AMKAF - Here Is Why We Maintain A Sell On A.P. Moller - Maersk

2023-08-30 03:45:37 ET

Summary

- A.P. Møller - Mærsk A/S has seen a decline in revenue and profit in the first half of 2023.

- The company's EPS has been consistently decreasing over the past three quarters.

- Weak consumer demand and oversupply of vessels are contributing to the poor freight markets.

- To address this problem is a multi-year development, which should put pressure on the share price.

Investment Thesis

We seldom make Sell calls.

One of them is on A.P. Møller - Mærsk A/S ([[AMKAF]], [[AMKBF]], [[AMKBY]]) where we started getting bearish in March this year when we started covering it. Our stance remained a sell in May too.

It is important to note that such a bearish call is not meant to indicate that the share price will plunge in the next week or month.

As a matter of fact, since the two bearish calls, the share price has stayed close to what they were at the time of publishing

{kind=link}

This article is to follow up with more data from AMKAF’s 2023 mid-year results and an analysis of what the latest trade statistics are telling us.

Latest Financial Results

When we look at Q2 results , it was to be expected that FH 2023 would be less stellar than FH 2022. It is a totally different market this year compared with last year. Revenue dropped from $40.9 billion to $27.2 billion.

The development of the underlying profit was even worse as it went from $16 billion to $3.9 billion. Free cash flow went from $12.9 billion to $5.8 billion.

A more interesting comparison would be on a quarter to quarter, as we want to see the most current trend. Are the lower freight rates and income from ports and logistics accelerating or decelerating?

EPS quarter to quarter shows a trend of three consecutive quarters of lower and lower EPS.

AMKAF - Quarterly EPS development (Data from A.P. Moller Maersk, graph by author)

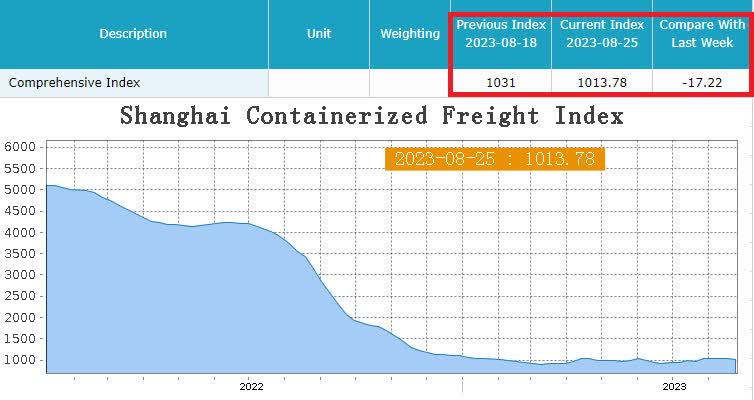

This will in all likelihood continue for several quarters to come, as spot freight rates keep dropping, as shown in the most recent Shanghai Containerized Freight Index.

Shanghai Containerized Freight Index (Shanghai Containerized Freight Index)

{kind=link}

AMKAF does fortunately have some coverage against the slump in freight rates, with about 1.5 million FFE fixed under multi-year contracts at higher rates.

Looking forward, we expect average rates to further decrease in the coming quarters as contracts have now reset and shipment rates are expected to continue to be under pressure” – CFO Patrick Jany

Their Balance sheet is still very solid.

Cash and bank balances were $10.4 billion at the end of Q2 2023. This was $693 million higher Y-o-Y.

Their net interest-bearing debt is negative. By the end of 2022, to the tune of -$12.6 billion. At the end of Q2 this year it had shrunk to -$3.4 billion.

Even if it becomes a positive debt figure, it should not be of much concern as the total equity is $56.4 billion.

It is important for us to highlight that we have no doubt that AMKAF will survive even a prolonged period of losses, should it get that bad.

Trade data

Management of AMKBY claimed that the reason for the poor freight market was due to destocking. The argument was used both at the 1st and 2nd quarter presentations to analysts.

We do not buy management's continuous claim that the weakness in freight is a result of destocking inventory.

The volume and rate environment has developed as anticipated with inventory destocking continuing to be the primary driver for lower volumes” CFO Patrick Jany

Our understanding of destocking inventory would be that the user wants to reduce their inventory temporarily in anticipation of a “better time to replenish it” This is commonly used by commodity users. If crude oil or iron ore, the world’s two largest commodities by volume, is expected to fall in price in the near future, users would typically draw down (destock) their inventory and hopefully replenish it at lower prices.

Goods moved in containers are predominantly consumer goods. We think the reason importers of these goods ship fewer containers is because of weaker consumer demand – not that they expect to “buy it cheaper in the near future”.

We follow closely the development of trade between China, including Hong Kong and the rest of the world. We have a stake in the large container terminal operator Hutchison Port Holding Trust ([[HCTPF]], [[HUPHY]]), which by the way delivered a drop of 87% in earnings to shareholders for FH 2023.

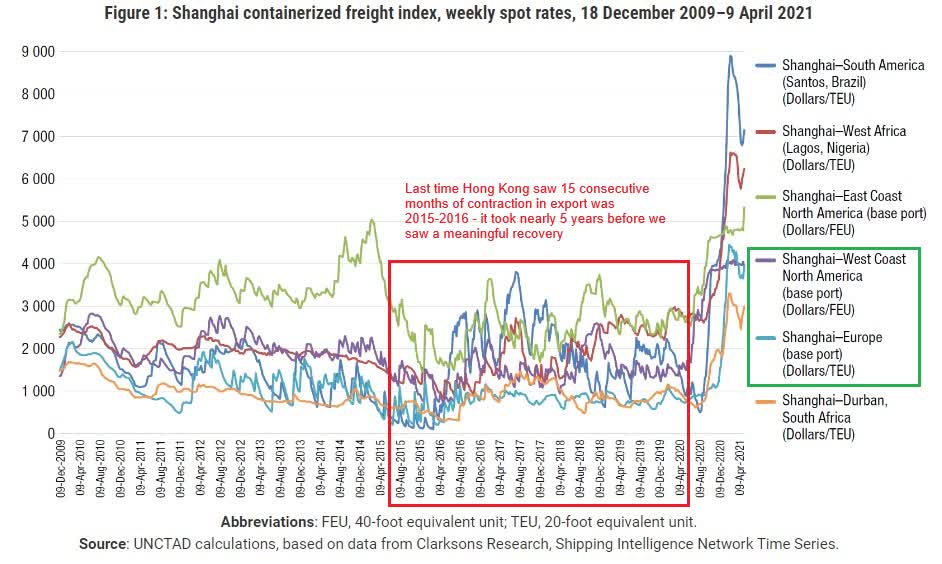

With statistics coming out in August for the month of July, Hong Kong reported 15 consecutive months of contraction in their export.

Bear in mind that as much as 60% of Hong Kong’s export is re-export of goods manufactured in China. Hong Kong has not reported such a long period of decline in exports since 2015-2016.

When we look at how the container freight cost behaved in that period, we can see that it took nearly five years for it to recover.

{kind=link}

On a slightly more positive note, the U.S. consumer confidence index’s number for July actually grew from 110 in June to 117 in July. On the other hand, Europe's consumer confidence index was more negative as it has been below 100 since July of last year. The latest reading in July of this year was 93.6

All statistics are “rearview mirror” looking, but we see weak consumer confidence in Europe and wonder if the optimistic view in the U.S. will continue.

The fleet supply side is not looking good.

The entire shipping industry is now at a very interesting crossroads as we are searching for the next fuel to propel the ships. The traditional intermediate fuel oil which has been used for the last century is going to be phased out.

Many shipowners understandably want to take a “wait and see” attitude. One of them is Star Bulk Carriers ( SBLK ). This, we believe, is going to be positive for bulk carriers, and also for tankers.

However, the liner companies, such as MSC and AMKBY are taking a more proactive approach. They have been ordering many dual-fueled new vessels.

The most popular substitute fuel is LNG. This does not produce zero emissions but lower emissions. Green bio-methanol is another fuel chosen on the path towards zero emission.

AMKBY ordered its first dual-fuel vessels, which can run on methanol, back in 2021. In total, they have 25 such vessels on order. In July, the first of the vessels just bunkered green bio-methanol here in Singapore, where we are located.

Lately, we have seen some working on “green” ammonia, which is produced using renewable energy. That is truly "zero emissions ".

Most downturns in shipping freight markets are a result of over-ordering new vessels. It is possible that containership owners will repeat the same mistake again.

According to Allied Shipbrokers, as of the 21st of August 2023, there were 347 new containership vessels ordered in 2022, and 118 vessels have been ordered so far this year.

This does not tell the full story. To put it into context, we need to think in terms of TEUs to be added to the fleet.

Throughout this year, 2.4 million additional TEUs will be added to the fleet. Next year another 2.9 million TEUs come into the market, plus 1.9 million in 2025. Recycling of ships has so far been kept low but is expected to increase. Even after taking into account recycling, the fleet capacity will increase by nearly 18%, according to Bimco’s report of the 10th of August.

Takeaway

In our graph above, we try to convey that it is a multi-year process for the shipping industry to recover from an oversupply of tonnage. It is especially hard when the oversupply comes in combination with a slowing demand.

The “Walmart’s of this world” will push freight rates lower for years to come since there is plenty of capacity on offer from the 5 largest liner companies.

With this in mind, why would investors want to buy into A.P. Møller -Mærsk A/S at this point in time?

Don’t they think that they can buy it at a cheaper price later?

We believe some might be putting too much focus on the mega dividends that were dished out at the peak of the market. Bear in mind that in what was a normal market, such as 2016 to 2021, they would pay out roughly $22 to $24 per share in dividends per year. That is a 1.3% yield based on the present share price.

We often remind our readers of the wise words from one of the world’s greatest investors John C. Bogle that

if there is a gap between perception and reality, it is only a matter of time until reality takes over”

Once that happens, the share price will see pressure.

Our Sell stance remains.

For further details see:

Here Is Why We Maintain A Sell On A.P. Moller - Maersk