BORR - Helix Energy Solutions: Mixed Quarter And Guidance - Buy On Weakness

2023-10-30 12:09:52 ET

Summary

- Helix Energy Solutions Group reported mixed third quarter results, with revenues exceeding expectations but weaker GAAP profitability and somewhat disappointing cash generation.

- Helix raised full-year revenue and profitability expectations but lowered free cash flow guidance due to higher working capital requirements and additional capital expenditures.

- The company is facing an estimated upto $100 million earn-out payment in H1/2024 for last year's acquisition of the Alliance Group of Companies.

- With some of the company's most advanced well intervention vessels still employed on lower-margin legacy contracts until the end of next year, I have reduced my expectations for profitability growth next year.

- But even after lowering my estimates and reducing the EV/Adjusted EBITDA multiple, Helix Energy Solutions Group's forward valuation still warrants a "Buy" rating. However, investors should rather consider scaling into the stock on weakness rather than chasing the shares aggressively here.

Note:

I have covered Helix Energy Solutions Group, Inc. ( HLX ) previously, so investors should view this as an update to my earlier coverage of the company.

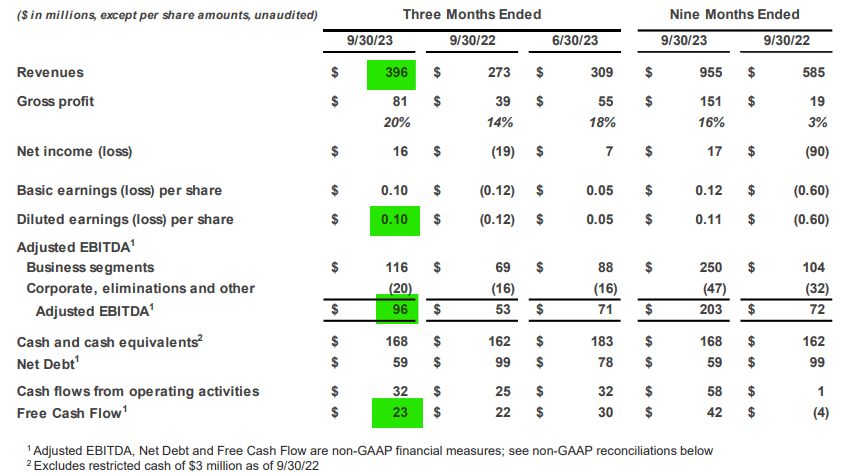

Last week, leading offshore energy specialty services provider Helix Energy Solutions Group, Inc., or "Helix," reported mixed third-quarter results.

{kind=link}

While revenues came in substantially above consensus expectations, GAAP profitability was much weaker than expected by analysts.

However, the miss was solely due to a further $16.5 million increase in the earn-out provision for last year's highly successful acquisition of the Alliance Group of Companies ("Alliance"), which has since been renamed Helix Alliance.

Company Presentation

In total, Helix has accrued $74.1 million in earn-out consideration. Based on Helix Alliance's ongoing, strong performance, I would expect this number to approach $100 million until the payment becomes due in the first half of next year.

Based on the terms of the purchase agreement , Helix may elect to pay the earn-out consideration in cash or common shares.

During the quarter, the company bought back 174,000 common shares at an average price of $10.92 per share, thus bringing year-to-date repurchases to approximately 1.6 million shares.

For my part, I was disappointed by the company's cash generation for the quarter, and particularly by the lowered free cash flow ("FCF") guidance for the full year. Management on the conference call attributed this primarily to higher working capital requirements and to a lesser extent to additional capital expenditures.

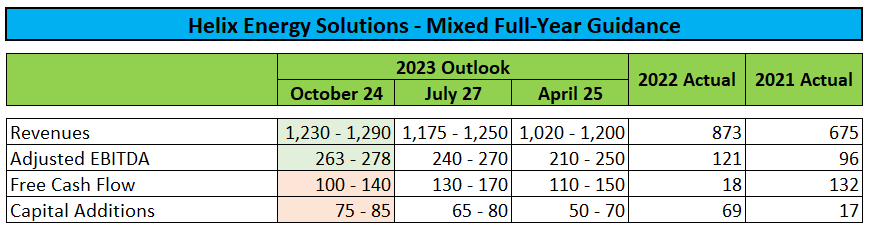

On a more positive note, Helix raised full-year revenue and profitability expectations again:

{kind=link}

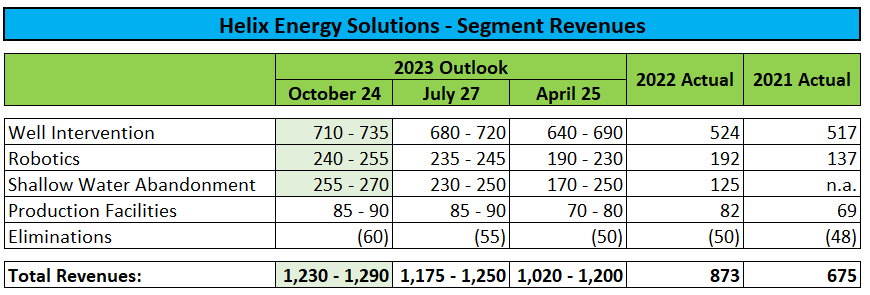

Demand for the company's solutions remains broad-based, with guidance raised again for all three major service segments:

{kind=link}

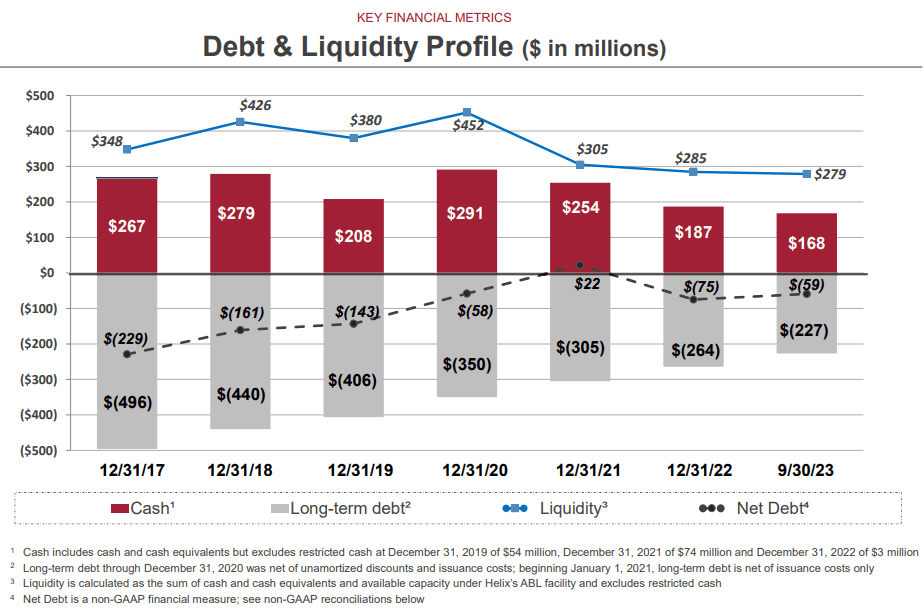

During the quarter, Helix settled the remainder of its outstanding 2023 4.125% Senior Convertible Notes for $30.4 million in cash.

In combination with other debt repayments, capital expenditures, and share buybacks, the redemption resulted in cash and cash equivalents decreasing by approximately $15 million on a sequential basis while net debt was down to $59 million:

{kind=link}

Please note that the company expects to generate between $60 and $90 million in free cash flow in Q4, which would result in Helix returning to a net cash position just 19 months after the Alliance acquisition.

However, this does not account for the substantial earn-out payment due to the former owners of Helix Alliance in H1/2024. Should the company elect to make the upcoming earn-out payment in cash, net debt would increase by an estimated $100 million.

On the conference call, management provided an early outlook for profitability in 2024 (emphasis added by author):

We're in the budgeting process for 2024. So we don't have specific guidance to share at this time with what we see so far, it could be upwards of 10% growth for 2024 over 2023 from our current assets.

This includes legacy below market rates previously contracted that start to roll off by the end of 2024, which would indicate even further growth opportunities in 2025 over 2024.

We've already pointed out that 2024 will have approximately 200 fewer scheduled maintenance days than 2023. Assuming market rates and that we're able to manage costs and execute on our maintenance programs. This could turn into approximately $25 million to $30 million in EBITDA.

Please note that the projected 10%+ in EBITDA growth next year appears to be solely based on much lower maintenance days and not on higher contract rates as some of the company's key assets remain employed on lower-margin legacy contracts as outlined by management in more detail on the call:

We have four major assets currently impacted by legacy rates.

The SH1 is on a 2-year contract to the end of 2024 with a small escalator in rates for 2024 over '23, offsetting higher costs. By 2025, we expect the vessel to be able to achieve market rates, which could be a 50% to 60% increase to the current rates.

The SH2 is on a 2-year extension of a 4-year contract that has a flat rate until the end of 2024. At that time, we expect the vessel to be available at market rates, which could be approximately 40% higher.

The Q5000 has a partial year commitment contract that ends at the end of 2024. There is a year-over-year escalator for 2024 over '23, but we will not see market rates until '25.

The Q7000 is contracted to work in the APAC into mid-2024 before transitioning to Brazil for 12 to 18 months. The rate and cost differences between APAC work and the Brazil work should generate $20,000 to $30,000 a day increase in EBITDA contribution starting in 2025 before reaching market rates in 2026.

Please note that Helix has not provided this level of granularity on its legacy contract commitments before. Particularly the fact that the company's most advanced well intervention vessels Siem Helix 1 and Siem Helix 2 will work at legacy day rates until the end of next year is an unpleasant surprise.

As a result, I am lowering my Adjusted EBITDA expectation for next year from $400 million to $315 million while introducing a 2025 estimate of $375 million:

Company Projections / Author's Estimates

However, the stock remains inexpensive on an EV/Adjusted EBITDA basis based on my estimates for 2025.

Given my expectation for substantially lower EBITDA margins relative to leading offshore drillers like Transocean ( RIG ), Seadrill ( SDRL ), Valaris ( VAL ), Noble Corp. ( NE ), Diamond Offshore Drilling ( DO ), and Borr Drilling ( BORR ), I am no longer assigning the same 6x EV/Adjusted EBITDA multiple to the business.

Author's Estimates

At 5x my 2025 EV/Adjusted EBITDA estimate, my new price target calculates to approximately 14.20 thus providing for almost 45% upside from current levels.

Consequently, I am reiterating my " Buy " rating but wouldn't chase the stock aggressively here. However, I still consider scaling into the shares on weakness an appropriate strategy.

Key Risk Factor

Please note that offshore service stocks remain heavily correlated to oil prices (CL1:COM), so any sustained down move in the commodity would almost certainly result in Helix Energy Solutions' shares taking a hit.

Bottom Line

While Helix Energy Solutions continues to experience strong demand for its services, higher-than-expected working capital requirements in combination with increased capital expenditures have caused the company to reduce full-year free cash flow expectations by $30 million at the mid-point of the provided ranges.

Moreover, with the majority of Helix Energy Solutions' most advanced assets still working on lower-margin legacy rates, profitability is expected to increase just slightly next year.

But even after lowering my estimates and reducing the EV/Adjusted EBITDA multiple assigned to the business, the company's forward valuation still warrants a " Buy " rating.

However, investors should rather consider scaling into Helix Energy Solutions Group, Inc. stock on weakness rather than chasing the shares aggressively here.

For further details see:

Helix Energy Solutions: Mixed Quarter And Guidance - Buy On Weakness