HLFFF - HelloFresh: Weak Q1 2023 Guide Huge Acceleration Needed To Hit FY23 Guide

2023-03-08 11:43:36 ET

Summary

- HLFFF 1Q23 guidance is weak, with adjusted EBITDA expected to fall by roughly half due to revenue and expense pressures.

- HLFFF needs to achieve a massive acceleration in the second half of 2023 to meet even the low end of its FY23 guidance range, which carries a hefty burden of risk.

- It would be helpful if the company shared more information about their cohorts and customer retention rates at the upcoming CMD.

Summary

HelloFresh ( HLFFF ) delivers meal kits on a subscription basis to consumers. The data-driven approach and unique technology developed by the company are two of the foundational pillars on which the business model stands. This is a game of optimizing CAC vs CLTV, as such it is crucial to secure optimized marketing spend. The next step is distribution, where the meal kits must be sent from A to B in a timely manner while taking the shortest and most efficient route possible. Theoretically, the business model has a lot going for it, including a large TAM, a clear path to profitability, and highly predictable revenue streams (subscription model). Customized products, recipes, menus, etc. add a lot of complexity to the business model, though. The core value is that it offers customers a new, more efficient model that they can adopt to cut costs and improve efficiency. Of course, the model also benefits from the growing interest in healthy eating, the convenience of online food ordering, and the rising expectations of discerning diners for honest, transparent labels.

Shares of HLFFF were down after the company reported earnings on March 7th , which I attributed to the company's very disappointing FY23 guidance. Importantly, I think another punch to investors was the 1Q23 guide, that adjusted EBITDA for 1Q23 would fall by roughly half, to between €30 million and €40 million. The 1Q23 underperformance appears to be the result of both revenue and expense pressures. For 1Q23, active customers are expected to decrease by the mid-single digits %, while order values are expected to increase by only the low single digits %. In the meantime, HLFFF is also accelerating its advertising efforts up front and its capital expenditures have not returned to their normalized levels. Given these factors, it would mean that FCF in 1Q23 is expected to be negative. This is quite a U-turn on profitability expectations in a sense FCF turned positive to negative (you can imagine how many investors were shocked by this as HLFFF was supposed to be a profitable business). This also means that 2H23 is carrying a hefty burden of risk if HLFFF is the case, as massive accelerations are required to meet these implied numbers.

HLFFF has a lot of work to do in the second half of the year to achieve even the low end of its FY23 guidance range, so I do not think it is a good time to buy the stock. This is especially true given that management has guided predicted a lackluster 1Q23 and a negative first half FCF.

4Q22 review

HelloFresh's quarterly customer growth and 2023 forecast were both lower than anticipated. The only bright spot in this report was management's reiteration of FY25 guidance for €10 billion in revenues and an adj EBITDA margin of 10-15%. While this helped ease investors' concerns about low customer growth, I remain curious about how long-term the HLFFF business model is sustainable in terms of customer retention (i.e., churn rates) and what the normalized CAC is.

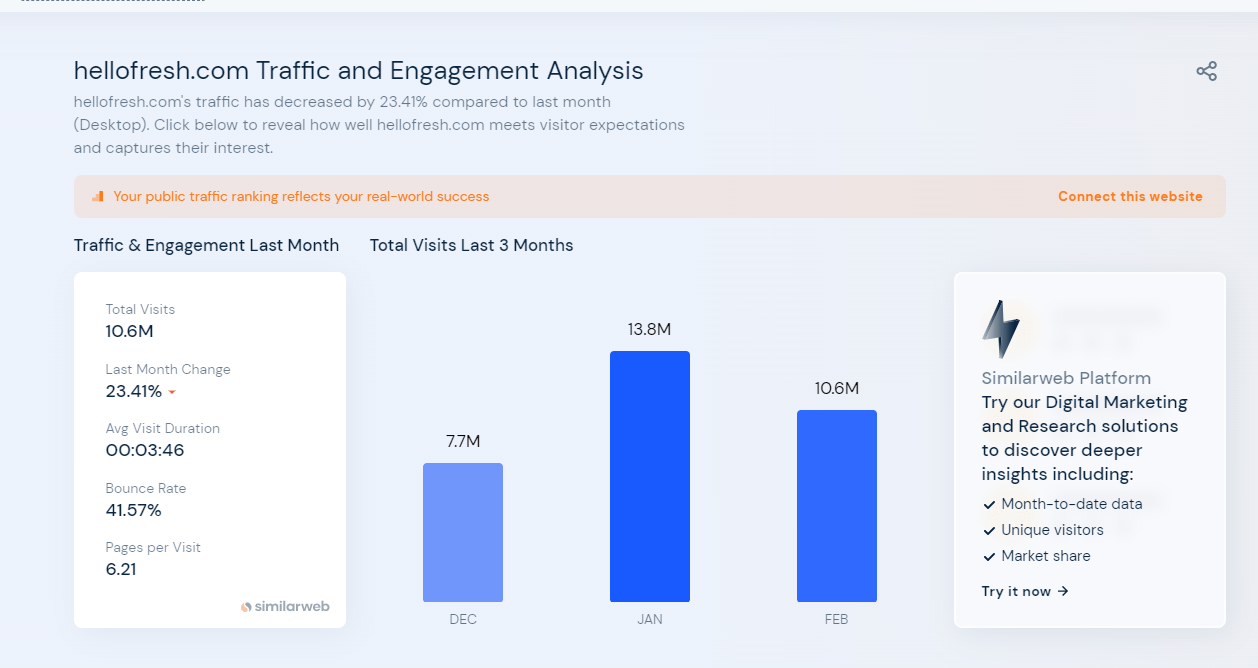

February web data is look

In my opinion, the massive sequential drop in HLFFF's Similarweb data was another factor that scared off investors. Consensus are now pricing in the weak 1Q23 that management has been forecasting (and might also be extrapolating this forward until end of 1H23). Since January is traditionally the quarter's strongest month for actives, this guidance likely reflects the noticeably weak month-over-month trends, indicating that high customer churn is expected to persist into March.

{kind=link}

More data needed

I think it would be helpful for HLFFF if they shared information about their cohorts. I'm looking forward to the CMD on March 23 and hope that there will be some discussion of customer retention rates. Despite HelloFresh already being a profitable business, the company's cohort and customer retention levels have been the subject of much debate for many bulls and bears. If I am the management, in the upcoming CMD, I would shed more light on improving customer retention, which could act as a catalyst if it causes the consensus to revise its earnings estimates upward from being too bearish on retention rates.

Conclusion

While HLFFF business model has the potential to be successful in the long term, there are some concerns about its sustainability and profitability. The company's disappointing FY23 guidance and negative FCF in 1Q23 are alarming, and management has a lot of work to do in 2H23 to achieve even the low end of its guidance range. Additionally, the drop in Similarweb data and high customer churn rates are concerning. It would be helpful if HLFFF shared more information about their cohorts and customer retention rates at the upcoming CMD. Until then, it may be wise for investors to wait and see how the company performs before considering buying the stock.

For further details see:

HelloFresh: Weak Q1 2023 Guide, Huge Acceleration Needed To Hit FY23 Guide