HLFFF - HelloFresh: Strong Turnaround In EBITDA But Investors Should Stay Cautious

2023-05-23 08:34:29 ET

Summary

- Strong 1Q23 results and confident EBITDA performance have positively impacted share price.

- HLFFF ability to strategically raise prices across regions and utilize effective pricing tools can contribute to improving EBITDA margins.

- Expansion opportunities lie in penetrating new meal-kit markets and the flourishing ready-to-eat industry, with the new Arizona facility expected to drive robust growth.

Summary

For readers that are not familiar with HelloFresh ( HLFFF ), please refer to my previous post . Previously, I discussed why the share price fell following the 4Q22 earnings, citing the weak 1Q23 adj. EBITDA guidance as a dealbreaker. To the market's and my surprise, HLFFF reported strong 1Q23 results, including a meaningful EBITDA beat driven by lower-than-expected marketing and fulfillment costs. Revenues came in broadly in-line with consensus expectations at ~EUR2 billion but adj. EBITDA outperformed at €66 million vs its own guidance of EUR30 to EUR40 million. Management also implicitly guided to a strong EBITDA performance in 2Q23 as well (based on my own calculations). My previous concern about adj. EBITDA performance has been quickly transformed into a strong driver of share price performance. However, I am still concerned about the company's ability to meet its $500 million guided FY23 EBITDA target, as significant acceleration is required in 2H23 (although management expressed optimism about 2H23 profitability). In my opinion, the safer move today is to wait for the 2Q22 earnings call before deciding whether or not to invest. Because the 2Q23 earnings call will be held sometime in 3Q23, we will be able to obtain more information about 3Q as well. Overall, I reiterate my hold recommendation.

Pricing and margin

While I am wary, I am still optimistic that HLFFF EBITDA margin will continue to improve as the business is continuing its streak of price increase across various regions in the UK, US and Netherlands – which has improved group AOV to 61.4 from 55.4 (management mentioned that half of it is due to pricing impact). This, I believe, is a core reason why management is so confident on profitability this year as the increase in prices have very high incremental margins. The immediate pushback is that price increase will hurt volume as consumers are extremely price sensitive in today’s inflationary environment. That is true if HLFFF were to raise prices organically. However, I believe there are multiple tools (mentioned in March Capital Markets Day) that HLFFF can utilize to “hide” this price increase from consumers. For instance, increasing fee for peak period delivery and lower fees for non-peak. The “effective pricing” should end up being margin lucrative. An introduction of shipping fee for certain slots would also do the trick. Also, I think the price increase action is not isolated to HLFFF only, other competing players are also increasing prices . On a like-for-like basis, I expect HLFFF, the largest player in the US, to be one that can raise prices more aggressively given their scale – which allows to offer more value to consumers (SKUs, delivery time, quality, etc.).

Growth

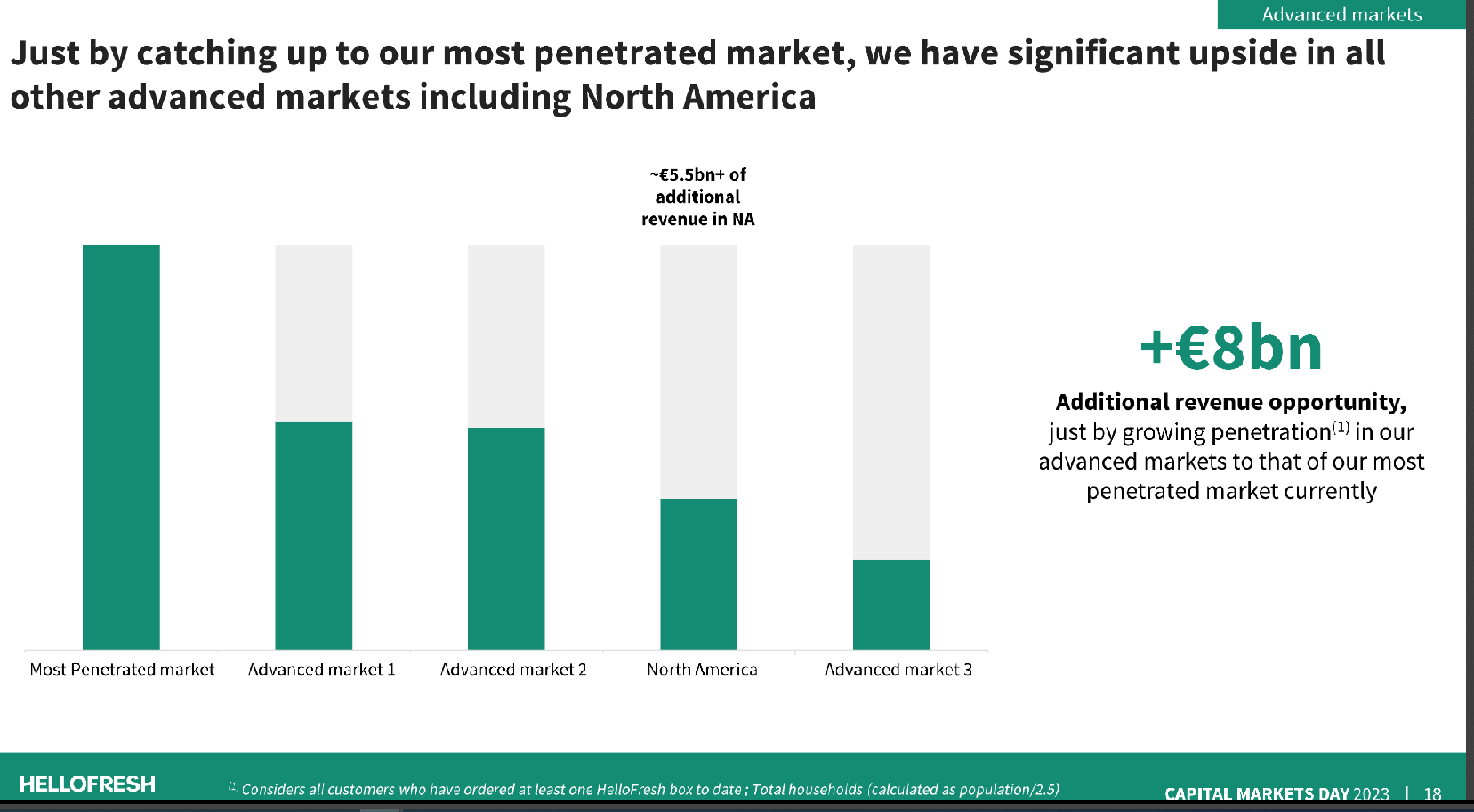

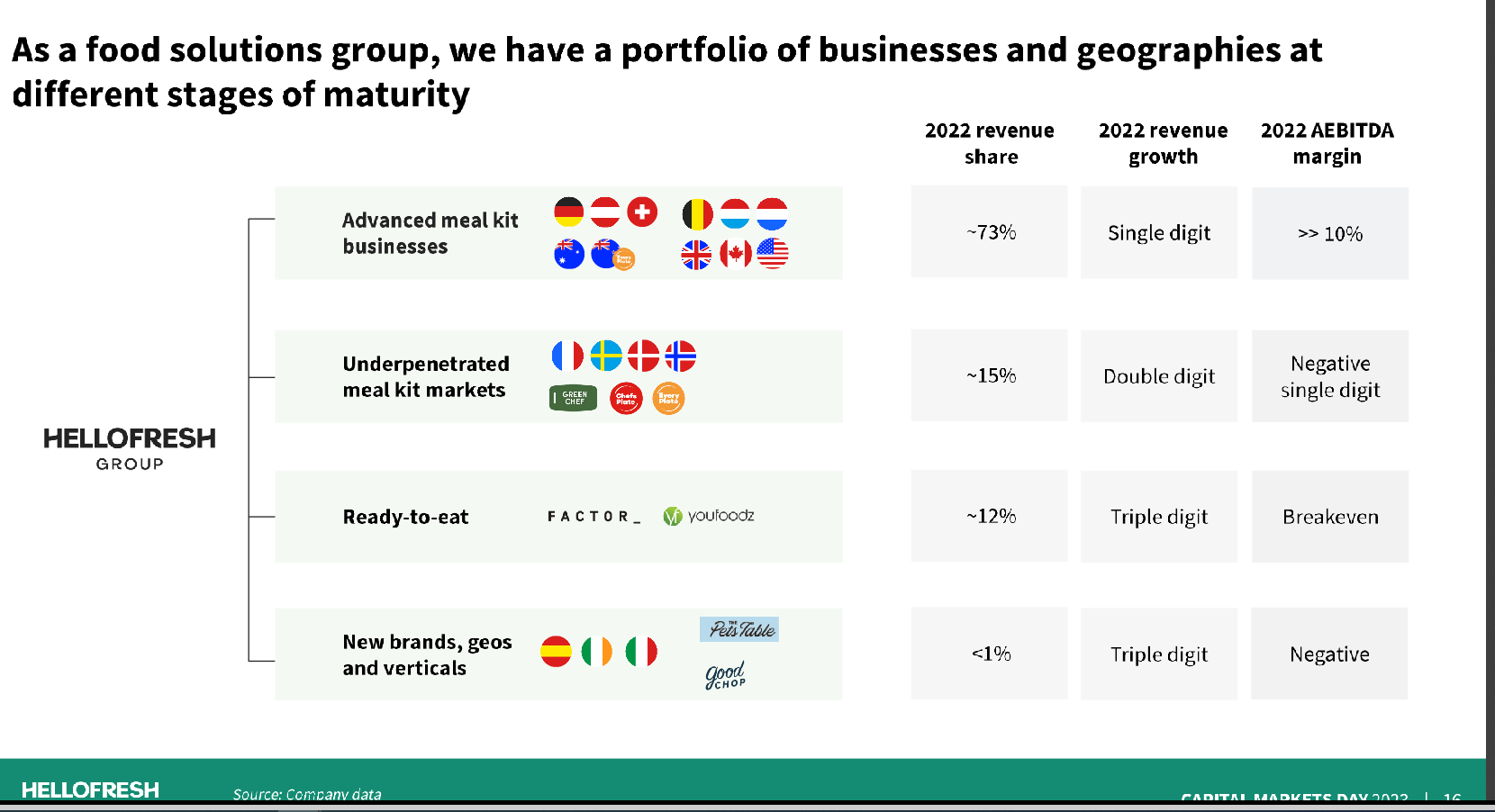

The growth forecast for HLFFF consists of two parts. First, HLFFF meal-kits segment is expected to grow at a slower rate as HLFFF's core large markets (mentioned in 2023 Capital Markets Day), where the company has a substantial presence, are facing much slower growth vs the past at only single-digit rates in FY22. Nonetheless, HLFFF is doing its best to extend the growth runway by penetrating into new markets (Europe, as per 1Q23 earnings call), and if the newly introduced meal-kit markets can bring perform just as good as the core markets, I believe HLFFF can continue growing at a rate well above the single digits on a blended basis for the short-to-med term. That said, it is difficult to underwrite at present given HLFFF's sub-scale position in the new markets (remember that scale matters).

{kind=link}

In stark contrast to the meal-kits market, the ready-to-eat segment is flourishing and offers the business an opportunity to diversify away from its legacy meal-kits business, with revenues growing to around €900 million in 2022 (12% * FY22 revenue of 7.6 billion), and is still growing at triple digits.

{kind=link}

Especially once the new Arizona facility begins operations later this year, I anticipate continued robust expansion. While management did not comment on how much the growth rate would have been if there was no capacity constraints, their hint that it would have been several times the current run rate suggest a sizable impact. Therefore, it appears that management's optimism regarding H2 profitability is also supported, in large part, by a rapid ramp of ready-to-eat capacity in the United States.

Risks

The primary risk I see for HLFF is the nature of its product. In my opinion, meal-kits and ready-to-eat meals are “wants” and not “needs”. When push comes to shove a deep recession, I expect households to cut back on these items and revert back to cooking which is a cheaper long-term solution.

Conclusion

HLFFF strong 1Q23 results and confident stance on EBITDA performance have positively impacted its share price. However, I do have some concerns about meeting the guided FY23 EBITDA target. That said, it is not impossible as HLFFF's scale and value proposition position it well to raise prices. HLFFF's expansion into new markets (meal-kits) and the flourishing ready-to-eat industry also offer growth opportunities. Overall, I believe waiting for the 2Q23 earnings call before making an investment decision seems to be the right move here as we can confirm 2Q23 EBITDA performance, and also gain insights in 3Q23 trends.

For further details see:

HelloFresh: Strong Turnaround In EBITDA, But Investors Should Stay Cautious