HTWSF - Helios Towers: An Attractively Priced Tower Company In Emerging Markets

Summary

- Helios Towers operates in excess of 13,000 towers in Africa and Oman.

- Africa's tower landscape is still very fragmented and Helios could use this to its advantage.

- Trading at less than 9x the 2023 EBITDA, the stock isn't expensive.

- The higher cost of capital likely indicates future M&A will have to happen at lower multiples than its recent Oman acquisition.

Introduction

Helios Towers ( OTCPK:HTWSF ) has a very straightforward business model. It is an Africa-focused cell phone tower owner and operator and thus a much smaller peer than for instance American Tower ( AMT ) or Cellnex Telecom ( OTCPK:CLNXF ) ( OTCPK:CLLNY ) is. I recently reviewed Cellnex Telecom and you can read that article here .

{kind=link}

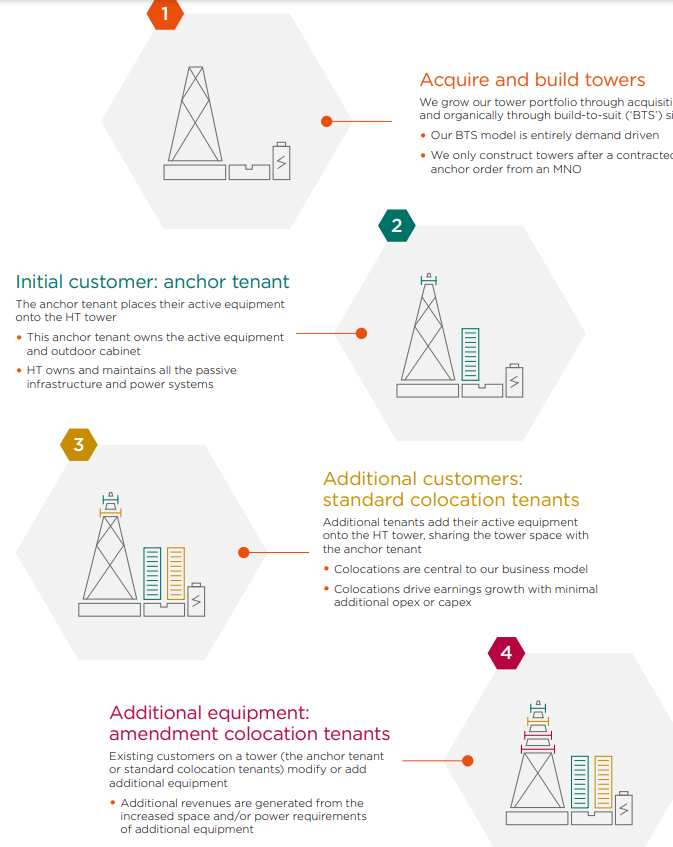

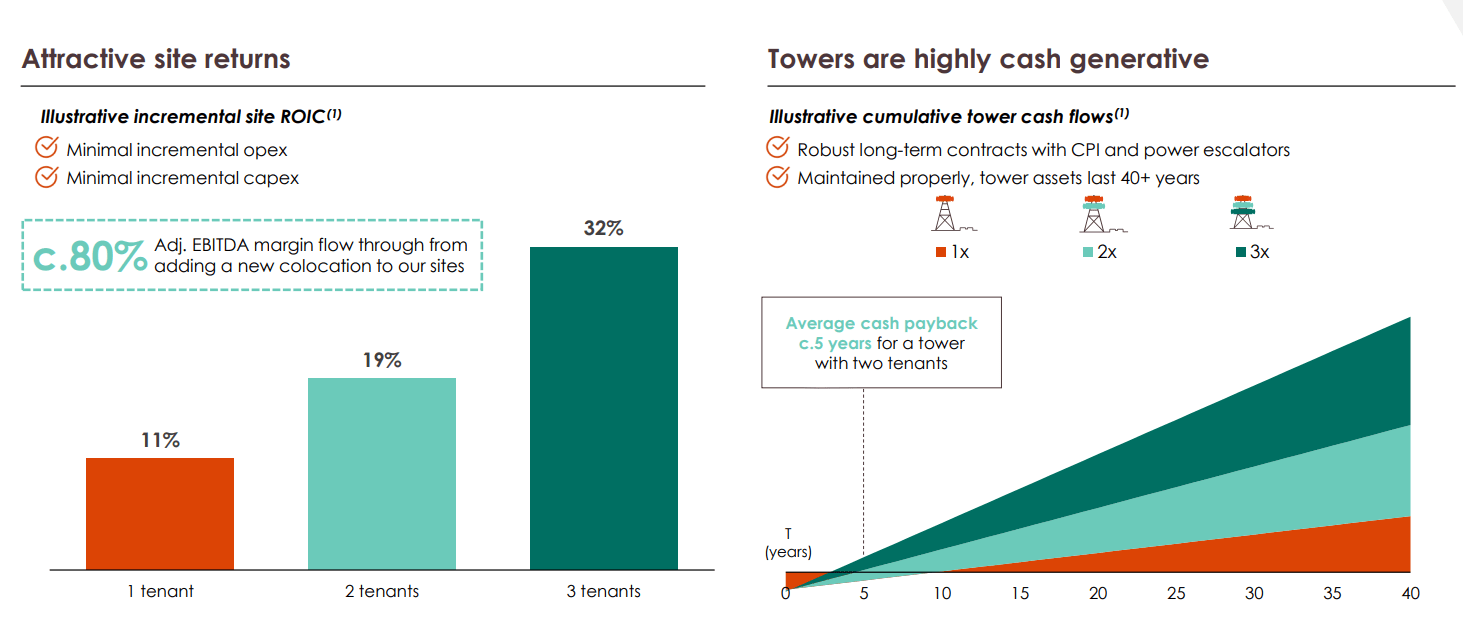

As Helios is a pure play on emerging markets, it has its own advantages and challenges. As a strong company with a foothold in some of the more important African countries it can start focusing on increasing the tenancy ratio (amount of tenants per tower) as its assets can handle 3-4 tenants per power, while also penetrating new markets. The recent completion of the acquisition of cell towers in Oman is a good example of adding a new emerging market to its portfolio outside of Africa. Unfortunately, the pure focus on these emerging markets means Helios is riskier. Not only because it’s a different approach versus operating in Tier-1 countries, but also because currency risk is real and local African currencies can be inherently more volatile than the US Dollar or Euro.

{kind=link}

Helios Towers has its primary listing on the London Stock Exchange where it is trading with HTWS as ticker symbol . The current share price is approximately 109 pence and considering there are 1.05B shares outstanding, the market capitalization is approximately 1.15B GBP. That’s approximately $1.38B (or $1.31 per share) at the current GBP/USD exchange rate . That’s important as Helios reports its financial results in US Dollar and I will use the USD as base currency throughout this article.

The results look good, but the cost of debt will be important

Helios only publishes detailed financial results every six months so I first wanted to look back at its H1 2022 performance and subsequently discuss the Q3 trading update and recent developments.

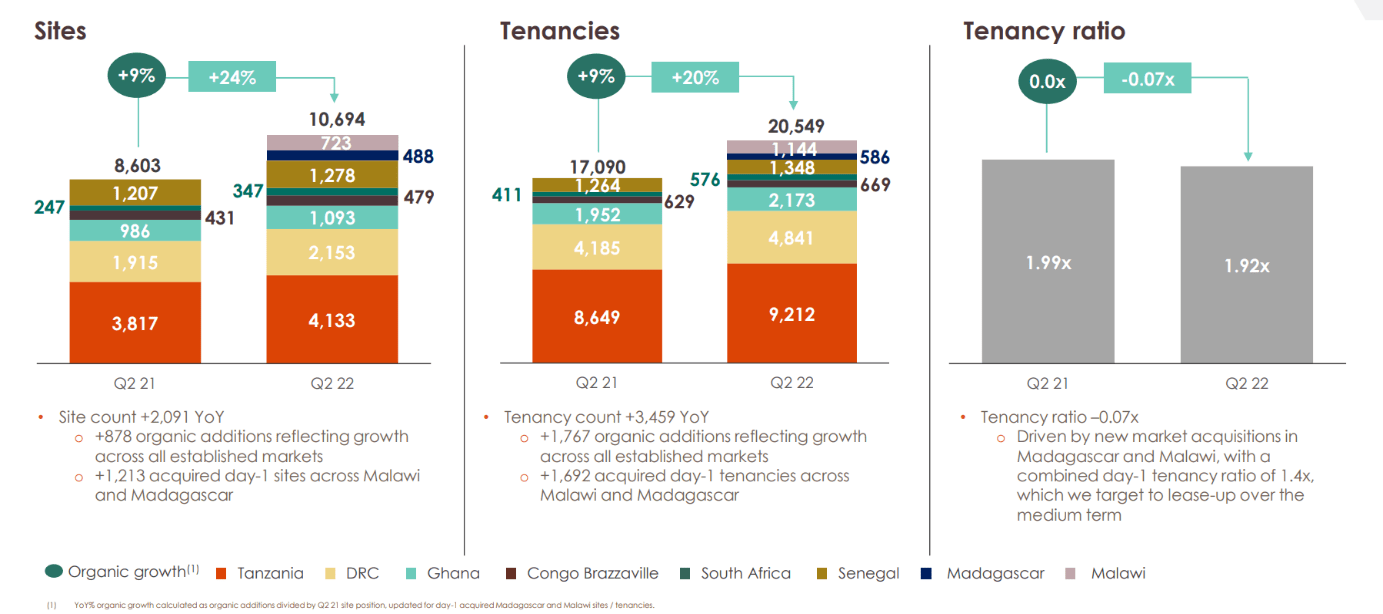

As of the end of the first half of 2022, Helios had just under 10,700 sites with 20,549 tenancies for an average tenancy ratio of 1.92. That’s pretty much in line with 2021 as the company ended the year with a tenancy ratio of 1.99. The higher this ratio, the more efficient the towers are operating as Helios is able to get lease fees from multiple tenants while the operating expenses increase at a much slower pace.

{kind=link}

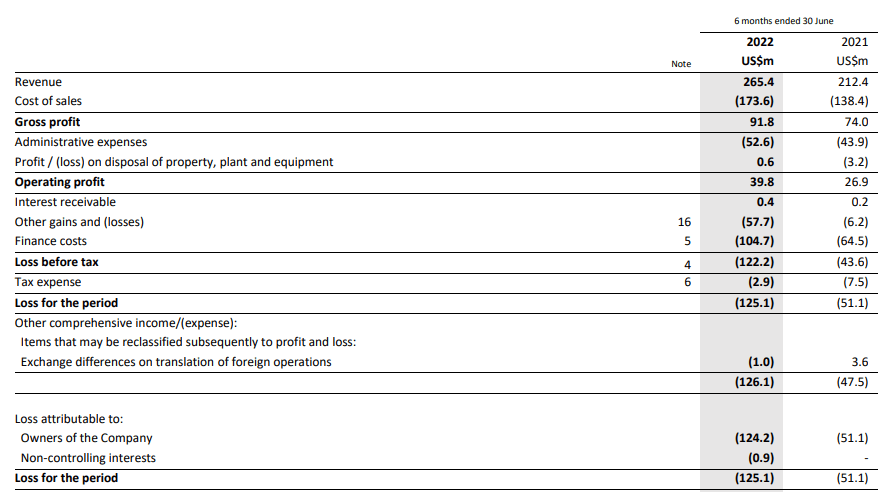

The total revenue in the first half of 2022 was $265M, resulting in a gross profit of approximately $92M. While you may be surprised the gross margin is just around 35%, keep in mind in excess of half of the cost of sales consists of depreciation and amortization expenses. The operating profit was $39.8M and unfortunately after deducting the finance expenses, the pre-tax loss was $122.2M resulting in a net loss of $125.1M of which $124.2M was attributable to the company’s shareholders.

{kind=link}

That’s not immediately something to be too worried about. First of all, the $105M in finance costs includes a charge of almost $37M related to FX changes. The real interest expenses were just $68M.

{kind=link}

Additionally, the $57.7M in ‘other losses’ is related to derivatives and currency hedges. This means about $95M of the finance expenses are related to one-time items and this has no impact on the ability to generate a positive free cash flow.

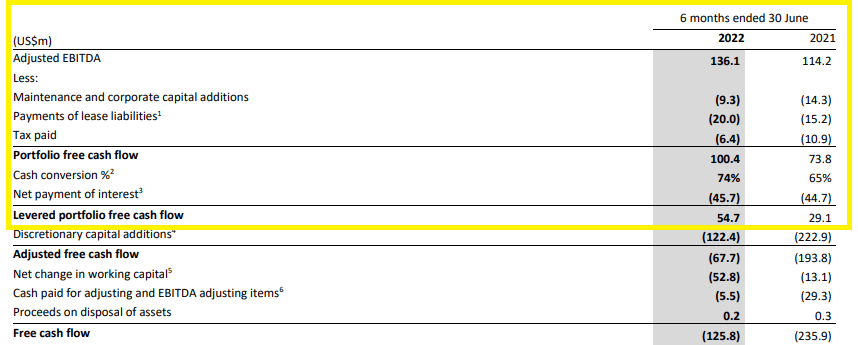

The free cash flow result is what really matters for an infrastructure company like Helios Towers and fortunately the management provided a detailed sustaining free cash flow calculation, starting with the EBITDA.

{kind=link}

Looking at the free cash flow result, Helios Tower generated about $55M, but keep in mind this excludes the interest paid on lease liabilities. We know that represents an additional $11.6M in cash outflow which means the underlying free cash flow was approximately $43M on a sustaining basis. That’s approximately $0.04 per share.

Looking at the Q3 results, the portfolio free cash flow came in at $145.1M which indicates the Q3 portfolio free cash flow was approximately $45M. After deducting the approximately $30M in interest payments, the underlying sustaining free cash flow was approximately $15M . Unfortunately, Helios did not provide a detailed breakdown but I am now anticipating a full-year levered portfolio free cash flow result of approximately $80M, including the interest in lease liabilities.

{kind=link}

The Oman acquisition has now closed

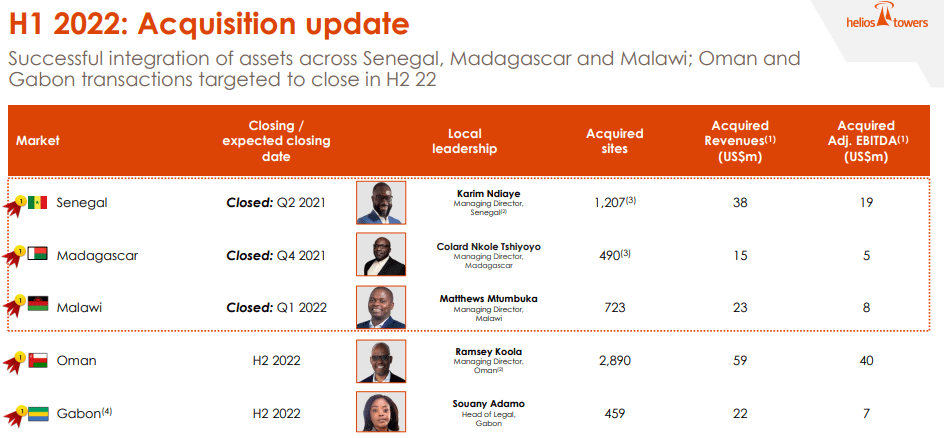

In December, Helios Towers finally closed a substantial acquisition. It completed the purchase of just over 2,500 phone towers for a total amount of US$495M. The original agreement consisted of almost 2,900 towers but the closing only includes 2,519 of them as there some regulatory issues with the rest. Helios Towers still hopes to complete the acquisition of an additional 227 sites from Omantel for US$53M but this remains subject to regulatory clearance.

The delay is not necessarily bad as it allows Helios to focus on its balance sheet in the next few months and quarters to keep the leverage under control. The Oman acquisition wasn’t cheap. The entire set of in excess of 2,800 towers was anticipated to generate $40M in EBITDA. This may increase in 2023 as the original expectation was based on the results before inflation-related hikes, but in any case, Helios is paying about 13 times EBITDA for the acquisition and that is not necessarily a very cheap deal.

{kind=link}

This also means the net debt will have increased as of the end of last year. The net debt will likely come in at approximately $1.65B while the consolidated EBITDA will likely increase towards $320-330M in 2023 for a total debt ratio of approximately 5.

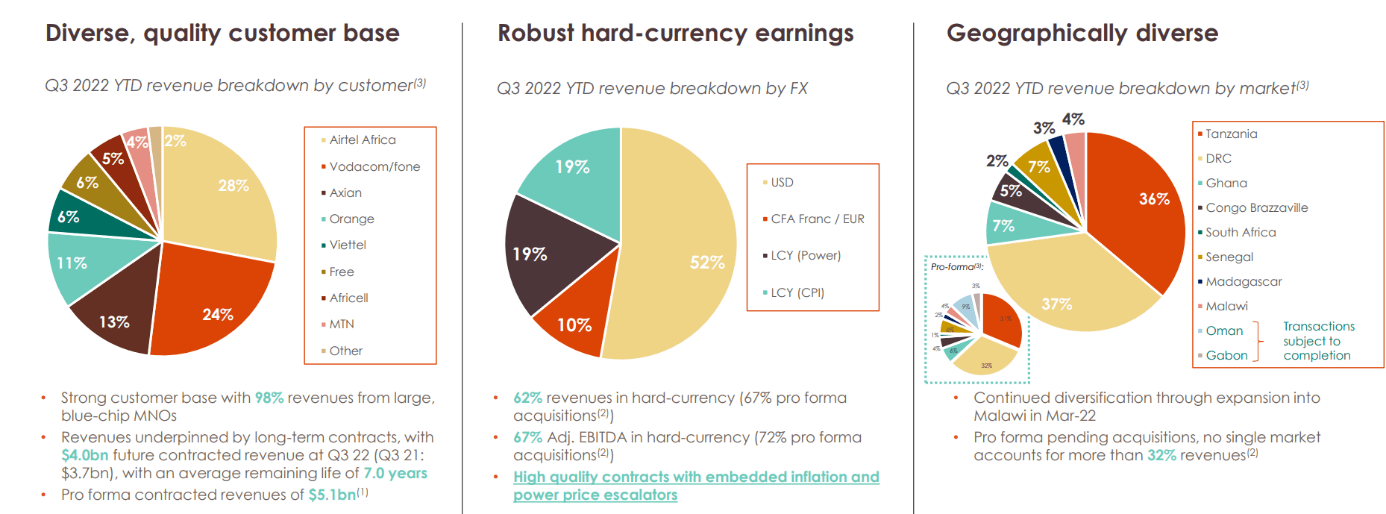

The one element that will be important to keep an eye on is how the FX changes have an impact on Helios’ financial health. The majority of the debt was issued in US Dollar, with just a small portion in Euro and an even smaller portion in a local currency. Meanwhile, Helios generates just over half of its revenue in US Dollar and about 67% of its EBITDA is generated in hard currency (either US Dollar or Dollar- or Euro-pegged currencies).

{kind=link}

Some of the debt was already quite expensive. The 2025 senior notes have a coupon of 7%, so perhaps the interest rate risk upon the refinancing of those senior notes could be pretty low. Perhaps we’ll see a 150-250 basis point increase, but it shouldn’t be too bad. The $300M in convertible bonds with a 2.875% coupon may be tougher to refinance but fortunately the maturity date of those securities is in 2027 so Helios still has plenty of time. The higher cost of debt likely means Helios will no longer be able to pay 13 times EBITDA for future acquisitions so it will be interesting to see the metrics for future acquisitions.

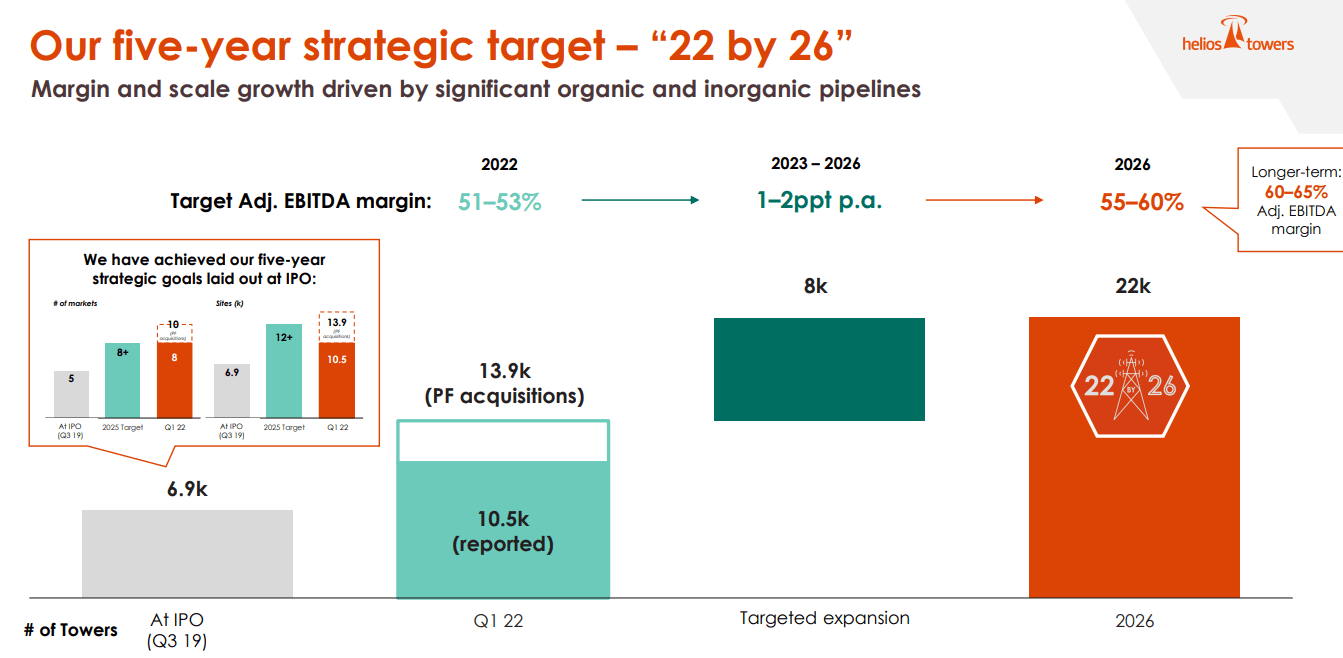

Helios is well underway to increase its amount of sites to 22,000 by 2026 as part of its ’22 by 26’ plan. The recent acquisition in Oman will increase the total amount of sites to in excess of 13,000 and Helios is well underway to further expand its empire.

{kind=link}

I do believe attracting new tenants for the same tower and boosting the tenancy ratio is key here. The additional expenses are minimal and every additional tenant should result in an 80% EBITDA margin on the incremental revenue.

{kind=link}

Investment thesis

I like Helios’s business model but given the current cost of capital I’m not sure the acquisition of the Oman towers was smart. Of course that’s hindsight as this deal was negotiated over a year ago in a different reality. I think Helios has a good chance to continue to perform well but the ‘easiest’ and cheapest growth will have to come from adding more tenants to the same tower as that requires minimal capex for a decent EBITDA contribution.

The company has a self-imposed debt ratio target of 3.5-4.5 and its net debt will likely decrease by approximately 0.5 times EBITDA per year by retaining the incoming free cash flow. The balance sheet doesn’t worry me but I will be very interested in seeing how the company will deal with the maturity of the 7% 2025 bonds in December 2025. Those bonds are currently trading at 95 cents on the dollar for a YTM of in excess of 8.5% which does seem to indicate the market is pretty comfortable despite the B+ credit rating. Unfortunately, the minimum tranche of that bond is $200,000 and that’s a very limiting factor.

If it wasn’t for the pretty steep $200,000 minimum I would likely prefer the 7% senior notes. In 2023, I think Helios Towers should be able to generate $100M in sustaining free cash flow but I don’t expect the net debt to come down as Helios will likely use the cash to further expand its operations by pursuing organic growth. The company currently doesn’t pay a dividend, so it retains 100% of the free cash flow it generates and I consider that to be an advantage.

Including the leases and assuming a FY 2023 EBITDA of $330M, Helios is currently trading at 9 times its EBITDA for 2023 which is definitely not outrageously expensive. More mature Cellnex is trading at about 15 times EBITDA while American Tower is trading closer to 20 times its EBITDA (although the latter is a REIT unlike Cellnex and Helios).

I’m watching with interest but I am in no rush. Helios is cheap but with a 100% focus on Africa and emerging markets it likely deserves to trade at a discount.

For further details see:

Helios Towers: An Attractively Priced Tower Company In Emerging Markets