HELFY - HelloFresh: Issues With This Growth Story

2023-05-23 21:52:16 ET

Summary

- HelloFresh SE provides meal kit solutions that enable customers to prepare home-cooked meals using their recipes.

- Revenue has grown at a CAGR of 77%, reflecting an impressive marketing strategy.

- EBITDA-M is a disappointing 3%, with the scope to potentially reach c.6%.

- HelloFresh is in for a tough 12-24 months as economic conditions lead to slowing growth.

- The company does look cheap and could be a speculative buy, but headwinds imply caution.

Investment thesis

Our current investment thesis is:

- HelloFresh's target market is consumers who are looking for healthy food options and are willing to pay a premium for delivered ingredients.

- Its growth strategy has been fantastic although the recent quarter's performance has been poor.

- HelloFresh's margins are unattractive, although, with scale, we see some value if margins can increase slightly.

- HelloFresh looks cheap but the difficulties in the coming year make the company unattractive.

Company description

HelloFresh SE ( OTCPK:HLFFF ) provides meal kit solutions that enable customers to prepare home-cooked meals using their recipes. The company offers a variety of options, including premium meals, double portions, and add-ons like soups, snacks, fruit boxes, desserts, ready-to-eat meals, and seasonal boxes.

HelloFresh operates in multiple countries, including the United States, Australia, Austria, Belgium, Canada, Germany, France, Luxembourg, the Netherlands, New Zealand, Switzerland, Sweden, Denmark, Norway, Italy, Japan, and the United Kingdom.

Share price

{kind=link}

HelloFresh's share price (Google Finance)

HelloFresh's share price made impressive gains in the years leading up to the end of the pandemic, as its aggressive expansion introduced a revolutionary product to the market. Unfortunately, investors turned sour, with the share price declining to its 2020 level.

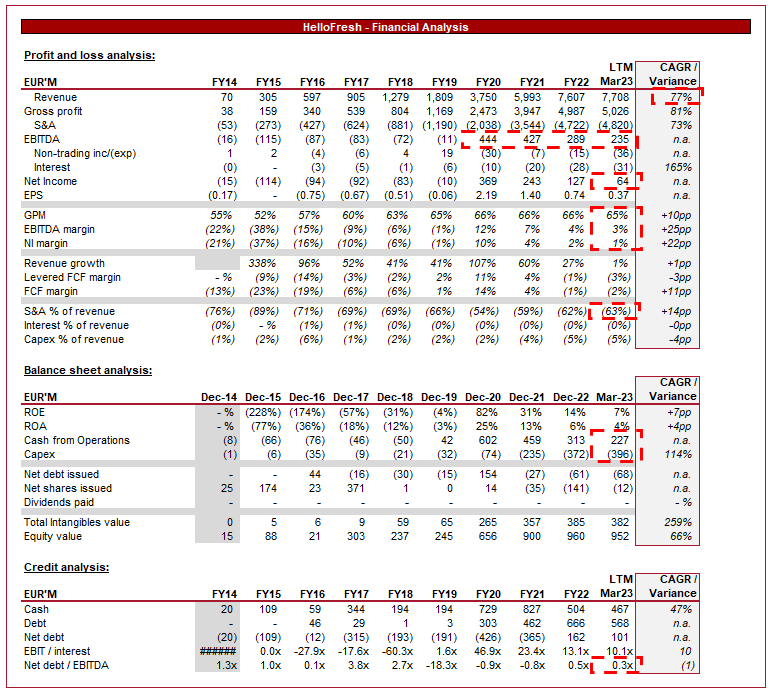

Financial analysis

{kind=link}

HelloFresh financials (Tikr Terminal)

Presented above is HelloFresh's financial performance for the last decade.

Revenue

Revenue has grown at a CAGR of 77%, driven by an aggressive growth strategy by Management. This involved an extensive social media campaign, as well as introductory discounts. Further, it should be acknowledged that the product is seemingly good enough to encourage repeat purchases.

The development of the meal kit solution market and its long-term outlook is driven by the following factors.

Changing Consumer Preferences

Consumers are increasingly looking for convenient ways to cook meals at home, driven by factors such as cost savings, health consciousness, and quality control. The rapid increase in delivery businesses such as DoorDash ( DASH ) is a reflection of the demand for convenience, but an increasing proportion of individuals are demanding healthier options.

HelloFresh has committed heavily to selling its offering as convenient and time-consuming. It offers flexible delivery schedules to accommodate customers' preferences and ensure freshness. Also, this convenience extends to its app. HelloFresh's mobile app allows customers to manage their subscriptions, select recipes, and track deliveries, as a means of enhancing convenience.

Further, we have experienced a global shift toward remote working, which has increased the proportion of households who are in a position to cook meals. This has increased the demand for meal kit delivery services, as HelloFresh provides enough convenience to work alongside a busy lifestyle. This has the characteristics of a long-term change in consumer behaviors, which suggests the runway for growth remains long.

Our concern here is that the company is essentially targeting the Venn diagram of people who do not want deliveries / takeout food, but are also not willing to purchase groceries themselves. Further, with a GPM of 65%, HelloFresh is charging a steep premium relative to groceries. We were surprised to see the prices the company charges, which is a steep premium relative to cheap meals and cooking. This is clearly an upmarket offering. Due to these factors, we question how large this market can be at a recurring revenue level (It is not clear what portion of revenue is genuine recurring customers, and what people are trying the service out).

Health and Wellness

Rising awareness of the importance of nutrition and wellness has led consumers to seek healthier food options. Similar to the points above, this is not an isolated factor. Those who are health conscious could easily buy ingredients themselves and curate the perfect meal. However, if an individual has a busy job, yet would prefer to consume a wide variety of healthy foods, HelloFresh suddenly represents a more attractive option than deliveries or groceries.

Many consumers follow specific dietary restrictions or have food allergies, yet for whatever reason, cannot make the foods they would like to consume. The biggest example of this is the rise of plant-based diets, which represents a significant trend in the food industry. There is an increasing number of meat eaters who are trying these foods. HelloFresh can capitalize on this trend by expanding its plant-based meal options and thus increasing the potential number of customers it can reach.

As the following illustrates, the number of meals has increased rapidly, with HelloFresh committed to expanding this offering.

Recipes (HelloFresh)

Our key concern with this point is that HelloFresh must rapidly innovate long term otherwise it will face churn as consumers find the meals they like and buy the ingredients themselves.

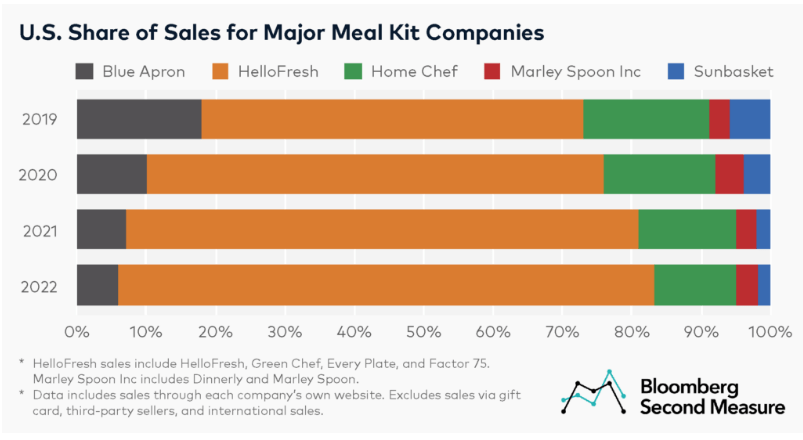

Competitive Landscape

The meal kit delivery industry has quickly become highly competitive, with new players entering the market regularly. HelloFresh has a first movers advantage, but with other companies spending significantly, we are seeing a race to the bottom. HelloFresh currently remains the largest player in the US.

{kind=link}

Market share US (HelloFresh)

Localization and Regional Expansion: HelloFresh has the opportunity to expand its operations in various regions globally. By adapting its meal offerings to local tastes and preferences, partnering with regional suppliers, and tailoring marketing efforts, HelloFresh can effectively penetrate new markets and gain a competitive edge.

Our concern is that HelloFresh faces reduced revenue growth as new customers are now "shared" among a greater number of incumbents. Further, given this is a growing market, we are seeing competition in the form of marketing spending and discounts, which could contribute to tighter margins.

Marketing

HelloFresh's growth strategy is very impressive. The company targeted strategic partnerships with retailers, influencers, and other food-related businesses to enhance HelloFresh's brand visibility. There was a time when you could not watch a YouTube video without seeing a HelloFresh ad. Our issue with this is customers are seemingly coming and going, as its S&A spending as a % of revenue is an astronomical 63%. HelloFresh is forced to maintain significant marketing spending in order to keep growth strong, which is unhealthy at its current size.

Economic considerations

Current economic conditions represent a key risk for the business.

With inflation remaining elevated, consumers are reducing spending where possible as a means of defending finances. Across many sectors, such as retail, we are seeing declining spending.

Consumers are unlikely to cease purchasing food to eat, yet HelloFresh is grinding to a halt in the LTM period. Active customers have declined by 410k Q/Q, reflecting this. This suggests consumers see HelloFresh as a luxury and potentially something "worth trying", but are unlikely to remain with the service if things get tough. This is concerning and unsurprising given the prices HelloFresh charges.

Looking ahead, we suspect HelloFresh will continue to lose customers and see reduced new customers, as consumers are deterred by prices and the value proposition.

Margin

HelloFresh's margins are surprisingly bad. Despite charging a significant premium to its input costs, the company's 65% GPM translates to an EBTIDA-M of 3%.

This is due to several factors, the largest of which is its aggressive marketing strategy. To support growth, the company is committed to spending a significant amount on customer acquisition. This is fine during the growth phase of a business but HelloFresh is at almost EUR 8bn and achieved almost no transition toward attractive profitability. In Q1, marketing spend has jumped as % of revenue, suggesting it is unable to fight against macro conditions.

Marketing spend (HelloFresh)

Further, the company is still seeing the impact of inflationary pressures on costs, with Procurement costs increasing as a % of revenue. The good news is that this looks to be subsiding, with fulfillment costs declining.

Procurement costs (HelloFresh)

Fulfillment costs (HelloFresh)

Management is attempting to offset these factors with increasing AOV, however, this will only compound the loss of customers. We do believe this to be the correct decision but the company still loses.

AOV (HelloFresh)

Overall, we believe EBITDA-M improvement is possible, with the company having scope to reach 5-7%. This is based on improving AOV and a decline in inflationary pressures in the coming quarters. The only issue is that this may come at the cost of customer acquisition and churn.

Balance sheet

HelloFresh remains conservatively financed, with an ND/EBITDA ratio of 0.3x. With scope for margin improvement in the coming years, we are not concerned with solvency.

HelloFresh's capex commitments have increased in recent years as the company expands internationally. This has contributed to reduced cash flows, which could continue in the coming years.

Valuation

HelloFresh is currently trading at 17x LTM EBITDA. Given the growth trajectory of the business, this looks reasonable despite the slim margins.

Although this paper has been negative, there is the potential for a strong business here. If we assume EBITDA-M can reach 6%, and FCF 10%, the company would generate c.10% of its EV annually. Further, with strong double digital growth, rapid multiple contraction is possible. This is why, at its current price, we think this stock could be a speculative buy in the next 2 years.

Our issue is what will occur in the next 12-24 months. With growth slowing rapidly, and margins facing contraction due to fixed overheads, HelloFresh is facing an extremely tough year. This will likely turn sentiment negative and potentially cause negative pricing action.

Final thoughts

HelloFresh is a great case study for effective marketing. The company is essentially selling ice to Eskimos. Consumers could google a recipe, go to their local grocery, and replicate a HelloFresh product at a fraction of the cost. Yet the company has 7.7bn in revenue.

Our key concerns are the lack of customer stickiness, price differential to alternatives, poor margins, and growth slowdown. With these factors taking prominence in the coming 12-24 months, we suggest investors avoid this stock.

For further details see:

HelloFresh: Issues With This Growth Story