JEPI - HELO: A New JPMorgan Fund For Risk-Averse Investors

2023-11-27 08:10:39 ET

Summary

- JPMorgan Hedged Equity Laddered Overlay ETF is a newly launched fund that invests in large-cap American stocks with low volatility and uses a laddered options strategy for downside protection.

- The fund's holdings are similar to JPMorgan's other funds and may use the same algorithms for stock selection.

- HELO uses put spread positions as part of its options strategy, which is cheaper than buying protective puts alone. The fund's calls are deeply in the money, limiting its upside potential.

- The fund hasn't announced a distribution target yet so income investors may want to wait before investing.

JPMorgan Hedged Equity Laddered Overlay ETF ( HELO ) is a newly launched fund given to us by the company that brought us highly popular funds like JPMorgan Equity Premium Income ETF ( JEPI ) and JPMorgan Nasdaq Equity Premium Income ETF ( JEPQ ). The fund's description says that it will invest in large cap American stocks identified by the fund's proprietary formulae to be good buying opportunities which also have low volatility while applying a "laddered options strategy" to protect against downside risks.

The type of stocks held by this fund are very similar to those held by JEPI which isn't surprising since both funds aim to hold stocks that have similar characteristics such as large cap, US-based, low valuation multiples and having low beta, low volatility in relation to the market. Since both funds use JPMorgan's "proprietary" methodology to pick stocks, they might be even using the very same algorithms. The fund is not very open and clear about what algorithm it uses and whether is uses a different algorithm for different funds other than that it is developed and owned by the company.

The fund holds 175 stocks, all of which are part of the S&P 500 index ( SPY ) and the fund's top 10 holdings are about the same as S&P 500's top 10 stocks. You will see a lot of familiar names like Microsoft ( MSFT ), Apple ( AAPL ), Amazon ( AMZN ), Tesla ( TSLA ) and Nvidia ( NVDA ) in top 10 holdings of the company's list which makes me wonder if it is really aiming to get a portfolio of "low beta" and "low volatility" stocks. One can't help but wonder if JPMorgan's new proprietary algorithm simply picks the top 175 stocks in the S&P 500 index by weight and that it may not be all that fancy and complicated. It's totally fine if the company is just using indexing approach but it should say so to the investors instead of saying it uses some sort of special algorithm to pick the best stocks with low beta and low volatility.

HELO Top 10 Holdings (Seeking Alpha)

The fund's paperwork doesn't do much in terms of describing its options strategy which is the bread and butter of the fund and what is supposed to separate this fund from others. In order to have a better understanding what the fund actually does with options, you have to dig a bit deeper. We went to the fund's webpage and downloaded a full list of its holdings including all the options.

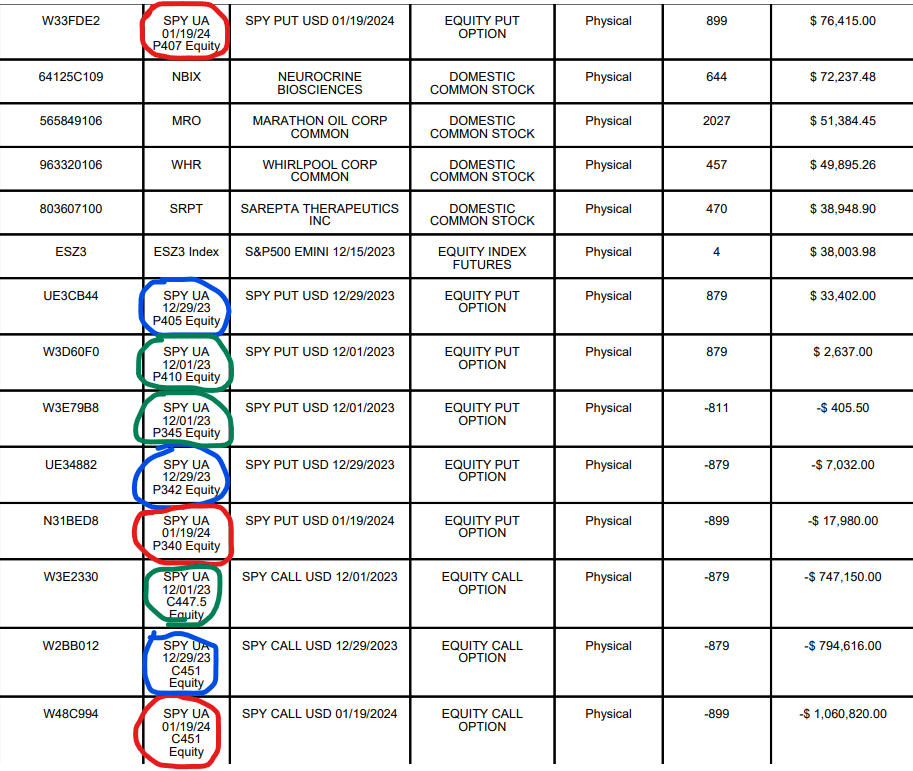

Below I added colored highlights to the list of HELO's options holdings in order to better demonstrate what the fund is doing with options. Green color coding represents options expiring on December 1st, blue color coding represents options expiring on December 29th and red color coding represents options expiring on January 19th (2024). Part of the "laddered options strategy" comes from having different options plays with varying expiration dates. What the fund does is similar to a collar approach but there are differences. In a traditional collar strategy, you write covered calls and use some of your premiums to buy protective puts as insurance in order to protect yourself against a market crash. Since market crashes are rare, most protective puts expire worthless. This fund applies this strategy with a twist. Instead of buying protective puts, it buys protective put spreads. For example, for December 1st expiration, it holds a protective put spread position of SPY $410-345. For December 29th, it holds a put spread position of SPY $405-342 and for January 19th, it holds a put spread position of SPY $407-340.

{kind=link}

HELO's Options Plays (JPMorgan)

This approach is not totally unique to this fund either. Recently I wrote an article covering Simplify Hedged Equity ETF ( HEQT ) which uses a similar approach. You can read it here: HEQT: A Young Fund With Promising Results So Far.

The idea is that it is a lot cheaper to buy put spreads as opposed to buying puts alone. For example, buying a put option of SPY $430 expiring on January 19th costs $1.95 per contract and it only kicks in if SPY drops below $430 during this time. You are basically paying a fee of 0.43% for a 2-month protection which may or may not kick in. Annualized, this comes to close to 3% fee for protection. When you sell covered calls, you are already giving up a big chunk of your upside potential in exchange for dividends and we already know that most covered call funds underperform the markets, so why add another 3% drag to your performance?

SPY Put Pricing (Options Profit Calculator)

Instead, if you sell $430-400 puts spreads, your cost drops from $1.95 to $1.26. Now you are still protected all the way from $430 to $400 while paying a much smaller price.

Put Spread Pricing (Options Profit Calculator)

As a matter of fact, this fund's protective put spreads are even further out of money than this. We are seeing its protective put spreads kicking in around $410 or below so SPY would have to drop significantly from here before those spreads help out. On the positive side, the fund paid only about 30 cents per contract for each of these put spreads which is a very small price.

The worrisome part is where the calls are sold though. December 1st calls had a strike price of $447, while December 29th and January 19th calls had a strike price of $451 each. Basically, all the calls sold by the fund are deeply in the money and the fund's participation in any upside the market may have from here on will be very limited for the next couple months. Perhaps the fund's approach is too conservative at the moment.

At this, this fund is a bit more transparent than JEPI in terms of its options plays. JEPI lists its options play as ELNs (equity linked notes) and doesn't specify details such as strike prices and expiration dates on them which has been a main point of complaint from investors.

On the other hand, JEPI is already a very conservative fund as it is. The fund picks low beta stocks and writes covered calls which offers enough protection in a down market as it is. You probably don't need to go one step further in being conservative because you would be sacrificing even more upside potential.

Another thing to note is that HELO is a new fund and we don't know how much it will pay in dividend distributions. The fund's paperwork doesn't specify a distribution target. It may pay a small distribution or perhaps no distribution at all in some years if it loses money. Income investors should probably wait for a few months and see where distributions are trending before getting in this fund.

For further details see:

HELO: A New JPMorgan Fund For Risk-Averse Investors