HLFFF - HelloFresh: Increased Visibility To Hitting FY23 EBITDA Target (Rating Upgrade)

2023-09-18 05:00:01 ET

Summary

- HelloFresh's 2Q23 results showed revenues of €1.92 billion and adjusted EBITDA of €192 million, with a decline in active customers but higher order rates and basket values.

- The company's growth is expected to accelerate in FY24, supported by easier year-over-year comparisons and continued traction in its Factor75 business.

- HelloFresh's entry into the B2B catering market and its potential success in selling ready-to-eat meals to corporate clients could be a significant growth driver.

Summary

Readers may find my previous coverage via this link . My previous rating was a hold as I was concerned about HelloFresh ( OTCPK:HLFFF ) ability to meet the $500 million guided FY23 EBITDA target. Hence, I thought it was safer to wait for the 2Q23 earnings call. I am revising my rating from a hold to buy as I gained more confidence in the business's EBITDA trajectory, supported by normalization in CAC and growth in its Factor75 business.

Financials / Valuation

Consistent with the pre-release , the 2Q23 results came as no surprise. However, I feel it is important to highlight some key metrics for the benefit of readers, including the fact that HelloFresh reported revenues of €1.92 billion and adjusted EBITDA of €192 million. For 2Q23, HelloFresh reported 7.3 million active customers, down from 8.1 million in the first quarter. The US fell by 10% and international fell by 8%, consolidating to a blended 9% decline. Even though the total number of active customers decreased, higher order rates and basket values more than made up for the decline.

Based on author's own math

Based on my view of the business, HelloFresh should see its growth accelerate next year as it faces an easier comp in FY23 and also see continuous traction from its Factor75 business (I used consensus estimates for FY23 and FY24). The major delta here is the improvement in margins from EUR 505 million as guided by management in FY23 to near 10% EBITDA margin as I expect CAC and marketing expenses to continue leveling off to pre-covid levels. Combining this with an acceleration in growth should drive margins upward to north of FY21 levels.

Comments

To address the most obvious issue, I do not believe the drop in active users is as severe as it appears. Because of the high volume of travel and low consumer confidence in the second quarter, the company decided to push back some of its marketing until the September back-to-school season, when the company's new ready-to-eat business, Factor75, will have more available capacity. While the number of customers was lower than anticipated, revenue was relatively consistent because of higher-than-anticipated average order values. As such, if we assume that the same marketing efficiency is seen in 2Q23 with the same level of marketing spend, the number of active customers should be higher. Hence, this is more of a "self-inflicted" damage vs. a structural impairment to the business.

Now that the company's management appears to have figured out the secret to the success of its Factor75 business, I am becoming more optimistic about the company's future prospects. I say this because HelloFresh's primary vertical (meal kits) is running out of room for expansion. Note that growth has slowed significantly from its COVID levels of 100% to just 10% with low-single digit growth in active customers. The Factor75 business, on the other hand, is in its formative stages of expansion and market penetration. Importantly, HelloFresh has done significantly well in this business, as they grew it by a factor of 10 over 2 years from FY20 revenue of EUR90 million to FY22 revenue of around EUR913 million (12% of FY22 revenue based on 2023 Capital Market Day ). When Factor75's bottleneck is removed at the end of 3Q23, I anticipate growth to continue at a rapid and impressive clip. This is huge as it means that the follow-quarter growth would be supercharged from an optical level as it tracks against an easy comp in the previous periods. Finally, the improvement in menu variety, product quality, and relative affordability has led to an increase in AOR (average order rates), which is arguably the most important indicator of demand and momentum. As such, I believe the target for Factor75 to reach a total revenue of EUR 2 billion by FY25 is not implausible, especially with the current triple-digit growth rate.

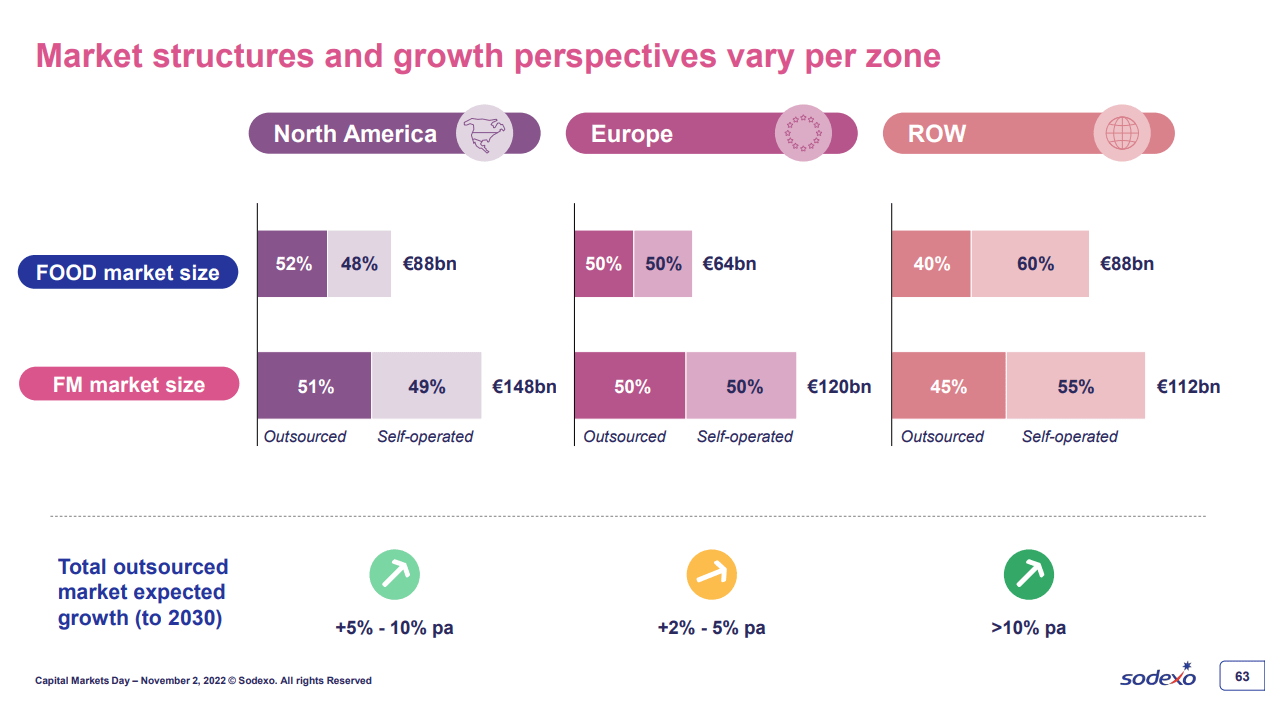

Entering the B2B Catering market and selling ready-to-eat meals to corporate clients for on-site consumption could be a significant growth driver. According to Sodexo, the North American Catering market is valued at €88 billion, with a €64 billion market in Europe. HelloFresh currently focuses primarily on the B2C sector, with a limited B2B presence through Youfoodz in Australia. Given HelloFresh's achievements in B2C and prepared meals, it's unwise to underestimate its potential success in the B2B market, especially with expanded production capacity to meet rising demand.

{kind=link}

Management's reiteration that CLV has increased more than CAC due to improved user retention, order frequency, average order value, and contribution margin is also noteworthy. With that in mind, I would assume that ROI for the new user base is gradually normalizing back to historical levels. This has been verified by comparison to the HelloFresh financials, where the clear operational efficiencies of the business were observable. HelloFresh's contribution margins in 2Q23 were 28.4%, up from 25.6% in the same period a year ago, driven by the improvement in gross margins to 66.2% and lower fulfillment costs (down 230bps to 38.2% as a percentage of revenue). The percentage of sales attributable to marketing also dropped 410 basis points between 1Q21 and now, to 16.5%. If we put together this improving CLTV/CAC element with growth potentially accelerating from here, I believe the outlook for earnings is bright.

Conclusion

I am upgrading my rating on HelloFresh from hold to buy due to increased confidence in the company's ability to achieve its FY23 EBITDA target of €500 million. Despite a decrease in active customers, higher order rates and basket values compensated for the decline. The drop in active users in 2Q23 is likely a temporary effect of marketing adjustments and is not a structural issue. Looking ahead, I anticipate HelloFresh's growth to accelerate in FY24, driven by easier year-over-year comparisons and continued traction in its Factor75 business.

For further details see:

HelloFresh: Increased Visibility To Hitting FY23 EBITDA Target (Rating Upgrade)