $61 million revenue on top of the $91.4 million of consulting revenue in 2022. On-demand talent, or interim management, appears better suited around Heidrick’s core business, and although there are no good market data available, interim management is a quickly growing way to meet rapidly changing talent needs of enterprises.

Heidrick's historical growth rates. (Seeking Alpha)

The company is also developing a digital product called Navigator. which is an AI-powered leadership intelligence platform. At the moment the product is in a beta testing phase. Heidrick expects bookings to start in early 2024. The product is unlikely to move a needle for the company, but it’s one of the reasons for R&D spending and a sign of the company maintaining its relevance.

Heidrick’s valuation looks attractive

Heidrick appears attractively valued based on its historical multiples. Due to Heidrick's capital structure, EV/EBIT appears the most suitable multiple to evaluate the valuation. If we would apply a historical 7.8x EV/EBIT multiple on the $73 million estimated EBIT we would arrive at an enterprise value of $570 million, indicating an upside of 25% and stock price of $35.

Heidrick's current multiples and historical averages. (Tikr)

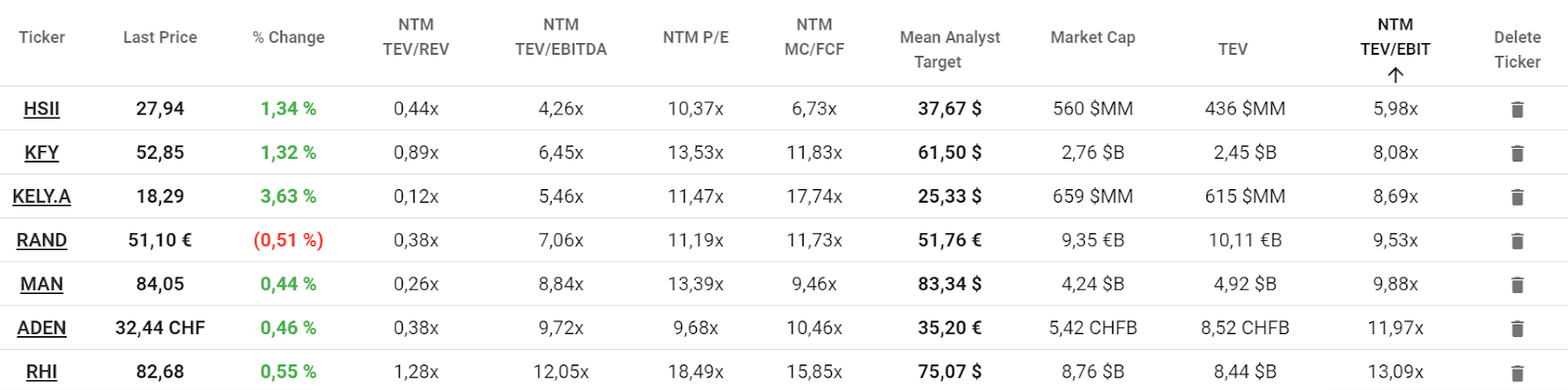

Heidrick’s stock is also trading at a significant discount to its peers based on several forward-looking multiples. Heidrick’s NTM EV/EBIT stands at 6x while the peer group mean is 9.6x. Heidrick appears particularly cheap based on price to free cash flow basis. The mean of the seven companies is 12x, whereas Heidrick’s multiple is nearly half this.

Multiples of the peer group. (Tikr)

{kind=link}

In terms of financial performance, showcased here by ROE and EBIT margin, Heidrick fares well against the second and third cheapest stocks in the peer group. Korn Ferry has upped its game recently. This comparison indicates that Heidrick doesn’t necessarily deserve the lowest multiples in the peer group.

ROE and EBIT-% of HSII, KFY and KELY. (Tikr)

If we compare Heidrick to the more expensive American peers Manpower and Robert Half International, we can see that Heidrick performs well compared to Manpower, but Robert Half’s high multiples could have a merit due to its better performance.

ROE and EBIT-% of HSII, RHI and MAN. (Tikr)

If we take the estimated 2023 EPS of $2.7, terminal multiple of 12 (5-year average) and discount rate of 10%, the market is expecting approximately 6% earnings growth in the longer term. Heidrick has grown EPS at a much higher pace historically.

There are only three analysts following the company and their average target price for the stock is $37.7.

Dividend provides a decent base yield

Heidrick has been paying a quarterly dividend of $0.15 since the beginning of the year 2019. This translates to an annual payment of $0.6 and a dividend yield of 2.1%, which is slightly above its five year average of 1.9%. Against last year’s excellent earnings ($3.86), the payout ratio is only 15%. If we completely disregard the negative years of 2017 and 2020, the average EPS for the past decade is $1.85, resulting in a payout ratio of 32%. Based on these data points, the dividend could be deemed safe.

Unfortunately Heidrick doesn’t do many stock repurchases and shares outstanding have slowly creeped up.

Conclusion

Although the company’s business is likely to face headwinds, Heidrick has potential to grow and enhance its profitability further. The business is inherently very cash generative and profitable. If the company manages to finally turn consulting profitable and also grows profitably in the interim management business, the returns on capital and earnings will further improve. This could be one catalyst to reverse Heidrick's attractive valuation closer to its historical levels and closer to its peers. The dividend also provides a decent base yield while waiting to see the investment thesis develop.

For further details see:

Heidrick & Struggles: Attractively Valued Cash Cow With Growth Prospects