HCXY - Hercules Capital: A Solid Hold Yielding Over 10%

2023-06-29 13:07:19 ET

Summary

- Hercules Capital is a $2B cap BDC that specializes in providing debt financing to innovative, high-growth venture capital-backed companies primarily in the pre-IPO and M&A stages.

- HTGC's ROAE and ROAA are 860 and 380 basis points higher than the peer group's averages, respectively. The firm is outperforming most peers significantly.

- The failure of a competitor presented a significant opportunity for growth and leadership in venture and growth-stage lending for HTGC in 2023.

- HTGC's dividend growth has been well above that of most of its peers, but currently, the yield cannot be described as very attractive.

- So HTGC stock is a solid Hold. Income-seeking investors should be ready to buy the stock on strong and unreasonable dips.

The Company

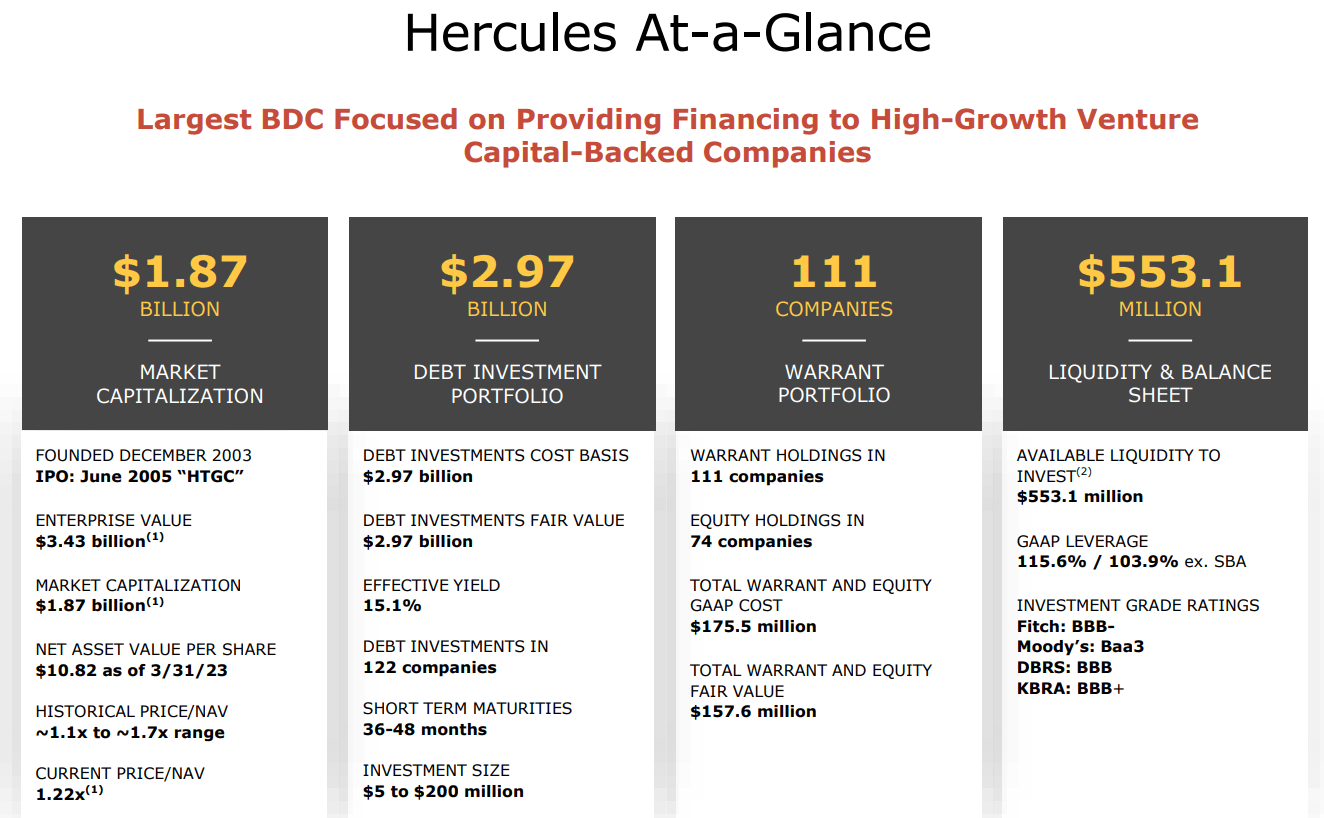

Hercules Capital, Inc. ( HTGC ) - formerly known as Hercules Technology Growth Capital - is a $2-billion market cap business development company [BDC], that specializes in providing debt financing to innovative, high-growth venture capital-backed companies primarily in the pre-IPO and M&A stages. Their portfolio spans a diverse range of technology, life sciences, and sustainable and renewable technology industries. With a focus on asset-sensitive investments, they primarily offer floating rate loans with interest rate floors, while maintaining a strong position as the sole lender in 81.5% of their debt investments. Additionally, they often include warrants in their investments for potential additional returns.

{kind=link}

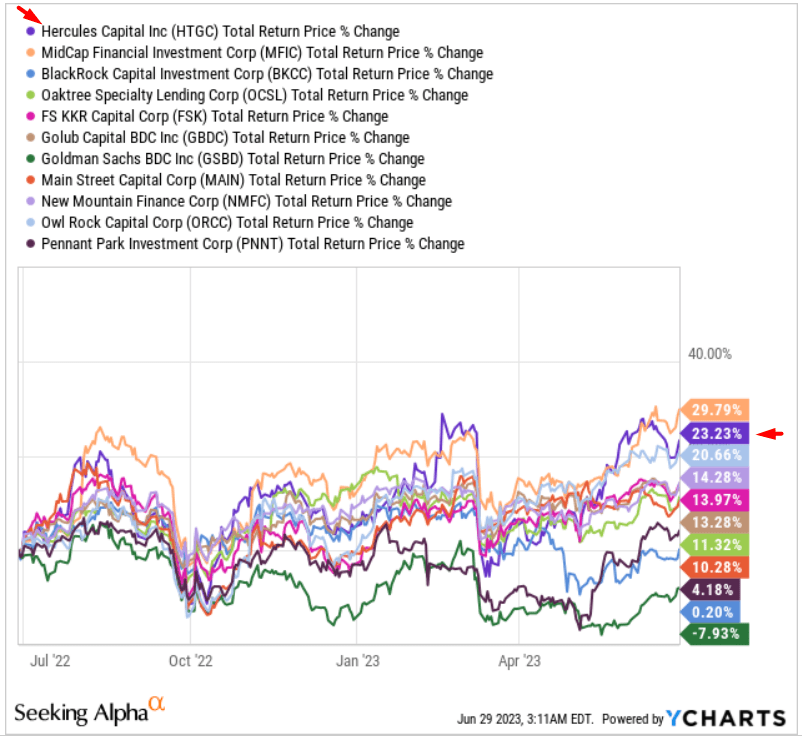

Since the beginning of the year, HTGC stock has shown above-peer dynamics despite the recent events surrounding Silicon Valley Bank and other failed financial institutions that, like HTGC, were closely associated with funding startups in the industries mentioned above.

{kind=link}

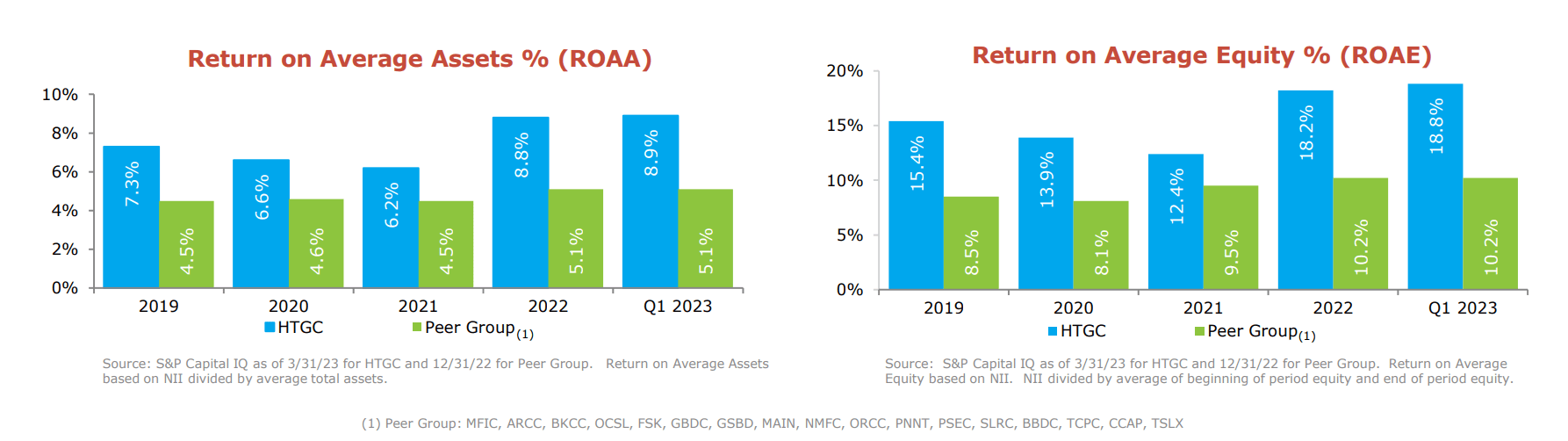

Much of this strong performance can be attributed to recent Q1 results, which demonstrated HTGC's superiority to the industry in terms of sustainability and profitability. For example, HTGC's ROAE (NII over average equity) was 18.8%, and ROAA (NII over average total assets) was 8.9% - both metrics are 860 and 380 basis points higher than the peer group's averages, respectively:

{kind=link}

Hercules Capital had a strong Q1 2023 performance , with portfolio growth and a focus on strengthening the balance sheet. The company's investment portfolio had a fair value of approximately $3.1 billion on March 31, 2023, compared to $3.0 billion in Q4 FY2022. The debt investments increased from $2.8 billion to $3.0 billion over the same period, while the equity portfolio decreased from $134.0 million to $124.4 million.

Total investment income exceeded $100 million for the second consecutive quarter [+61% YoY], driven by debt portfolio growth and benchmark rate increases, according to the CFO's words during the latest earnings call . Net investment income reached a record $65.5 million, with an effective yield of 15.1% and a core yield of 14%. From what I read, the company anticipates a core yield range of 13.8% to 14.2% for the remainder of 2023, with expectations of significant prepayment activity in Q2 FY2023.

The CEO Mr. Bluestein mentioned the company's capital-raising efforts, expansion of its RIA, and increased credit facilities, positioning Hercules well in the market. It turned out that the failure of a competitor presented a significant opportunity for growth and leadership in venture and growth-stage lending for HTGC .

In fact, what we know from the Q&A session during the latest call, HTGC made key hires from SVB and is optimistic about their ability to navigate challenging workouts and bankruptcy situations. So now HTGC may take a more senior position in the lending stack and strengthen its incumbency with portfolio companies.

Valuation

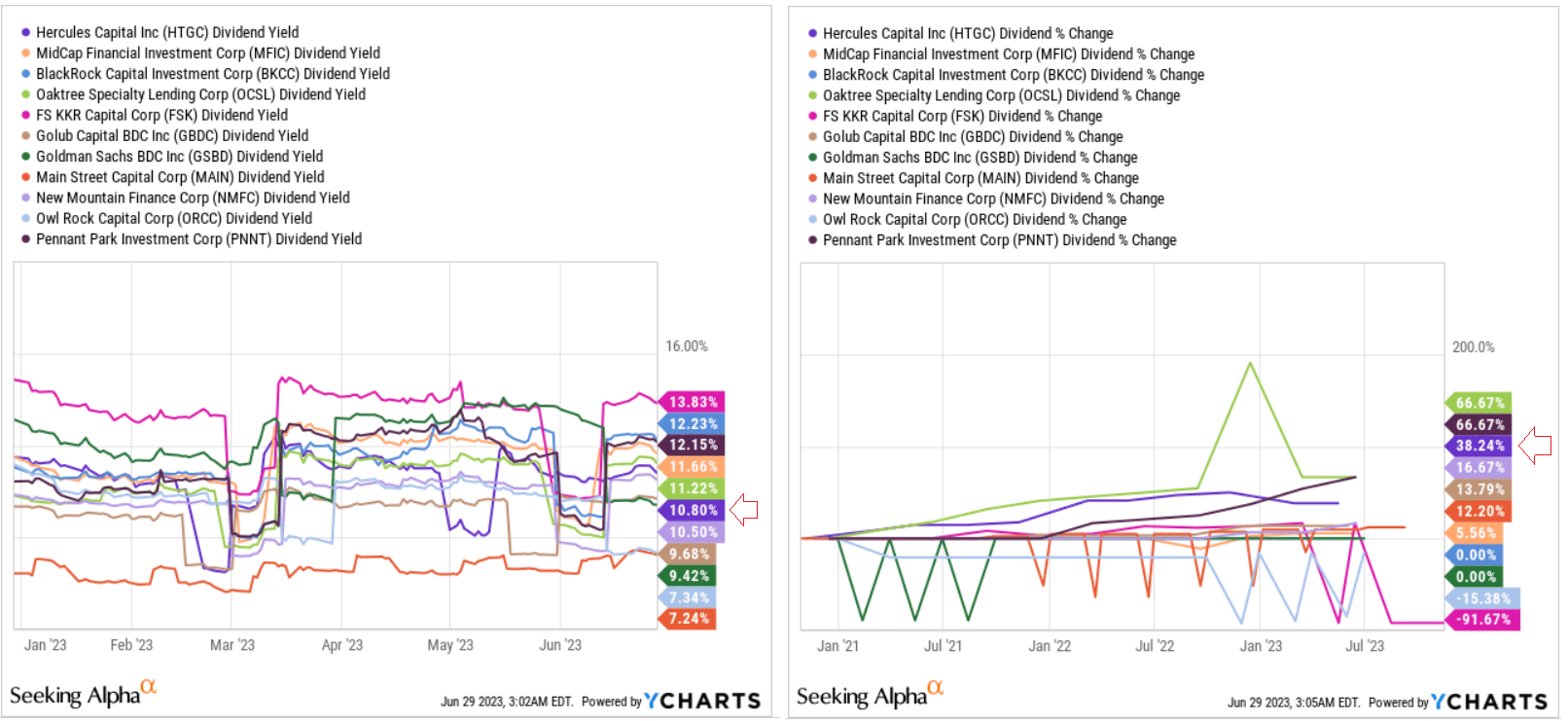

If we focus on dividend yield, HTGC is trading relatively fairly in that regard right now. I do not see a bright "buying opportunity" (by analogy with the GFC and COVID crises):

Historically, the company's dividend growth has been well above that of most of its peers, but currently, the yield cannot be described as very attractive - it is rather average, all else being equal:

{kind=link}

Valuation is a fairly fluid thing, and in many ways, individual companies - even quality companies like HTGC - follow the industry. In recent months, BDCs have been actively rallying, as we can see from the momentum of the UBS ETRACS Wells Fargo® Business Development Company Index ETN ( BDCZ ), which is up 3.47% YTD, excluding dividends.

At the recent Fed meeting, Mr. Powell made it clear that the tightening cycle is not yet complete. The expected period of higher interest rates will have an impact on highly leveraged companies whose loans are coming due soon, which could affect their ability to refinance. While many borrowers are still able to make their interest payments, their debt service coverage has declined on average. However, a growing minority of borrowers are facing restructuring, bankruptcy, liquidation, or selling at a loss. This presents a complex situation for BDCs, as they temporarily earn higher income from above-average interest rates, but also suffer permanent income losses from principal losses.

The decline in lending across all segments of leveraged lending, including BDCs, is expected to continue over the long term, possibly lasting several quarters, BDC Reporter wrote in its recent note . The pressure is unlikely to ease until interest rates return to levels seen in early 2022. High delinquencies and record bankruptcies are expected to continue until at least late 2024, and the credit stress phase is still in its early stage s.

So while the quality of HTGC's loans is not particularly questionable so far, I do not think the valuation offers investors much upside. Yes, the dividend seems safe, and if you are interested in 8-10% per year, HTGC will most likely continue to please you. But in nominal terms, I expect kind of flat momentum over the next few quarters.

Takeaway

In my view, HTGC is indeed a well-positioned BDC in the market today, benefiting from the "SVB situation", making key hires, and expanding its outreach. However, HTGC's valuation may not offer a significant upside from here, considering the potential impact of higher interest rates on leveraged companies and the expected continued credit stress in the industry.

Again - I am not saying that HTGC specifically might have serious problems with loans [my analysis did not reveal the seriousness of that possibility]. I am just talking about the industry-wide effect that could cause HTGC to trade at a dividend yield above 10-12% long enough even after a possible increase in payouts. However, for income-seeking investors , there is no particular reason to worry too much - in their place, I'd be ready to buy HTGC on strong and unreasonable dips .

HTGC stock is a solid Hold, in my opinion.

Thanks for reading!

For further details see:

Hercules Capital: A Solid Hold, Yielding Over 10%