HTBK - Heritage Commerce: 5.7%-Yielding Dividend Growth Bank At Bargain Basement Prices

2023-03-20 11:23:24 ET

Summary

- The recent turmoil in the banking industry with high-profile bank failures has cast a shadow. Regional banks have traded lower as a category. Bargains may be found on the market.

- Heritage Commerce Corp is an exceptionally well capitalized regional bank, and is not in any danger of suffering from bank runs.

- An analysis of recent 10-Ks shows that HTBK management largely avoided the problem of unrealized losses on securities held to maturity, and willingness to be patient on timing securities purchases.

- HTBK grows via both organic deposit growth and loan issuance, as well as industry consolidation via strategically picked acquisitions and mergers.

- Its 5.7% dividend yield more than makes up for its temporary pause in dividend growth, and can be considered a solid sleep-well-at-night income investment.

The market is awash in hubbub over the collapse of Silicon Valley Bank and Signature Bank, as well as the teetering First Republic Bank that has recently gotten a deposit bailout package from the largest US banks. The long story short, recent inflation-fighting rate hikes by the Fed have done two things:

- Raise short term treasury yields (and by extension CD yields) and reignited competition between banks over deposit rates

- Raise long term treasury yields, causing the value of securities held-to-maturity at banks to decline, denting bank balance sheets.

With sophisticated and larger depositors generally looking for higher yielding accounts, banks such as Silicon Valley Bank and First Republic Bank with highly concentrated depositor bases may be in trouble - the market fear is that if a bank run develops, banks in this situation may fail.

As a result, regional banks have traded down on the stock markets as a category, which means that if we are willing to do some legwork and set aside emotion for pure logical calculation based on actual financial situations, we might be able to find some bargain deals available on the market. This article is about one such potential bargain that has caught my eye.

{kind=link}

Heritage Commerce Corp ( HTBK ) is a bank holding company that holds the Heritage Bank of Commerce. Heritage is a rapidly growing regional bank with operations in Southern California in the "Silicon Valley", growing by both organic growth and by M&A deals. Heritage is a commercial bank, calling itself "banking for businesspeople by businesspeople".

Lending activities have a heavy tilt towards commercial real estate. As of Dec 31, 2022, by percentage composition, Heritage lends in commercial & industrial (16%), commercial real estate (51%), construction & land development (5%), residential mortgage (16%), and consumer & other (12%).

Capitalization & Balance Sheet

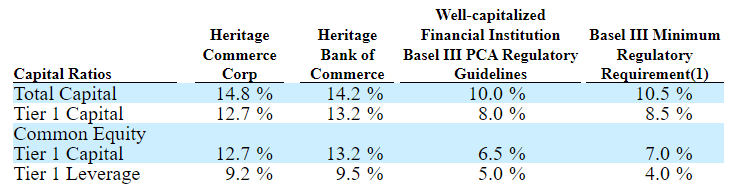

Heritage is at its face a well-capitalized bank. All of its ratios are well above the Basel III minimum regulatory requirements, and also above what the Basel III considers "well capitalized". Below are its capital ratios, as reported on page 60 of the 2022 10-K filing:

HTBK Capitalization (2022 10-K, page 60)

{kind=link}

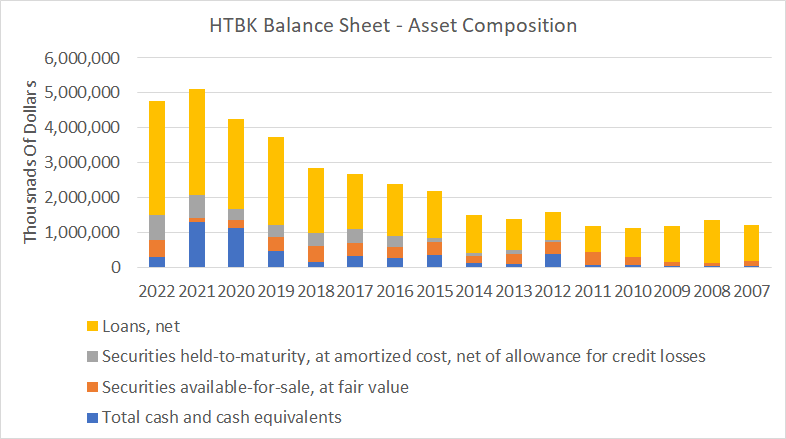

This is a good time to start to nit-pick how well Heritage has managed its balance sheet, from a top-down perspective. I have taken figures for Cash & Cash Equivalents, Securities Held For Sale, Securities Held To Maturity, and Net Loans from the 2022, 2020, 2018, 2016, 2014, 2012, 2010, and 2008 10-K filings, and pieced them together into a single chart:

HTBK Balance Sheet - Asset Composition (Various 10-K Filings)

{kind=link}

The most immediately noticeable aspect of the graph is the rapid growth of the bank over the past 15 years. The size of the bank has multiplied by about a factor of 4, driven by both deposit growth and M&A deals. As expected, most of its assets are in loans, however the 2020-2022 period requires some comment.

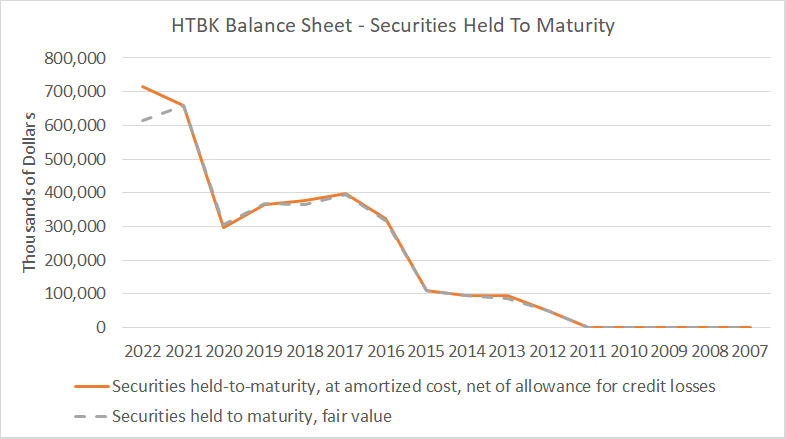

Possibly due to the COVID-19 stimulus, HTBK saw an influx of cash in its assets. Cash by itself does not yield anything, and so we can comment on how well HTBK managed its securities account. From 2015-2021, it held a sizeable quantity of securities held to maturity, and grew this account. Like most banks, HTBK did suffer unrealized losses on this account. I have put together the amortized cost and fair value figures for this account from the relevant 10-K filings:

Securities Held To Maturity - Amortized Cost & Fair Value (Various 10-K Filings)

{kind=link}

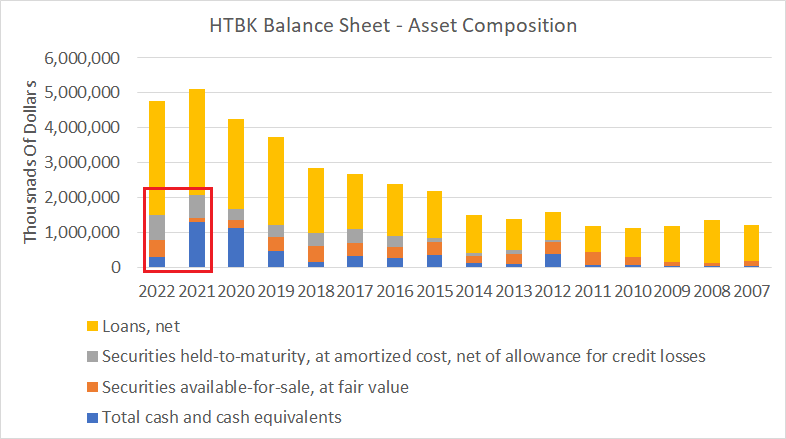

The unrealized losses (about $100M worth) are readily apparent by the end of 2022, coinciding directly with the rising of the yield curve. Somewhat questionable was the decision to dramatically expand the amount of securities held to maturity during 2021, when the yield curve had already bottomed out. However, on the flip side, we can see that in 2022, HTBK management decided to put a large amount of cash to work by buying more securities for the "held for sale" account", boxed in red below:

HTBK Balance Sheet - Asset Composition (Various 10-K Filings)

{kind=link}

From this, we can conclude that HTBK management was unwilling to go "whole hog" on buying long term treasuries as a way to deal with a large influx of deposits (at a time of basically zero interest rates anyway). Instead, it was willing to wait until the yield curve rose as a result of the inevitable Fed tightening cycle until it committed funds to its securities available-for-sale account. This is real tangible evidence of management's prudence in decision making on the timing of its securities purchases. Management was not duped into thinking that bond prices in 2021 would reflect fair value in the near future.

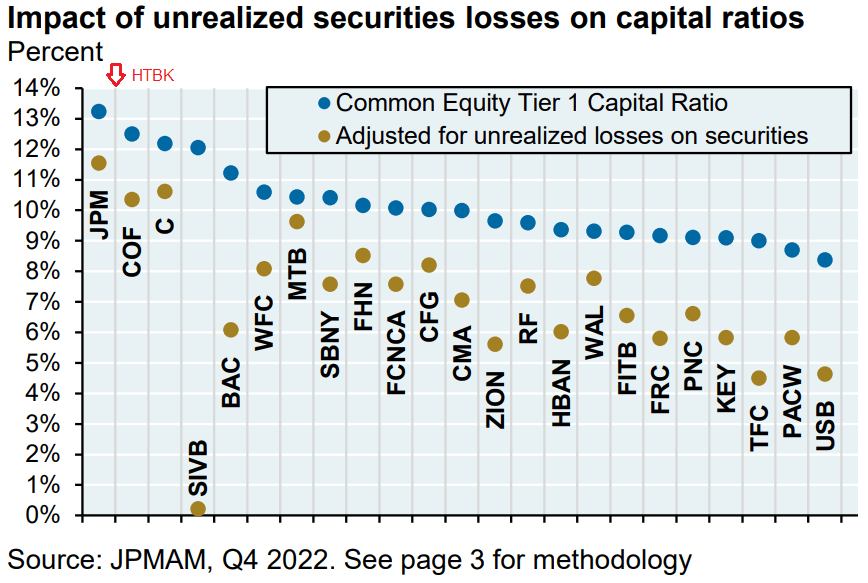

Let's put the $100M of unrealized losses into context. Below is a chart of CET1 ratios of some of the largest banks, put together by J. P. Morgan:

JPM - Eye On The Market - Silicon Valley Bank Failure (J. P. Morgan)

{kind=link}

If CET1 capital were adjusted for unrealized losses on securities, its $632M of common equity as of Dec 31, 2022 would be adjusted down to $532M, which by my estimation would reduce CET1 at HTBK from 12.7% to about 10.5%. Note that even after the adjustment, HTBK would rank near the top of this list in terms of capital ratios , just below J. P. Morgan and at the same level as Capital One and Citigroup. I have taken the liberty to add a small red arrow to indicate where HTBK would be in this chart.

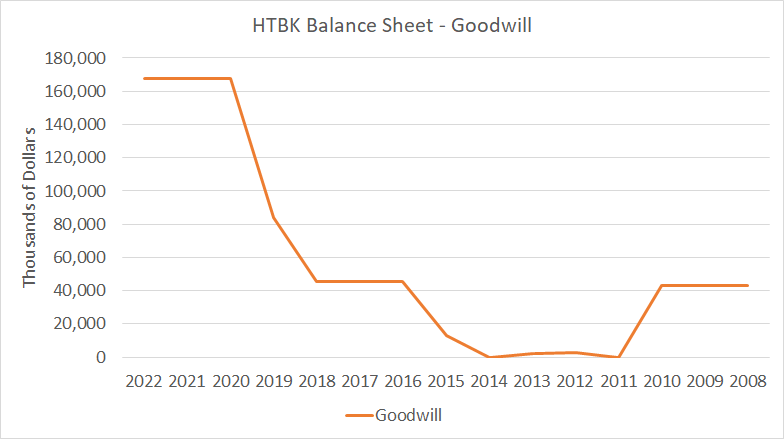

Recent Acquisitions & Balance Sheet Goodwill

As part of its growth strategy, HTBK engages in selective acquisitions and mergers. Below is a recent history of its activities :

| Target Name |

| Completion Date |

| Deal Value (millions) |

| Target Total Assets (millions) |

| Associated Goodwill (millions) |

| Presidio Bank |

| 10/11/2019 |

| $175.54 |

| $906.059 |

| $83.67 |

| United American Bank AT Bancorp |

| 5/4/2018 |

| $46.91 |

| $330.328 |

| $24.3 |

| Tri-Valley Bank |

| 4/6/2018 |

| $32.29 |

| $147.155 |

| $13.8 |

| Focus Business Bank |

| 4/23/2015 |

| $68.44 |

| $397.105 |

| $32.62 |

HTBK Balance Sheet - Goodwill (Various 10-K Filings)

{kind=link}

These acquisitions have left a trail of goodwill accumulation on HTBK's balance sheet. Note the drop in goodwill in 2010: This was part of the "clean up" after the subprime mortgage crisis.

I believe these acquisitions need to be put into scale perspective. These acquisitions added about $1.780B of total bank assets to the balance sheet. From end of 2014 to the present, the bank grew from $1.617B to $5.158B in total assets, implying that HTBK had organic asset growth of $1.761B. These acquisitions were paid for largely using share issuance. At the same time, HTBK's geographical footprint increased from 11 full service branch offices to 19 offices, all in Southern California.

I believe that even though the balance sheet shows that HTBK somewhat overpaid for these acquisitions on a book value accounting basis, and although share issuance is a less attractive than paying in cash, they were well picked and play an integral part of HTBK's growth. It is also reassuring in a way to know that HTBK is a shark in its own little pond: it has the strength to be a driver of industry consolidation.

Efficiency Ratio

The efficiency ratio for a bank is the noninterest expenses expressed as a % of total revenue. Lower numbers are desirable, and a good number for a bank is under 50%. HTBK shows an excellent trend: at the same time as it has been consolidating in its geographical home area, it has become more efficient as a bank, with efficiency ratio reaching below 50% in 2022 for the first time.

HTBK Efficiency Ratio (Various 10-K Filings)

Dividend Record

Lastly, we look at HTBK's dividend record.

While HTBK has recently stopped growing its dividend since the COVID-19 period, I believe that its current dividend yield of 5.67% more than makes up for the lack of growth. HTBK can have a place in a portfolio as an excellent income investment that investors can sleep well on, knowing that it is a bank with excellent capitalization, sound management, and partaking in efficiency-boosting industry consolidation.

Risks & Uncertainties

There are several factors that may make owning HTBK a bumpy ride, however.

The ongoing bank crises are as of yet unresolved, and cast a shadow on confidence in banks. Silicon Valley Bank and Signature Bank may be resolved, but others such as First Republic are not yet finished, and there may still be banks teetering that are waiting in the wings. At the very minimum, any further bank crises would be a cause of market volatility, meaning that a strong stomach is needed to hold regional bank stocks.

Additionally, the Fed's upcoming moves are a source of uncertainty. If the Fed continues to hike rates, then it may trigger a few more banks to become wobbly, as well as push a slowdown in US economic growth, which would be a negative for Heritage Commerce Corp. Additionally, extra rate hikes would be an upwards influence on treasury yields, which would pressure security portfolios across the board for all banks.

Finally, I would like to highlight one last consideration that is idiosyncratic to HTBK: Geographic concentration. HTBK is a regional bank and is entirely centered on the Southern California area, so its fate is tied to the events of that area.

For further details see:

Heritage Commerce: 5.7%-Yielding, Dividend Growth Bank At Bargain Basement Prices