TPVG - Hercules Capital: High Profitability To Support 9.5% Yield Limited Upside Though

2023-08-07 06:26:35 ET

Summary

- Hercules Capital, a Business Development Company, specializes in providing senior-secured venture loans to high-growth companies in diverse industries.

- Upside may be limited, but cash flow is strong and supports a generous dividend yield of 9.5%.

- Hercules Capital is currently trading at a premium to NAV of 51%.

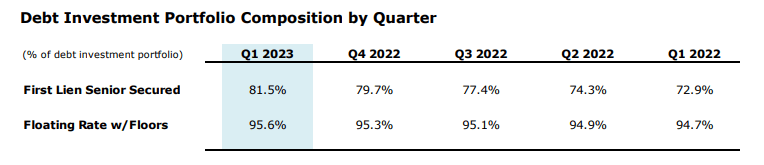

- Investment Portfolio contains 95% floating rate loans and benefits from a high interest rate environment.

In my opinion, Hercules Capital (HTGC) is a solid choice for any income investor looking to capture some reliable cash flow. The price entry is not the best right now, though, as it sits near an all-time high, so it currently remains at a Hold rating for me. Hercules Capital proves strong cash flow to support a growing dividend, high credit quality, great management, and a debt portfolio that can benefit from a high interest rate environment. Unfortunately, it seems like the upside was already captured as the stock is trading at a premium to NAV at 51%.

Company Overview

Hercules Capital is a BDC (Business Development Company) that specializes in offering senior-secured venture loans to high-growth companies backed by venture capital. Their strategy spans across diverse industries, the majority being life sciences, tech, and sustainable and renewable technology. You may recognize some of the popular brands that Hercules is involved in.

{kind=link}

Let's analyze the strategic benefits, risks, and valuation of Hercules Capital.

Internally Managed

Hercules Capital is internally managed. This simply means that rather than having an external firm manage their investments, they manage it themselves.

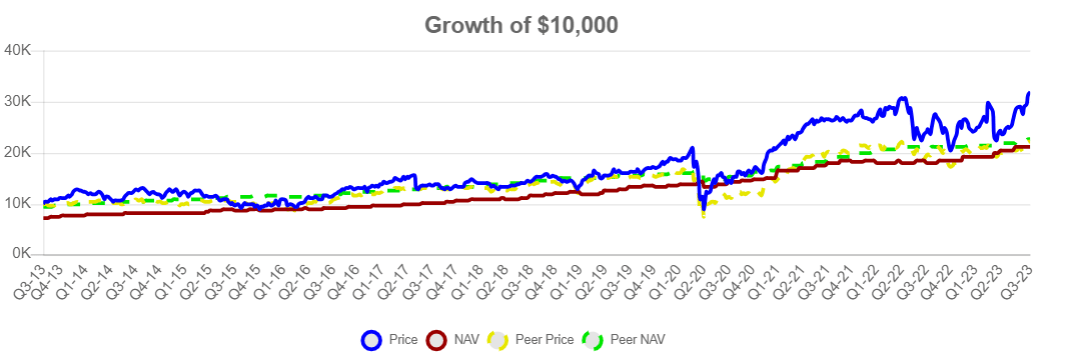

Internally managed BDCs tend to have lower operating expenses. An effect of having lower operating expenses usually means that they have lower expense ratios compared to competitors as well. Internally managed BDCs are also incentivized to perform well over time so that the stock price grows. This is because employee bonuses and salaries are typically linked to NAV (Net Asset Value) performance. In this case, HTGC has steadily traded at a premium to NAV. Even while at a premium, growth of $10,000 over the last ten years would have result in sizeable growth to $30,000.

{kind=link}

Risk

As previously stated, Hercules has historically always traded at a premium to NAV. The price / NAV premium is over 50% at the moment, so I don't think entry here is the best approach.

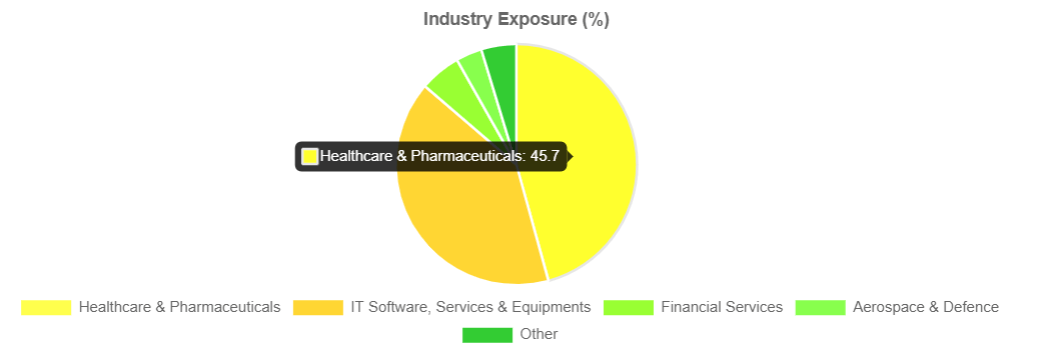

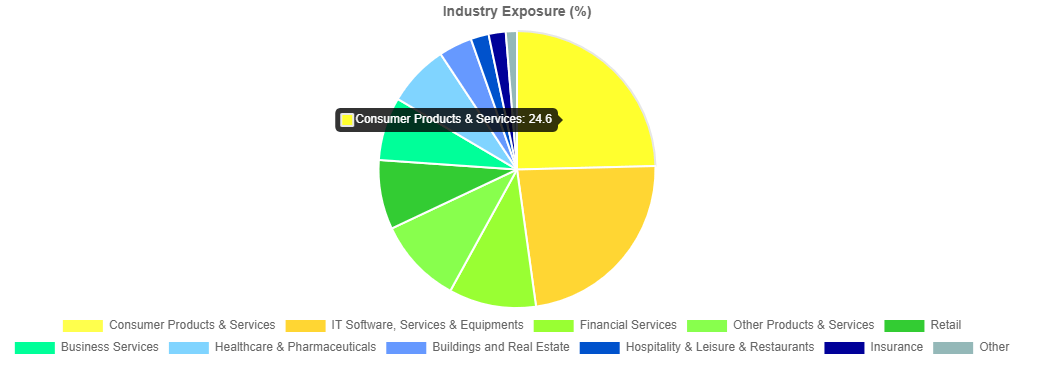

Premium aside, I do think it's worth noting that the concentration in healthcare related investments is something that stands out; not necessarily a positive or negative, but nonetheless it stands out.

{kind=link}

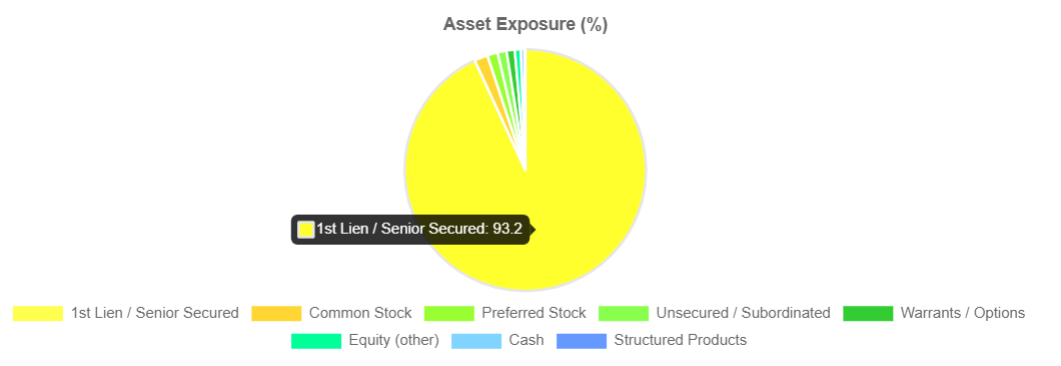

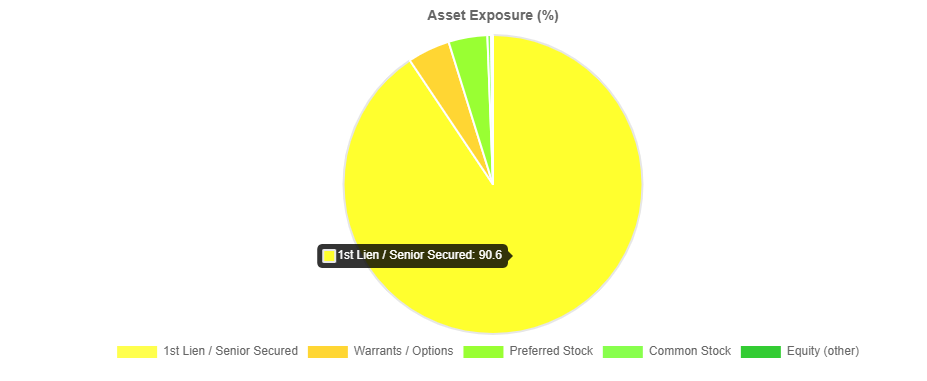

Close to half of their industry exposure is to healthcare and pharmaceuticals. Personally, I think that a bit more of an even spread across industry exposure would make this a more attractive buy candidate for me. At the same time though, the majority of that exposure is through 1st Lien / Senior Secured loans, which is reassuring.

{kind=link}

Senior secured/1st lien loans are types of debt instruments that companies can use to raise capital. These loans are typically considered low-risk for lenders because they are backed by specific assets or some form of collateral. In the event of default or bankruptcy, the lenders have a higher priority claim on the assets used as collateral, which gives them a better chance of recovering their investment compared to other types of debt. In Hercules Capital's case, this collateral can be ownership of the businesses, which they are lending too. This is a nice defensive layer to have.

Interest Rate Vulnerability

I do think a possible threat to HTGC's future profitability is the lowering of interest rates. As it stands, 95% of their investment portfolio comprises floating rates. This is notable as it may present a level of vulnerability. As we've seen, HTGC was set to benefit from all of the rising interest rates. How will this play out in the future, though, when rates start to come back down? Especially when compared against their peer, TriplePoint Venture Growth ( TPVG ), who has a portfolio of floating rate investments only totaling 61%, according to Morningstar.

Q1 Investor Presentation

{kind=link}

During Hercules Capital's earnings call in May , it was stated that early loan repayments are expected to rise. This suggests that they are lending to high-quality, highly profitable companies.

As we anticipated early loan repayments increased further in Q1 to approximately $202 million, slightly above our guidance of $150 million to $200 million, and an increase from $131 million in Q4 2022. For Q2 2023, driven in large part by M&A, we expect prepayments to increase further to between $225 million and $320 million, although this could change as we progress in the quarter. - Scott Bluestein

Valuation

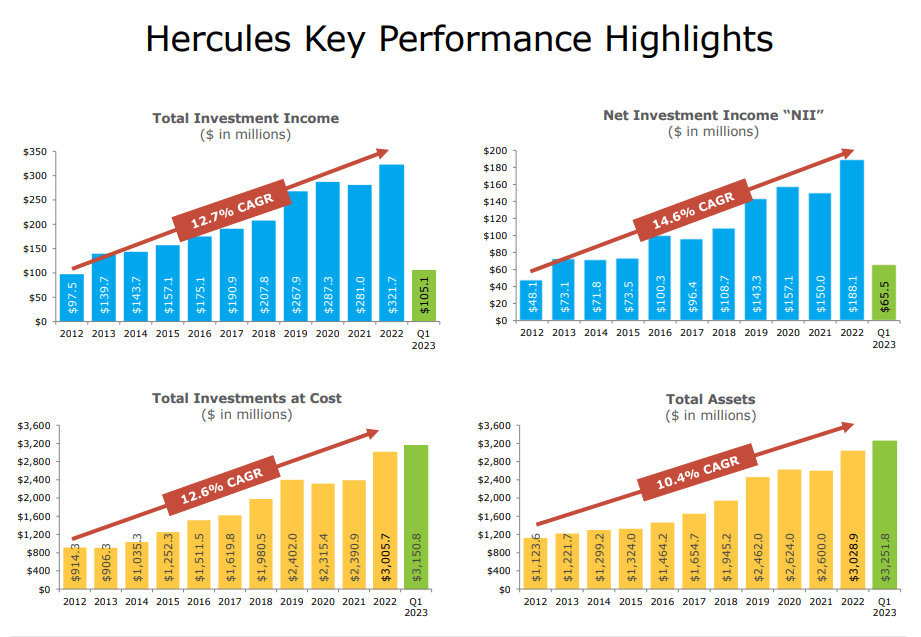

HTGC has report stellar performance: since the start of the pandemic and continuing through the Silicon Valley Bank fiasco.

They have grown well based on the following metrics from 2012 to 2022:

- Total Investment Income - CAGR (Compound Annual Growth Rate) of 12.7%

- Net Investment Income - 14.6% CAGR

- Total Assets: 10.4% CAGR

2023 Q1 Hercules Investor Presentation SA's Valuation Stats

{kind=link}

{kind=link}

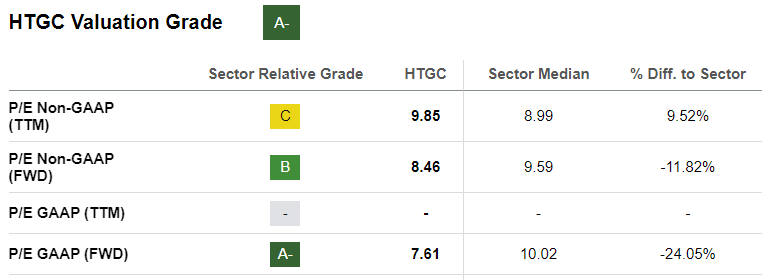

Hercules currently has an A- valuation grade and presently trades at a slight discount, with its forward P/E ratio at 7.61x compared to the sector's 10x. This amounts to a 24% price discount.

Alongside an enticing 9.5% dividend yield and a remarkable track record of 16 consecutive years of dividend payments, Hercules proves to be a cash flow rich opportunity. Nonetheless, I remain optimistic and hopeful for even more substantial upside potential in this opportunity, but given the most recent run-up with BDCs , it's hard to know where this will land.

{kind=link}

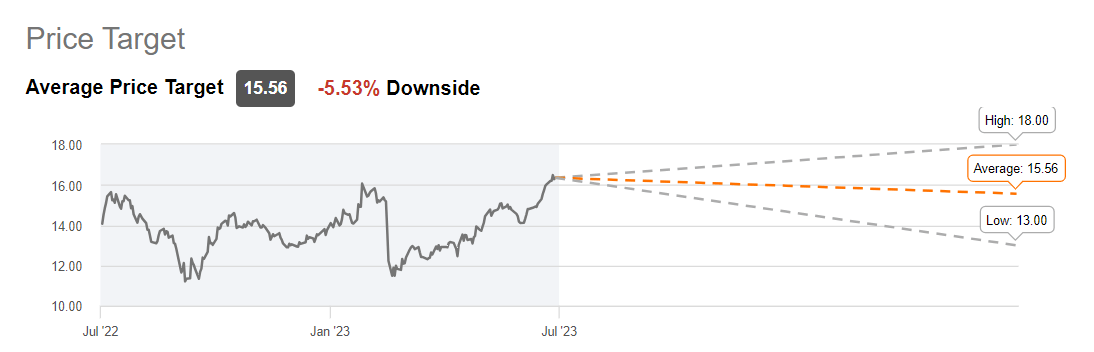

We can see that the price currently sits above the average price target of $15.56/share. With that said, I do believe that HTGC will trade towards the higher end of these price targets based on their profitability metrics. From its current price, there is only a 9% buffer from the high price target of $18/share. I believe that upside is limited in this scenario and rate environment.

In the latest earnings report, HTGC shows performance, with net investment income reaching $65.5 million. Moreover, their total investment income stood at a substantial $105.1 million, reflecting a strong overall portfolio. Their Net Investment Income ('NII') per share was reported to be $0.48.

Additionally, the company demonstrated a remarkable Return on Average Equity (ROAE) of 18.8%, affirming efficient capital utilization and shareholder value creation. Their risk management strategies were evident from an annualized loss rate of only 1.5%, underscoring their ability to maintain a low level of credit losses. These results highlight the company's sound financial health and prudent investment decisions.

Competitor

The main competitor against HTGC would be TriplePoint Venture Growth . Comparing the two on total return, we can see that Hercules has outperformed over the last 5 years.

This is partly due to HTGC benefitting from the higher interest rate environment as a larger majority of their loans are floating rate.

HTGC has a portfolio consisting of 95% floating rate, compared to TPVG's +60% floating rate portfolio. As rates remain elevated, I expect HTGC to continue to outperform.

We can also see that Triple Point's portfolio consists of a smaller percentage of 1st Lien loans compared against Hercules. While Hercules focuses on Life Science and Tech, Triple Point has a majority of their portfolio concentrated within consumer products and services.

{kind=link}

{kind=link}

While TPVG has a higher starting yield at about 12.6%, its underperformance compared to HTGC can be attributed to a less focused portfolio and less return on assets.

Dividend Comparison

Comparing Hercules Capital's dividend against the peer group, we can see that the upward price movement further reinforces why this remains a Hold for me. The dividend currently sits under its moving average, as well as on the lower end of its peer group. Based off HTGC's strong cash flow, I'd feel comfortable adding to my position when the average yield crosses back over its 10.44% average. If the upside didn't seem already to be captured, this would earn a buy rating from me.

I do still think a 9.5% dividend is great for investors that love reliable income. Cash flow supports it, so I plan to hold and continue to collect at these levels.

Hercules just announced a 2.6% dividend raise to kick off August. It's also worth noting that Hercules has already previously announced supplemental dividends for when cash flow is strong. As rates remain on the higher end of the spectrum, I anticipate more supplementals.

Conclusion

I like Hercules Capital and hold shares, so I can happily collect the well-supported dividend payments. The problem is that I think entry at these price levels are a bit high. I understand that Hercules Capital has always traded at a premium historically, but a 51% premium is out of my comfort level as of right now. I will be looking to add shares on any dips as well as keep an eye on the yield going back above its moving average.

HTGC's investment portfolio has proved to contain quality investments in the tech and life science sector, but the high level of floating rate investments may leave them vulnerable to future rate changes. In the meantime, they seem to have greatly benefitted from the rising rates and have rewarded shareholders with a recently announced divided raise.

The concentration of healthcare investments and vulnerability to interest rate fluctuations are noteworthy aspects. Despite strong profitability metrics and solid financial health, the dividend comparison and limited upside potential in the current rate environment suggest a cautious "Hold" approach.

For further details see:

Hercules Capital: High Profitability To Support 9.5% Yield, Limited Upside Though