HINKF - Heineken: Leads In The Global Beer Market

2023-07-07 08:00:00 ET

Summary

- Heineken N.V. is a leading Dutch brewing company with a diverse portfolio of international and regional beer brands, operating in over 70 countries.

- Heineken is forecast to continue its growth trajectory, with margin improvement expected as inflationary pressures subside.

- Heineken has supplemented its portfolio with acquisitions, allowing the business to partake in growth areas such as craft beer.

- Relative to peers, we believe Heineken performs slightly better. This implies upside based on its current valuation.

Investment thesis

Our current investment thesis is:

- Heineken is positioned well to generate continued strong returns, due to its ownership of several leading brands in the wider beer market.

- Margins are poised to improve as inflationary pressures subside, further supporting financial returns.

- The company has a wide moat due to its leading position in many segments within the market, as well as its global distribution network.

- Relative to peers, we believe the company is attractively positioned.

Company description

Heineken N.V. ( HEINY ) is a leading Dutch brewing company known for its flagship brand, Heineken, and a diverse portfolio of international and regional beer brands. The company operates in over 70 countries, with a strong presence in Europe, the Americas, and Asia-Pacific.

It offers its beers under the Heineken, Amstel, Sol, Tiger, Birra Moretti, Pure Piraña, Desperados, Edelweiss, and Lagunitas brands; and cider under the Strongbow Apple Ciders, Orchard Thieves, Cidrerie Stassen, Bulmers, and Old Mout brands, as well as under regional and local brands.

Share price

Heineken's share price has underperformed the market, although has achieved healthy financial development. The company has continued its strong growth trajectory while maintaining good profitability.

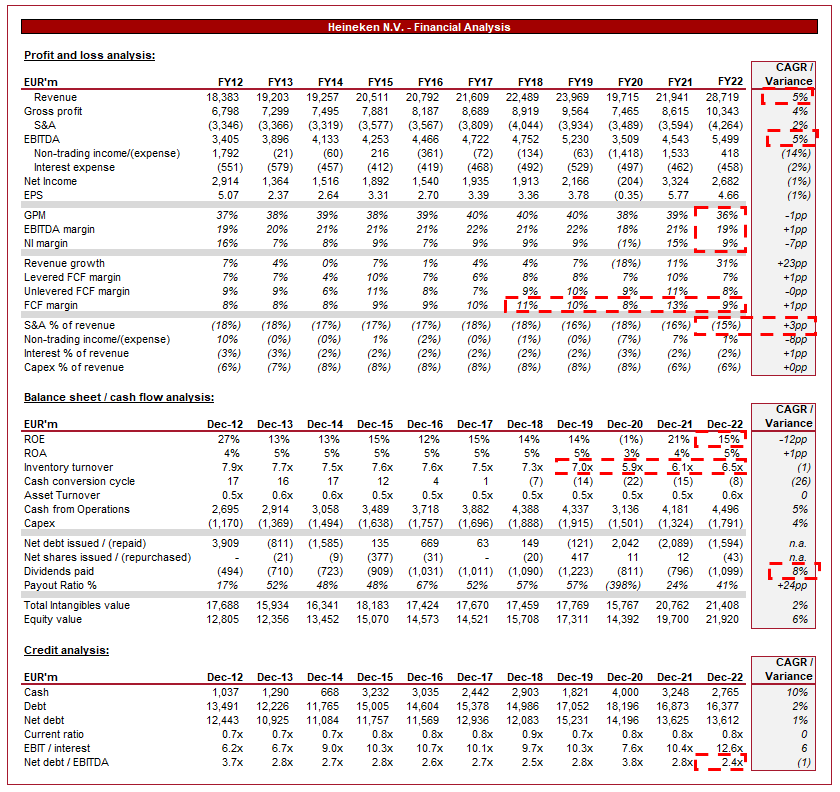

Financial analysis

{kind=link}

Presented above is Heineken's financial performance for the last decade.

Revenue & Commercial Factors

Heineken's revenue has grown at a CAGR of 5% in the last 10 years, as its fundamental strength in the industry remains, allowing the business to achieve enjoy market growth. Throughout this period, the company only experienced a single period of negative growth (Covid impacted), reflecting its resilience.

Business Model

Heineken's focus has been on building a premium brand portfolio, which includes Heineken, Amstel, Desperados, and Strongbow, among others, catering to different consumer preferences and markets. The objective is to capture a large segment of the market through a range of brands, similar to the strategy conducted by fashion houses like LVMH ( LVMHF ).

The company operates a decentralized managerial structure, with local breweries and sales teams in various countries, allowing for adaptation to local market dynamics and consumer tastes, which generally differs by country. For example, Strongbow is a market leader in the anglosphere and so continues to produce the majority of its beverages at Bulmer's Hereford plant (Group entity above Strongbow).

For this reason, supply chain management is critical, with the returns equally lucrative, as it allows for shared competencies and economies of scale to minimize costs. Heineken manages its supply chain well, reflected in its consistent margins, ensuring consistent quality, efficient production, and distribution of its beer products.

Competitive Positioning

We believe there are three key competitive advantages Heineken has.

Firstly, Heineken's brands are recognized globally as a premium offering, allowing the business to enjoy high consumer loyalty and access to new market entrants.

The company's extensive distribution network and geographic presence enable access to a wide variety of markets. Access to bars and pubs, for example, is vital to achieving scale and longevity. Its strong brand in conjunction with its distribution network allows the brand to maintain its dominance over access to customers.

Finally, with a wide variety of brands, many of which are acquired over time, the company is in a position to continuously introduce new products and expand its portfolio to cater to evolving consumer preferences. Consumer tastes, like in so many industries, tend to change and so it is critical to remain aware of this. Most recently, Heineken acquired Beaverton Brewery, expanding its presence in the growing craft beer segment.

Alcohol Industry

Businesses compete based on factors such as brand strength, product quality, pricing strategies, distribution channels, marketing campaigns, and innovation. Major competitors of Heineken include Anheuser-Busch InBev ( BUD ), Carlsberg ( CABGY ), Molson Coors ( TAP ), and Diageo ( DEO ), among others. The beer market is estimated to be $794bn in size , growing at a CAGR of 4% into 2030. The market is large enough for all of these brands to co-exist, although there is fierce competition in each market, primarily in factors other than price.

The growing popularity of craft beer and consumers' preference for unique, local, and artisanal offerings is majorly disrupting the beer industry. These are the same reasons why the industry has seen premiumization, supporting Heineken's strategy. In response to this, we have seen a wave of acquisitions, as the traditional players (listed above), rapidly seek to tap into this growth. As well as the recent acquisition, Heineken owns Affligem, Lagunitas, and Mort Subite. All four brands provide Heineken with strong exposure to the industry.

Further, we are seeing changing consumer attitudes toward healthier lifestyles, which is impacting beer consumption patterns and driving demand for low-alcohol and non-alcoholic alternatives. Heineken is leaning heavily into this, both through acquisitions and the development of non-alcohol equivalents. Heineken has illustrated its commitment in Formula 1, where it is a lead sponsor, choosing to advertise its non-alcohol equivalent. The marketing is smart as it's clearly the company's logo (thus targeting the masses) but with a subtle but clear illustration of its zero alcohol contents.

Margins

Heineken's margins have been incredibly consistent in the last decade, currently boasting a GPM of 36% and an EBITDA-M of 19%.

Heineken's attractive margins are a reflection of its strong pricing power, due to brand strength, its premiumization strategy, and its scale providing cost benefits.

Although the absolute margins are attractive, it is disappointing to see the business has been unable to gain scale economies. This is due to inflationary pressures (such as the cost of glass), reducing the company's gains made in the lead-up to FY19. We suspect the business could make gains in the coming years as pressures subside.

Balance sheet & Cash Flows

Heineken is moderately financed, with a ND/EBITDA ratio of 2.4x. Our view is that a 3-3.5x level is a healthy maximum, implying Heineken still has some flexibility. This is vital as it allows the business the ability to conduct further M&A if required.

Heineken's cash flows have been extremely consistent, owing to its profitability and operational excellence. Post-covid, we have seen its CCC decline, partially due to a decline in inventory turnover. An improvement in this should support an improvement in FCF.

Distributions to shareholders have been in the form of dividends which have been volatile during the historical period. Based on the current cash flow, this level looks sustainable.

Outlook

{kind=link}

Presented above is Wall Street's consensus view on the coming 5 years.

Analysts are forecasting an uptick in the company's growth rate in the near term compared to its 10Y average, a reasonable estimate based on Heineken's recent performance and industry tailwinds.

Margins are expected to improve gradually over time, a reasonable expectation given the improvement in scale expected and costing pressures subsiding.

Industry analysis

Brewery industry (Seeking Alpha)

{kind=link}

Presented above is a comparison of Heineken's growth and profitability to the average of its industry, as defined by Seeking Alpha (7 companies).

Heineken is marginally above average. From a growth perspective, the company slightly lags on a revenue basis but this is offset by profitability growth, implying the strong margins are offset by its mild revenue growth.

Margins are superior to peers, although not significantly so. Importantly, the company is more efficient with its asset allocation, with a higher ROE and ROA.

Based on this, we believe Heineken deserves a slight premium to the average valuation of these businesses. In a mature industry, we prefer margins to growth (Caveated that substantially higher growth is more preferable still).

Valuation

{kind=link}

Heineken is currently trading at 12x LTM EBITDA and 10x NTM EBITDA. This is a discount to its historical average.

Compared to the company's historical average position, we believe there has been some improvement, namely:

- Improved scale.

- Marginally better free cash flow conversion.

- Reduced leverage.

- Scope for margin improvement.

These factors do not imply a significant premium but we believe it would be reasonable to suggest a premium of c.10% is appropriate. Based on this, there is an upside of 10-13.5% at its current price.

When compared to peers, Heineken is trading at a 7% discount on an LTM EBITDA basis and the same percent on a NTM P/E basis. Again, we believe a slight premium is warranted (c.5% given the margin superiority is minimal), implying upside again.

Key risks with our thesis

The risks to our current thesis are:

- Further margin deterioration. Given the competitiveness of the market, winning margins back is not an easy task. For this reason, any margin deterioration represents a key risk to returning to >20% levels.

- Trend changes. Changing trends continue to represent a risk to the business, even if it can "buy" its way of the problem. This is still risky because a strategic misstep could leave the business lagging behind peers and unable to catch up.

Final thoughts

Heineken is an incredibly strong business. It owns a range of market-leading brands, allowing the business to grow well and generate large returns. We believe this will continue in the coming years, with scope for margin upside as inflationary pressures subside.

When compared to peers and its historical average, we see scope for upside that is seemingly not priced in. Based on this, we believe the stock is undervalued.

For further details see:

Heineken: Leads In The Global Beer Market