HTWSF - Helios Towers: African Growth To Diversify Your U.S. TowerCo Holdings

2023-04-29 03:17:04 ET

Summary

- The U.S. appears to be harboring the worst of both worlds, high inflation on the one hand, and a slowing economy on the other.

- At the same time, 5G-related equipment installations at American Tower and Crown Castle had already reached the 50% mark at the end of 2022, implying sluggish revenue growth this year.

- This calls for rest-of-the-world diversification, through London-based Helios Towers which offers exposure to Africa's fast-growing telecom towers.

- Given that investors used to putting their money in geopolitically-safe America try to avoid investing in more uncertain parts of the world, I emphasize risks throughout the thesis.

- To its credit, Helios offers country-level diversification and a business model which favors profitability, while providing services to blue chips.

At a time when macros are deteriorating in the U.S. and with both American Tower ( AMT ) and Crown Castle ( CCI ) having likely passed the point of maximum growth for 5G-related tower equipment as I will detail later, the aim of this thesis is to show that an investment in faster growing Helios Towers ( HTWSF ) as tabled below, makes sense.

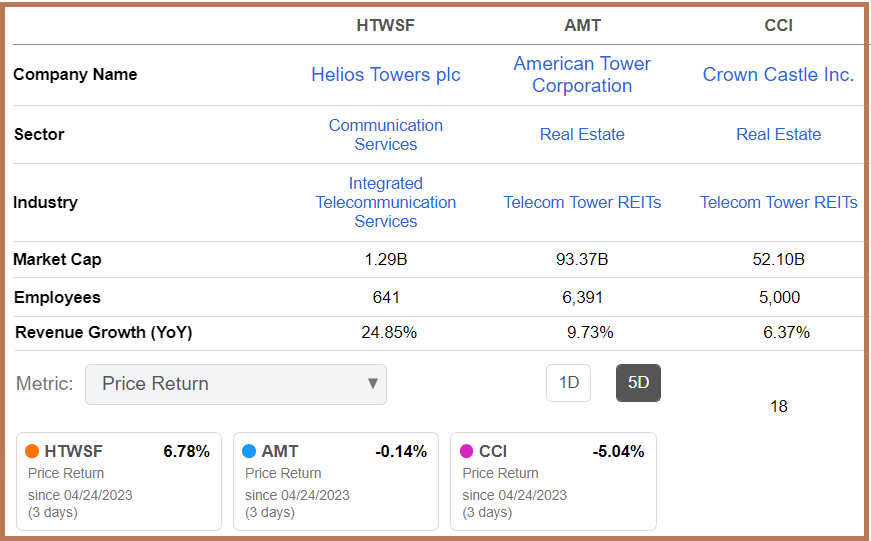

Comparison of Key Metrics for HTWSF, AMT and CC (seekingalpha.com)

{kind=link}

Well, the U.K. based company with tower operations in Africa does not possess the scale of its U.S. counterparts, but, it is rapidly improving in EBITDA as I will elaborate on later. Also, looking at its five-day price performance of 6.78%, there is definitely some interest in the stock.

However, instead of pitching these TowerCos (tower companies) against each other, my approach will be to show that instead of adding to your shares of AMT and CCI by buying the one-year dips , an investment in Helios makes more sense. For this purpose, I will use a balanced risk approach in an economy where the Fed's agenda to control inflation has given rise to liquidity issues as evidenced by the banking turmoil.

The difficulty for the Economy and TowerCos

A glance at the macroeconomic environment shows the U.S. gross domestic product has slowed down significantly in the first quarter of 2023 at a 1.1% annualized rate compared to 2.6% in the last three months of 2022. At the same time, core inflation remains high at above 5.5% with the Federal Reserve now having to make sure it does not further destabilize the banking sector while trying to restore price stability.

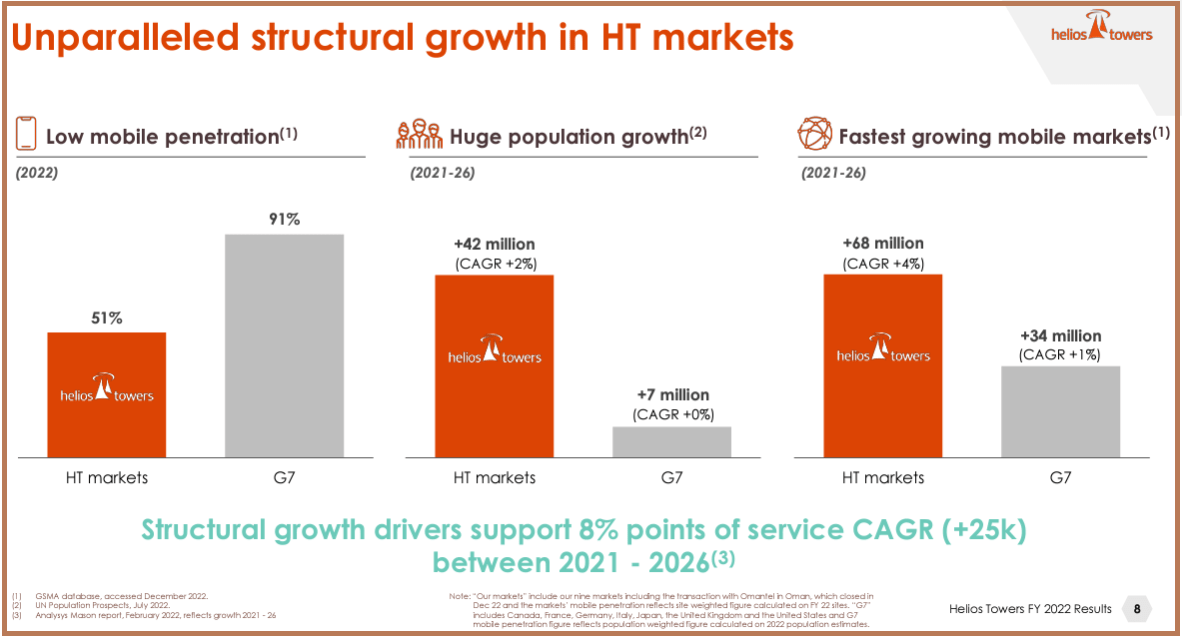

In these conditions, while its Chairman is not likely to sustain his hawkish tone throughout this year, rates may have to stay higher for longer as inflationary pressures persist. Such a situation is not conducive to growth, for a country that together with other members of the Group 7 (G7) countries already has a mobile penetration rate of 91% as pictured below.

Comparing Mobile Penetration Rate, Population growth, and markets (static.seekingalpha.com)

{kind=link}

Well, generally speaking, penetration primarily concerns earlier cellular network generations like 3G and 4G, while most of the capital expenses made by U.S. MNOs (mobile networks operators) like T-Mobile (TMUS) and integrated telecom operators like Verizon ( VZ ) has been consumed by the migration from 4G/LTE to 5G.

Part of these investments have benefited tower companies like AMT and CCI who rent their properties and towers to service providers, and as a result, they have grown revenues rapidly as shown by the charts below.

However, the shapes of the charts indicate that after growing rapidly since 2020, growth is slowing down, and one of the reasons is that both companies are now past the point of maximum addition of 5G radio equipment. Thus, in their respective fourth quarter 2022 earnings call, about 50% of AMT's sites were already equipped with 5G from carriers while approximately half of CCI's sites were upgraded with mid-band spectrum equipment.

Now, by no way, this implies that revenue growth peaked in 2022 given that nationwide expansion is continuing as well as densification activities whereby existing sites are equipped with additional equipment in order to improve signal quality. However, these activities are not likely to be carried out at the same frantic pace, with the probability of the U.S. entering into a recession now exceeding 60% . This all means more sluggish growth going forward.

On the other hand, the markets where Helios operates have a mobile penetration rate of just over 50% (see penetration rate diagram above) implying opportunities for rapid growth, namely at a CAGR of 4% from 2021 to 2026. As a result, the company has been delivering a sustained organic growth of 7%-8% in tower tenancy since 2019 and expects similar figures for fiscal 2023.

Looking at the bottom line, its EBITDA growth is even more enticing, as I will elaborate later, but, for now, it is important to look at a potential investment in Helios from the balanced risk perspective.

Balancing Risks of U.S TowerCos Vs Helios' African Growth

First, for those holding the stocks of companies based in the U.S. where there is political and social stability, investing in Africa may appear risky. In addition, as per the lease agreement signed with carriers, U.S. TowerCos can navigate through higher inflation by charging more to customers in response to changes in the CPI, which implies that they can still increment their top lines for years to come.

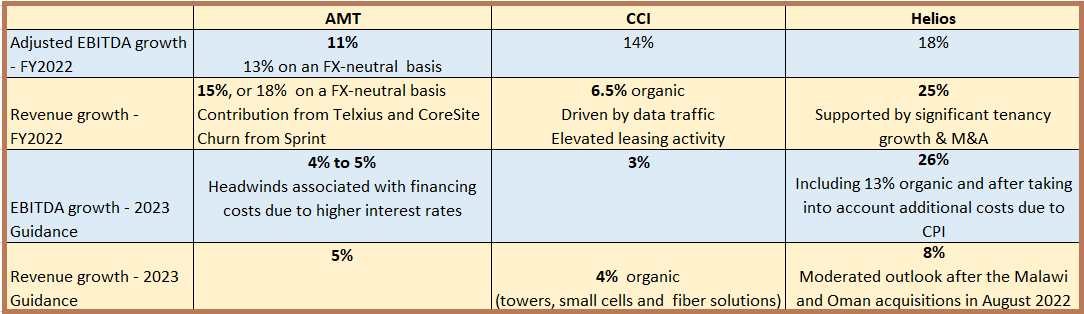

Looking further, these companies have also expanded in other industry verticals with CCI in fiber and small cells, while it is data centers as well as tower operations in other parts of the world for AMT. Still, as seen by both companies' EBITDA and revenue growth for 2022 and projections for 2023 in the table below, they are in the 3% to 5% range, far behind Helios' numbers of 8% to 25%.

Table Built Using Data from (www.seekingalpha.com)

{kind=link}

Focusing on the EBITDA growth, it should be 26% (midpoint) YoY in 2023 as the company executes on the Malawi and Oman tower acquisitions performed in August of last year, with tenancy additions expected to be around 8%.

Looking at the bigger picture, the company has nearly doubled its tower infrastructure from 7K to 14K in just about three years while at the same time expanding from five to nine countries. Empowered by these acquisitions, the aim is to grow organically in 2023 while investing less. For this purpose, only $170 million to $210 million of capex is expected to be consumed this year compared to $765 million in 2022.

Thinking aloud, country-level diversification helps to mitigate the risks associated with the region where Helios operates and also differentiates it from peers in Africa. In this respect, AMT is diversified with around 11,700 towers in seven African countries.

In addition, Helios has signed long-term contracts with large, blue chips MNOs which accounted for 98% of its revenues in 2022, and 63% of revenues were constituted of hard currencies (USD and Euro). These contracts had a total value of $4.7 billion as of the end of last year with an average remaining life of 7.6 years. Noteworthily, the amount of $4.7 billion is 8.4 times FY-2022 revenues and helps to cushion against risks of a sudden downturn.

Valuing by Considering Risks and Resiliency of the Business Model

Thus, for those prioritizing stable revenues with income, dividend-paying AMT and CCI make for appropriate investments, but at the same time, one must be realistic that there are challenges with inflation likely to remain high plus the increased probability of a recession as I mentioned earlier. In these conditions, tower companies may simply not have the appetite to pass on costs to lessees and may have to absorb some of them while waiting for better times.

In the meantime, as part of portfolio diversification, one can invest in Helios headed by Tom Greenwood , which provides exposure to the African telecom sector.

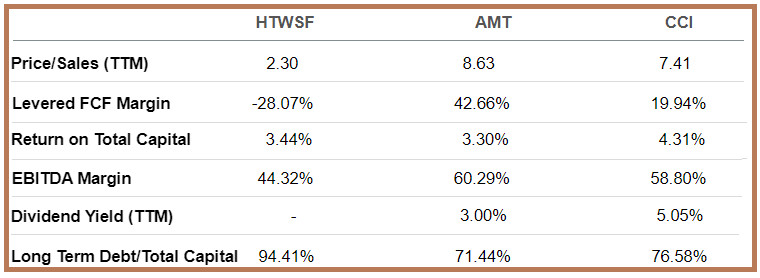

Comparison of more metrics (www. seekingalpha.com)

{kind=link}

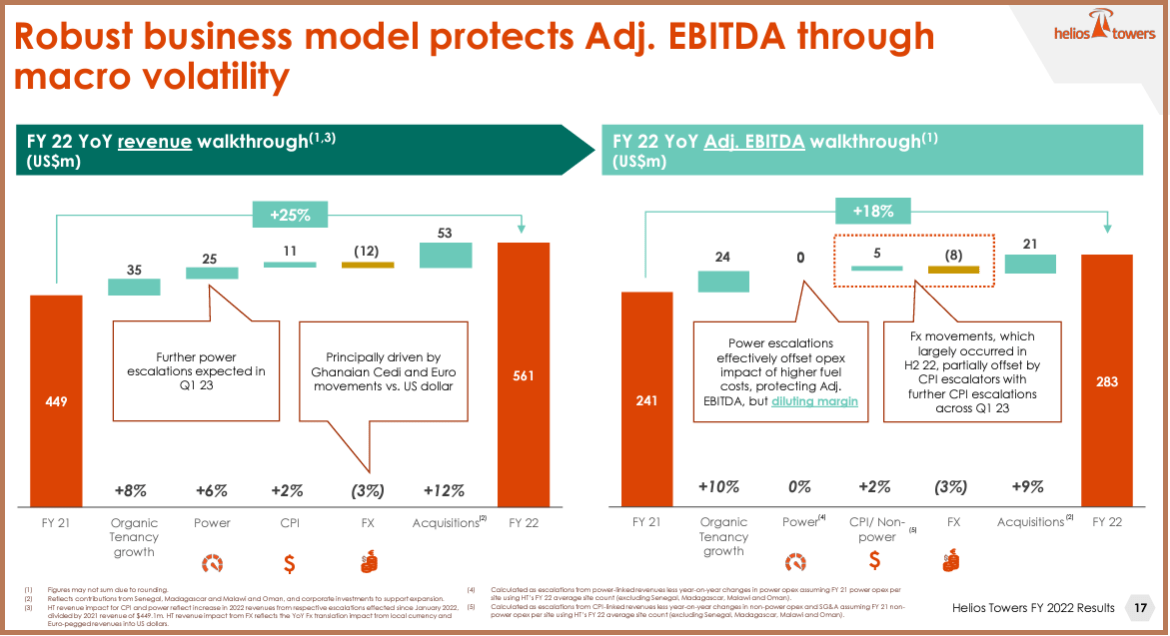

For this purpose, unlike its American counterparts which are structured as REITs or real estate investment trusts which have to distribute a big chunk of their taxable profits to shareholders as dividends, Helios operates as a normal company communication services sector. As such, it also provides power as a service in regions where the grid is not well developed. Therefore, power (in addition to tenancy), is another lever to escalate costs to its tenant base and helps to offset higher operational costs due to energy prices as pictured below.

Robust Business Model for EBITDA growth (static.seekingalpha.com)

{kind=link}

As for valuations, its trailing price-to-sales ratio of 2.30x (above table) is at least three times lower than its peers. However, with much better free cash flow margins and located in geopolitically safe regions, U.S. TowerCos deserve their richer valuations as they make for less risky investments. Still, Helios' EBITDA margins are not far below its two peers, and with its capital expenditure expected to drop four times this year compared to 2022 as I touched upon earlier, the cash position should improve significantly. For this matter, FCF is anticipated to increase by 18% (midpoint) in 2023, and the shift to organic growth (as opposed to M&A) implies that the debt level is not likely to increase.

Furthermore, the return on total capital is at 3.42% or about the same as its U.S. counterparts, meaning approximately the same level of efficiency in allocating capital to generate profits. This also implies that despite operating and investing heavily in Africa, the company has not faced an abnormally high cost of capital, which it has raised through a mix of equity, debt, and convertibles.

Coming back to the price action, after the recent upward momentum, there is room for further upside given that the stock is down by 22.22% during the last year. Consequently, depending mostly on financial results which are scheduled for May 18, the stock could rise. Just considering a 10% gain, it could climb back to the $1.39 (1.26 x 1.1) level based on its current share price of $1.26. This translates to a P/S of only 2.53x (2.30 x 1.1), which is still far below peers.

Rest-of-the-World Diversification in Helios

Therefore Helios is a buy and I have a moderate target which takes into consideration that exposure to the African continent entails more risks than geopolitically safe U.S.A. In this case, AMT also has extensive operations in the continent, but this only constitutes 18.5% of its total number of towers globally.

In conclusion, this thesis has made the case for investment in Helios, more as part of a portfolio diversifier for existing TowerCo investors. Metrics that have proved useful not only include revenue but also EBITDA growth as well as the way capital has been deployed to generate profits. On the risk side, factors like country-level diversification and exposure to blue chips are positives.

Last but not least, there is also the business model which helps to cushion the EBITDA against volatility, induced by factors like higher CPI, inflated energy costs, and foreign exchange fluctuations.

For further details see:

Helios Towers: African Growth To Diversify Your U.S. TowerCo Holdings