HINKF - Heineken: Soft Emerging Market Volumes Don't Tar Value Potential

2023-10-07 08:18:36 ET

Summary

- Heineken has seen soft volumes in key emerging markets hit its share price, with the stock currently off around 20% from its 2023 highs.

- Aggressive price hikes should moderate into H2, while cost inflation should also start to ease off a little. This will help restore earnings in the back half of 2023.

- Heineken's route to high single-digit per annum earnings growth remains in place, with the firm well-placed to capitalize on key beer industry growth spots.

- The ADRs look attractively valued in the low/mid-$40s area, and I expect 10%-plus annualized returns in the medium-term from here.

As I briefly mentioned the last time I covered the firm, emerging markets and 'premiumization' (i.e. driving higher prices) likely represent Heineken's (HEINY)(HINKF) best shot in terms of long-term earnings growth. At the end of the day the global brewers, of which Heineken is #2 to Anheuser-Busch InBev (BUD), only have so many drivers to boost chronically low beer volume growth, and the two just mentioned are by far the clearest.

While Heineken is relatively well-placed on both counts, if I had to think of a possible downside to this strategy it is that it might introduce a modicum of cyclicality into a what is typically a very defensive business. That may be playing out to a degree this year, with the firm entering the Q3 reporting season on the back of earlier soft performance in some of its key emerging markets.

As a result, these shares have fallen around 20% from their 2023 highs in local currency terms, and a little more for the USD-denominated ADRs due to foreign exchange movements.

The above said, it's important not to overdo it here. A softer than anticipated year in FY2023 still probably sees Heineken eke out some year-on-year operating profit growth, while I'm hopeful that improvement in H2 will carry over into a better full-year performance in FY2024 and beyond. With these shares now only trading for around 16.5x EPS compared to over 20x a few months back, Heineken today looks like a solid long-term value pick.

EM Weakness Likely A Temporary Setback

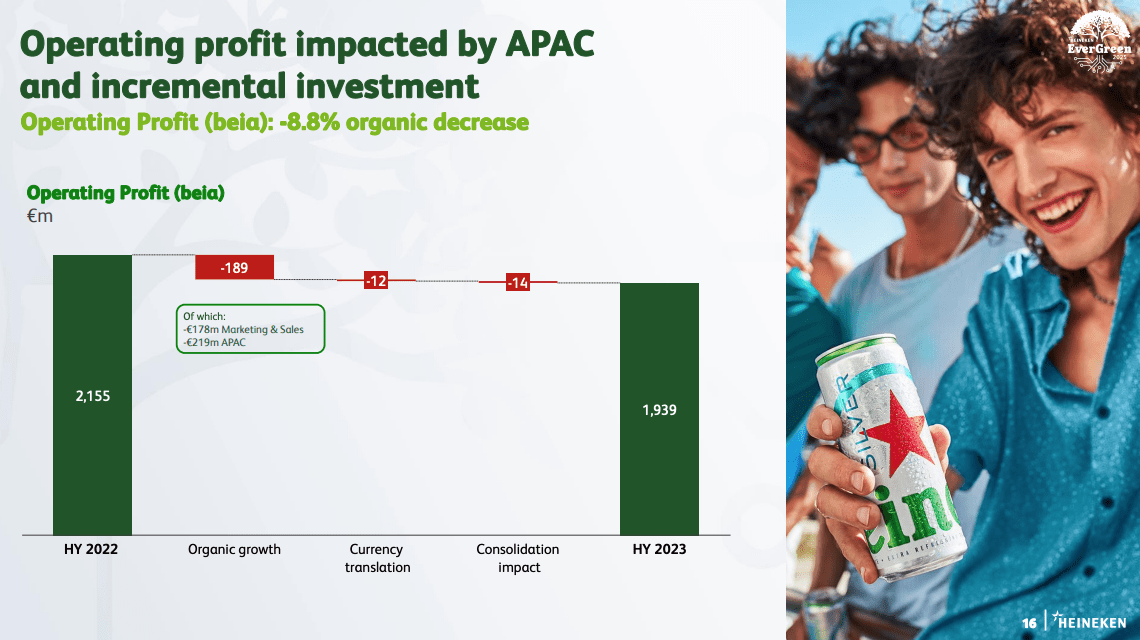

Heineken will provide its Q3 trading update in a few weeks, and investors will be hoping to see some stabilization after a pretty soft Q2. Beer volumes fell 7.6% in that quarter, driving a 5.6% volume decline for the first half of FY2023. H1 underlying operating profit fell 8.8% year-on-year to €1.94 billion (Fig 1).

Asia Pacific (~17% of consolidated volume) was a particular weak spot, with volumes declining 13.2% in H1 and 15.5% in Q2 specifically. APAC underlying operating profit fell 34% year-on-year to €400 million.

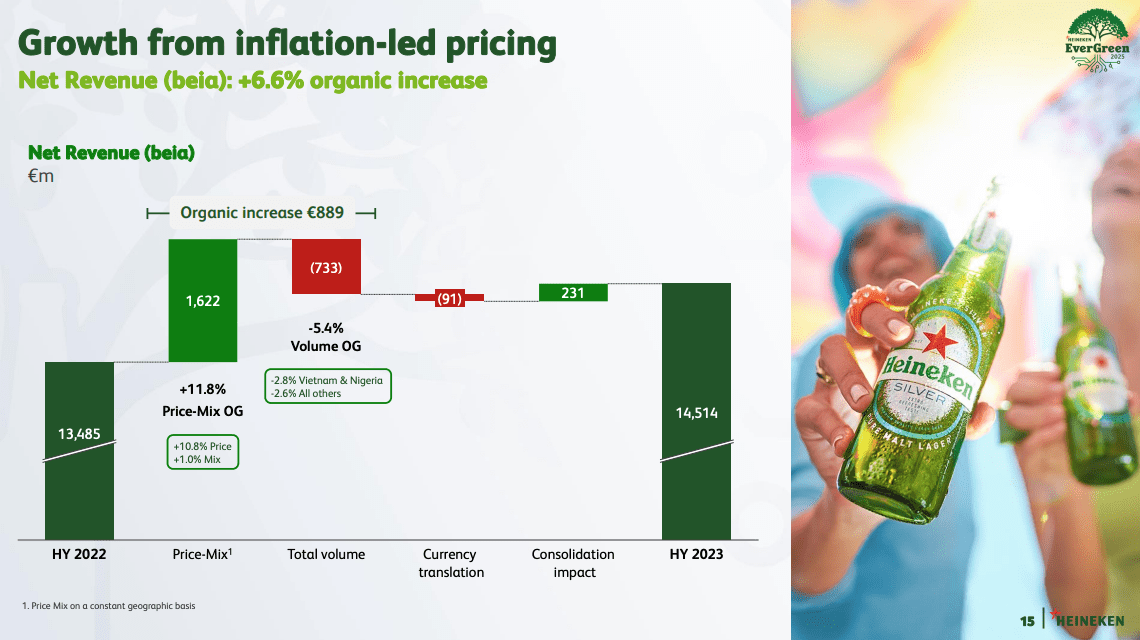

Fig 1. (Source: Heineken NV Interim Results Presentation) Fig 2. (Source: Heineken NV Interim Results Presentation)

{kind=link}

{kind=link}

Heineken was battling a couple of issues in its fiscal first half. Firstly, it hiked prices aggressively in order to compensate for the impact of inflation on its cost base. Net revenue per hectoliter was up 12.7% against a "mid-teens" rise in energy, water, transport and raw materials. Expense lines like staff salaries (up around 5% year-on-year) were also affected by elevated inflation, while marketing spend as a portion of sales was hiked 60bps in order to support its brands. That cost the firm volume as per above (Fig 2), with consumers not willing to absorb price increases like they were a year ago.

Relatedly, the company has come up against some very soft macro conditions in certain emerging markets like Nigeria and Vietnam, with those two countries ultimately responsible for around half of H1's consolidated volume decline. Vietnam has been a boon for Heineken over the past decade or so due to some structural tailwinds (rising GDP and a doubling in per-capita consumption off a low base). Still, manufacturing-led growth has been a key pillar of the country's economic performance, and a global economic slowdown is hitting it fairly hard. Heineken's business there also skews more toward premium brands, and that makes it a bit more sensitive to general economic conditions.

H2 performance is implied to be significantly better (given guidance for 0-6% full-year operating profit growth). I don't see that as a particularly high bar to clear given slightly lower cost inflation - seen around 2-3ppt better half-on-half in H2 - and better volume performance as pricing-per-hectoliter growth falls back a little. Vietnamese demand should also show some improvement as around half of the volume decline there was due to de-stocking after the Lunar New Year festival.

Shares Look Good Value For The Long Run

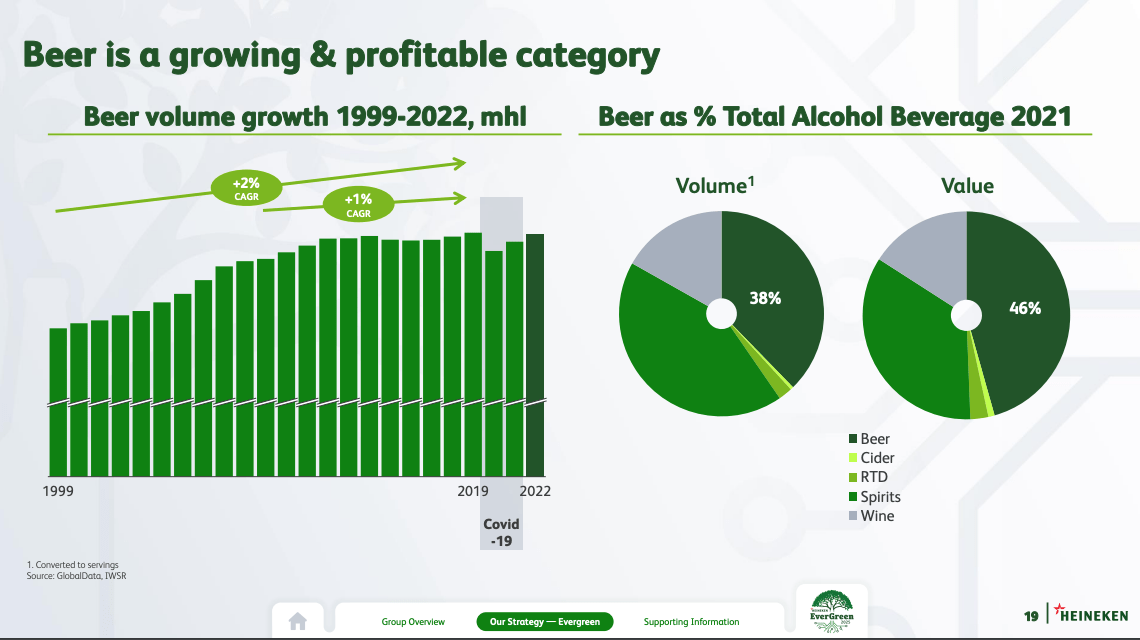

Disappointing short-term performance aside, I still view Heineken's long-term strategy of targeting emerging markets and premiumization as being sound. The main issue for the global brewers is that beer volumes have only registered a circa 2% CAGR over the past 25 years, with that falling to around 1% since 2009 (Fig 3). A large portion of that is due to poor developed market ("DM") demographics, with DM consumers also rotating out of beer and into spirits (Fig 4).

In contrast, many emerging markets ("EM") offer better demographics and are still seeing beer gain ground as a share of throat due to lower per-capita consumption. The competitive landscape is also better (i.e. higher margin) in a lot of Heineken's EM operations when compared to its predominantly European DM footprint.

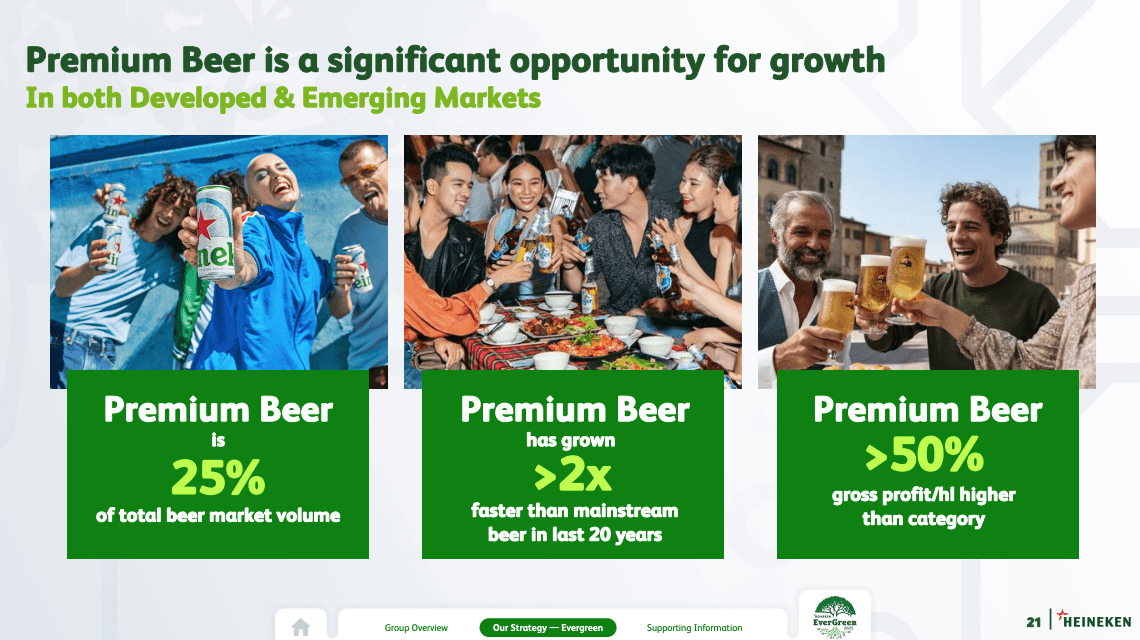

Similarly, the premium segment of the beer category has outgrown the category as a whole by a fairly wide margin (Fig 5). Heineken remains well placed to capitalize on both trends, with sizable EM operations (~59% group EBIT) and a beer portfolio that skews to premium (40% of net revenue).

Fig 3. (Source: Heineken NV August 2023 Investor Presentation) Fig 4. (Source: Heineken NV August 2023 Investor Presentation) Fig 5. (Source: Heineken NV August 2023 Investor Presentation)

{kind=link}

{kind=link}

{kind=link}

With that, my core assumption of a 4-5% long-term revenue CAGR remains in place from last time. I also still see margin expansion driving higher levels of earnings growth, notwithstanding the recent negative impact of inflation (1H2023 EBIT margin was 13.4%, around 260bps below the 2010-2019 average) (Fig 6). Seeking Alpha already scores Heineken a "B+" on profitability , and I expect that to improve over the next few years due to operating leverage.

The ADRs trade for $43.93 at time of writing, putting them at circa 16.8x FY2022 EPS and 16.5x my FY2023 EPS estimate. That represents a discount to the circa 18x EPS multiple Heineken averaged in the 2010s (with that range chosen to normalize for COVID) (Fig 7). Heineken clocked in an EPS CAGR of around 6% in that time (Fig 8), which I expect it to beat in the medium term.

Fig 6. (Data Source: Heineken NV Annual Reports) Fig 7. (Data Source: Heineken NV Annual Reports, Yahoo Finance) Fig 8. (Data Source: Heineken NV Annual Reports)

With the above in mind, I see around 10-11% annual returns over the next few years on a flat P/E. That is made up of high single-digit earnings growth (split roughly 2:1 between revenue growth and EBIT margin expansion), plus the current 2.35% yielding dividend growing in line with earnings.

Risks

My main short-term concern is largely macro related, specifically that a sharp economic downturn could lead to softer performance in Heineken's emerging markets and/or the premium-end of the beer category more generally. Similarly, stickier inflation and/or softer volumes could put downward pressure on EBIT margins. Heineken struggling to get EBIT margins back to the high-teens area is the most obvious long-term risk too.

While the above would mean annualized earnings growth would likely land around 4ppt lower than my target, I'd argue that is what these shares are pricing in right now anyway. Given that, I'm happy to stick with my Buy rating.

Editor's Note : This article was submitted as part of Seeking Alpha's Best Value Idea investment competition , which runs through October 25. With cash prizes, this competition -- open to all contributors -- is one you don't want to miss. If you are interested in becoming a contributor and taking part in the competition, click here to find out more and submit your article today!

For further details see:

Heineken: Soft Emerging Market Volumes Don't Tar Value Potential